ABB India is expected to report modest revenue growth for the quarter ended December 2025 (Q3 FY26 or Q4CY25), supported by healthy execution in Robotics and Motion, even as weakness in Process Automation and competitive intensity weigh on profitability. The company follows a January-December reporting calendar, and its Q4CY25 corresponds to Q3FY26). The company is scheduled to announce its earnings on February 19. ABB India provides electrification, automation, motion, and digital solutions to the industrial, utility and infrastructure sectors.

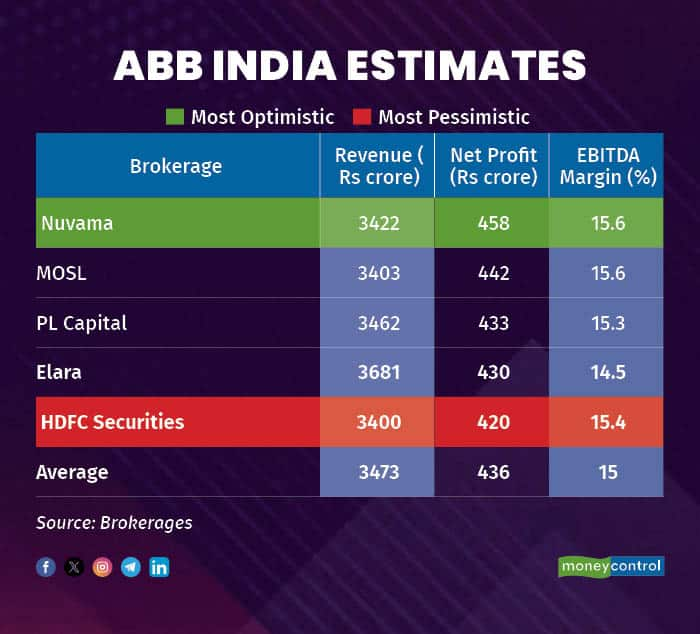

According to a Moneycontrol poll of five brokerages, revenue is estimated to be around Rs 3,473 crore for Q3 FY26, compared with Rs 3,311 crore in the year-ago quarter, a growth of around 5 percent year-on-year. Net profit is seen at Rs 436 crore versus Rs 409 crore a year ago, while operating margin is expected to improve marginally to 15.3 percent from 15.1 percent in Q3 FY25.

Key drivers for earnings

Growth to be subdued Revenue growth is expected to remain in the low- to mid-single digits amid relatively tougher comparables. According to YES Securities, sales estimates have been raised by 3 percent to around Rs 3,500 crore, about 5 percent year-on-year growth. The brokerage expects Robotics & Discrete Automation to post healthy growth supported by continued momentum in the electronics sector, while Motion is likely to grow more than 10 percent amid strong industrial activity and sustained capex by Indian Railways. However, Process Automation is expected to remain subdued and may register a double-digit decline. PL Capital also expects revenue growth of around 3 percent year-on-year, driven by healthy execution in Robotics and Motion, partially offset by likely weakness in Electrification.

Margins to contract

Margins are likely to remain under pressure during the quarter. PL Capital expects EBITDA margin to contract by around 400 basis points year-on-year due to higher import content in raw materials and an unfavourable mix. Brokerages have also flagged competitive intensity and limited pricing flexibility as key headwinds, which could weigh on operating performance despite stable execution.

Order inflow and capex outlook

Order inflows will remain a critical driver for earnings visibility. According to Nuvama Institutional Equities, revival in private capex and timely conversion of large ticket-size projects will be key catalysts going ahead. The brokerage expects order inflows to gradually trend toward the Rs 3,800–4,000 crore quarterly run-rate over the medium term to sustain earnings growth. YES Securities noted that customers may have slightly increased investments to address pent-up demand following GST rate cuts, but believes companies are likely to wait for sustained demand visibility before committing to major capital expenditure.

What analysts will be watching

Analysts will closely track order inflow momentum, particularly large-ticket project wins and conversion of the enquiry pipeline into firm orders. Commentary on segmental performance, especially the pace of recovery in Process Automation and the sustainability of growth in Robotics and Motion, will be important.

Disclaimer: The views and investment tips expressed by investment experts on Moneycontrol.com are their own and not those of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.