Share buybacks have lost their sheen following changes in the tax regime, making the route less attractive for shareholders and significantly slowing buyback activity after October 2024. Before this, companies were required to pay a Buyback Distribution Tax (BDT) of 23 percent — comprising 20 percent tax and a 3 percent surcharge — on all shares bought back.

Post October 2024, companies pay the full buyback amount to investors. These proceeds are added to the shareholder’s income and taxed according to the applicable income-tax slab rate, which can be as high as 35.88 percent for individuals in the highest tax bracket. As a result, for promoters and shareholders in the 30 percent or higher tax bracket, buybacks offer limited incentive. In comparison, selling shares in the open market attracts capital gains tax of about 10 to 15 percent.

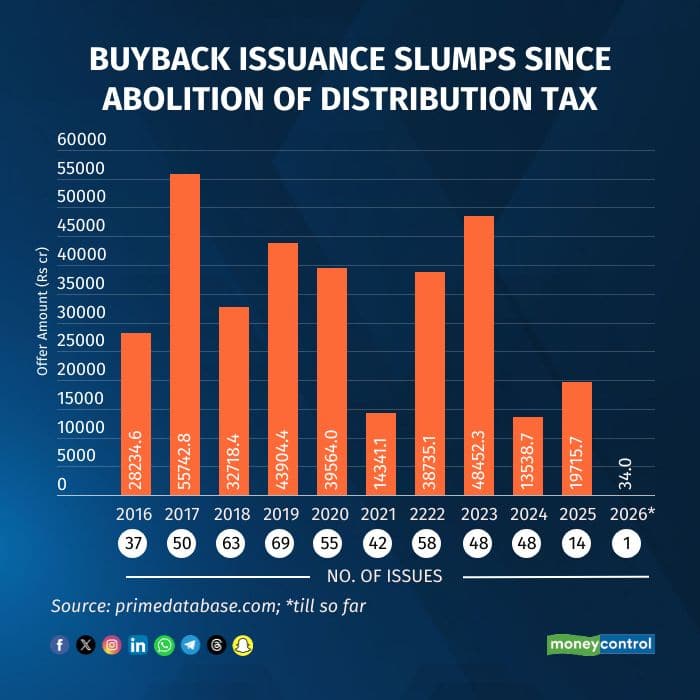

According to Prime Database, only one company has announced a buyback so far in 2026, amounting to Rs 34 crore. This compares with buybacks worth Rs 19,716 crore announced by 14 companies in 2025 and Rs 13,539 crore by 48 companies in 2024.

buyback

buyback

Until 2023, companies preferred buybacks over dividends as a means of rewarding shareholders due to tax arbitrage benefits. The buyback route was also used by public sector undertakings to meet divestment targets, a trend that has now stopped. Information technology companies, historically the largest issuers of buybacks, have also slowed the pace of offers.

In 2022 and 2023 combined, buybacks worth Rs 87,187 crore were announced by more than 100 companies. In 2023 alone, 48 companies announced buybacks totalling Rs 48,452 crore, while in 2022, 58 companies conducted buybacks worth Rs 38,735 crore.

In the interest of minority shareholders, the Finance Minister has proposed in the 2026 Budget to tax buyback proceeds as capital gains for all shareholders, ensuring that tax applies only to the actual economic gain. To curb misuse through tax arbitrage, an additional buyback tax has been introduced for promoters, resulting in an effective tax rate of about 30 percent for corporate promoters.

Experts said that if a founder is recognised as a “promoter” under the Act, the individual will not benefit from the new buyback tax regime. Such promoters will be taxed at 22 percent if they are domestic corporate promoters and at 30 percent if the promoter is other than a domestic company, in the case of long-term capital gains arising from buybacks.

Experts added that non-corporate promoters will be taxed at a higher rate than private equity and venture capital funds, provided such funds do not fall under the definition of a promoter. The objective, they said, is to enable a more tax-efficient exit for investors, including PE and VC funds. This rationalisation of taxation is also expected to partially offset the impact of a depreciating rupee on returns for global investors.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.