The market closed the week ending December 12 lower, though there was significant buying interest at lower levels, which restricted the loss to half a percent for the week. The market sentiment improved after the Federal Reserve announced a 25-bps rate cut and easing liquidity concerns.

Supportive central bank policies, steady domestic investments, and optimism over trade progress despite unclear timelines also supported the market. However, consistent FII outflows and continued rupee weakness weighed on sentiment.

Going ahead, in the current week, starting from December 15, the market is expected to be ranged amid possible volatility with focus on further updates related to India-US trade deal progress, US retail sales, central banks' interest decision (ECB, BoJ and BoE), FII flow, Indian rupee, and manufacturing PMI numbers.

The Nifty 50 declined 140 points (0.53 percent) to 26,047, and the BSE Sensex slipped 445 points (0.52 percent) to 85,268 for the last week, while the Nifty Midcap and Smallcap 100 indices dropped 0.5 percent and 0.67 percent, respectively.

Overall, Siddhartha Khemka - Head of Research, Wealth Management at Motilal Oswal Financial Services expects the markets to remain range-bound with bouts of volatility in the broader indices, while any formal breakthrough on the India–US agreement could trigger a meaningful market up-move.

According to Vinod Nair, Head of Research at Geojit Investments, the markets are likely to remain sensitive to rupee stability, FII flow trends, and clarity on trade agreements, alongside global cues from the central banks' meetings.

Risks persist from currency fluctuations and global trade uncertainties; however, improving earnings visibility and liquidity support provide a constructive backdrop and downside protection, he said.

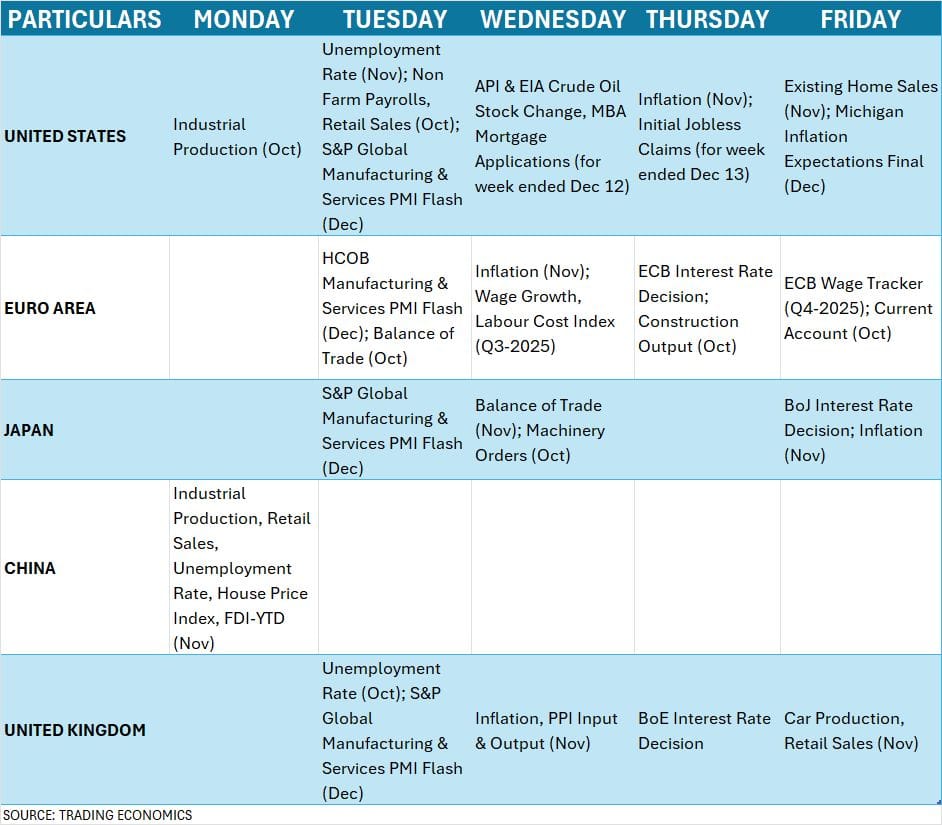

Here are 10 key factors to watch this week:

India-US Trade Deal Updates

The market participants will keep an eye on further updates related to the ongoing India-US trade deal negotiations. The optimism has been built after the recent phone call between Prime Minister Narendra Modi and President Donald Trump. Both reviewed progress in India-US comprehensive global strategic partnership, and agreed to work closely to address shared challenges & advance common interests.

According to most experts, the additional 25 percent tariff on account of Russian oil may get eliminated, and the reciprocal tariff may be reduced to 15-20 percent.

The ongoing negotiations between India and the US, along with a recent phone call between the state heads, indicate that many pending issues have been ironed out and point to positive progress on the trade deal front, Siddhartha Khemka said.

Central Banks Meetings

Globally, the focus will be on the three central banks with the officials from the European Central Bank as well as the Bank of England meeting on December 18 to announce their interest rate decision, followed by the Bank of Japan's meeting on December 19.

The Bank of England is expected to cut the benchmark interest rate by a quarter percentage point, while the ECB is likely to maintain the status quo on rates in December.

The Bank of Japan may deliver its first rate hike in 11 months amid a weaker yen and rising inflation. "Markets are likely to remain jittery, as a potential rate hike would push Japan’s benchmark rate above 0.5 percent for the first time in three decades. This could prompt a reversal of the “yen carry trade,” potentially triggering capital shifts out of global equities and adding further volatility across financial markets," Kaynat Chainwala of Kotak Securities said.

