Adani Ports and Special Economic Zone (APSEZ), India’s largest private port operator, is expected to report strong profit, revenue and EBITDA growth in the quarter ended December, driven by an increase in cargo volumes.

However, margins may decline on-year due to revenue mix and low-margin international operations, according to analysts.

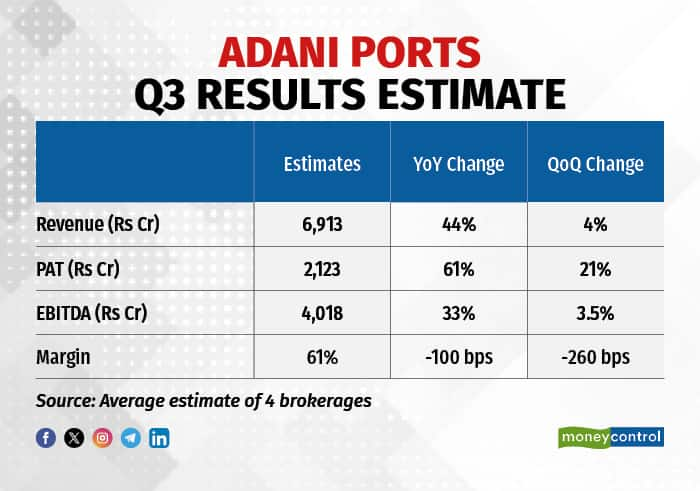

Consolidated net profit may jump 61 percent on-year to Rs 2,123 crore and revenue may surge 44 percent to Rs 6,913 crore, according to the average estimate of four brokerages polled by Moneycontrol.

Adani Ports' earnings before interest, taxes, depreciation, and amortisation (EBITDA) is seen rising 33 percent. However, margins may decline 100 basis points (bps) to 61 percent in Q3.

Also Read | Adani Energy Standalone December 2023 Net Sales at Rs 885.01 crore, up 226.4% Y-o-Y

APSEZ has a more than 24 percent market share in cargo handling. From two ports (Mundra and Dahej) in FY11, its portfolio now spans 14 ports across India. Motilal Oswal expects the company to maintain its strong positioning.

The company’s board is scheduled to meet on February 1 to approve its third-quarter results.

According to analysts at Elara Capital, the attacks in the Red Sea, through which an estimated 10 percent of global trade passes, might result in delayed vessel arrivals but it won’t drag overall volumes for Adani Ports.

"We expect port revenue growth of 37 percent YoY with port EBITDA margin of 70 percent. For Adani Logistics, we expect revenue growth of 5 percent YoY on the back of healthy volume, with a margin of 30 percent," it said.

Volume surgeTotal volumes handled at Adani Ports during Q3 stood at 108.7 million metric tonnes (MMT), leading to a healthy jump in revenue. "We expect operating margins to be in the range of 59-60 percent given the sales mix," Equirus said in a note.

In its Q3 business update, APSEZ reported a 42 percent YoY growth in October-December volumes, taking the nine-month total in FY24 to 311 MMT, registering a 23 percent YoY growth.

With monthly volumes of about 35 MMT, the company increased volume guidance to 400 MMT in FY24 from 370-390 MMT earlier. "We expect volumes for FY24 to even surpass the revised volume guidance of 400 MMT," said Motilal Oswal.

Adani Ports recently acquired Karaikal Port in Puducherry, and Krishnapatnam and Gangavaram ports in Andhra Pradesh. It is reportedly in advanced negotiations to acquire Shapoorji Pallonji Group's Gopalpur Ports in Odisha.

According to Phillip Capital, the impact of these acquisitions will be visible in YoY volume growth numbers. The brokerage estimates a 45 percent on-year growth in volumes for the quarter ended December 2023.

Improvement in utilisation at existing and recently acquired ports, growth in the logistics business along with the recovery in global trade, and volume ramp-up remain the key monitorables for investors.

Also Read | Adani Green completes funding of reserves for $750-million Holdco Bond

APSEZ has consistently generated strong cash flow from operations (CFO) over FY18-23, according to Motilal Oswal. The Adani Group company is expected to concentrate on optimising the assets it has acquired, ensuring consistent robust cash flows in the upcoming years.

"We estimate CFO to register a CAGR of 14 percent over FY23-26," the brokerage said. This, it said, will be used to fund capex and reduce debt.

Adani Ports aims to become India’s largest integrated transport utility and the world’s largest private port company by 2030. It has a diversified cargo mix and is looking to increase the cargo share of ports on the east coast.

"The operational ramp-up at the recently acquired ports is expected to drive a 14 percent growth in cargo volumes over FY23-26," the domestic brokerage noted. This would drive revenue, EBITDA, and PAT CAGR of 19 percent, 18 percent and 17 percent, respectively, over FY23-26, it said, while putting a 'buy' rating on the stock with a revised share target price of Rs 1,410.

Disclaimer: The views and investment tips expressed by investment experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.