US Jobs Data

Further, the focus will also be on the economic releases from the United States, like the unemployment rate & inflation for November, and non-farm payrolls & retail sales for October, which can help the Federal Reserve to make interest rate decisions in the next policy meetings. The unemployment rate is expected to be steady at 4.4 percent, according to economists.

Global Economic Data

Apart from the US, important economic data points like China’s retail sales data, as well as inflation numbers from Europe, the UK, and Japan, will also be watched.

The focus will also be on the manufacturing and services PMI flash numbers for the current month in the United States, Japan, and Europe.

Domestic Economic Data

The market participants will keep an eye on WPI inflation for November due on December 15. Most economists expect it to remain in deflationary mode.

The unemployment rate will also be announced on the same day, followed by HSBC Manufacturing and Services PMI flash numbers for December on December 16. Manufacturing PMI in November dropped to 56.6, from 59.2 in October, while Services PMI in the same period rose to 59.8, from 58.9.

On December 19, the final day of the week, the minutes of the monetary policy meeting held in December and the foreign exchange reserves will be released.

The focus will also remain on the action at FIIs (Foreign Institutional Investors) desk as they remained buyers throughout the week and even the current month, offloading over Rs 9,200 crore worth shares during the last week and Rs 19,600 crore for the month, may be due to the delay in the India-US trade deal.

On the contrary, DIIs (Domestic Institutional Investors) remained strong buyers in equities, fully compensating the FII outflow. They net bought more than Rs 20,000 crore worth of shares during the week gone by, taking the total net purchases to nearly Rs 40,000 crore in December.

Meanwhile, the rupee continued to hit new lows for another week, weakening 0.72 percent to 90.54, the all-time closing low, amid high volumes, in addition to 0.63 percent depreciation in the previous week due to consistent FII outflow and delay in trade deal.

The primary market will remain active with a total of four companies worth Rs 830 crore launching their Initial Public Offerings (IPOs) this week, against 15 offers worth nearly Rs 14,800 crore last week.

In the mainboard segment, magnet winding wires manufacturer KSH International will open its Rs 710-crore IPO for public subscription on December 16 with a price band of Rs 365-384 per share, while from the SME segment, the Neptune Logitek IPO will hit Dalal Street on December 15, followed by Global Ocean Logistics India, and MARC Technocrats public issues on December 17.

ICICI Prudential AMC will close its Rs 10,603-crore maiden public issue on December 16, while in the SME segment, five companies - Pajson Agro India, HRS Aluglaze, Ashwini Container Movers, Exim Routes, and Stanbik Agro - are set to close their public issues this week.

Meanwhile, a total of 15 new companies will be available for trading on the bourses this week, including five from the mainboard segment. Wakefit Innovations and Corona Remedies will start trading on December 15, followed by Park Medi World and Nephrocare Health Services on December 17, while ICICI Prudential AMC will be the last to list on December 19.

In the SME segment, 10 companies - KV Toys India, Prodocs Solutions, Riddhi Display Equipments, Unisem Agritech, Shipwaves Online, Pajson Agro India, HRS Aluglaze, Stanbik Agro, Exim Routes, and Ashwini Container Movers - will be available for trading this week.

Technical View

Technically, the Nifty 50 is likely to be in the 25,700-26,300 range this week, as breaking either side of the range can give firm direction. Falling below 25,700 can bring bears into action, and may drag the index down toward 25,500-25,400; however, on the higher side, sustaining trade above can open the door for 26,500, experts said. Technical and momentum indicators signal improving momentum, though confirmation is still awaited.

F&O Cues

The weekly options data suggested that the Nifty 50 is expected to face immediate resistance at 26,200-26,300, with support at the 25,900-25,800 zone, while the 25,500-26,500 could be a broader trading range.

The maximum Call open interest was seen at the 26,500 strike, followed by the 26,200 and 26,300 strikes, with the maximum Call writing at the 26,050, 26,500 and 26,350 strikes, while the 26,000 strike holds the maximum Put open interest, followed by the 25,800 and 25,900 strikes, with the maximum Put writing at the 26,000, 25,950, and 25,900 strikes.

The fear index, India VIX, remained in favour of bulls as it fell for the third consecutive week and reached multi-week lows, sustaining below all key moving averages. It was down 2.01 percent to 10.11, signalling low uncertainty, but the sharp market move can't be ruled out given the VIX trading at lower levels.

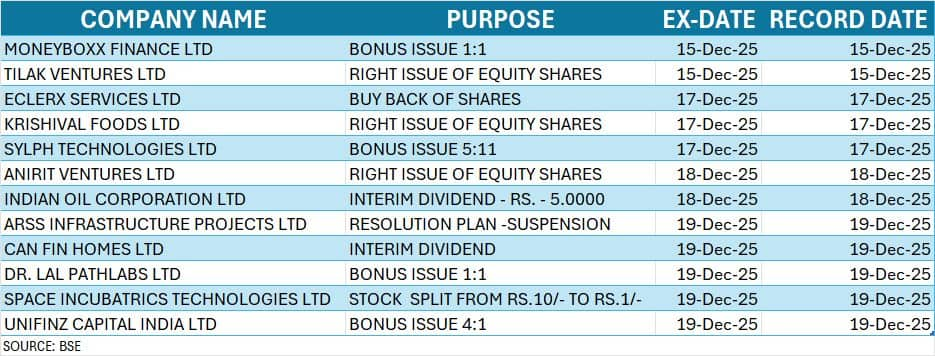

Corporate Action

Here are key corporate actions taking place this week:

Disclaimer: The views and investment tips expressed by experts on Moneycontrol are their own and not those of the website or its management. Moneycontrol advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.