Wires and fast moving electrical goods maker Polycab India opened its Rs 1,346-crore initial public offering for subscription on April 5 at a price band of Rs 533-538 per share.

The public issue comprises a fresh issue of equity shares aggregating up to Rs 400 crore and an offer for sale up to 1,75,82,000 equity shares.

The offer includes a reservation of up to 1,75,000 equity shares for eligible employees who will get shares at a discount of Rs 53 per share to final IPO price. The bidding for offer will close on April 9.

Also read: Polycab India's Rs 1,346-cr IPO opens on April 5; 10 things to know

Polycab will use fresh issue proceeds for debt repayment and incremental working capital requirements.

Polycab India manufactures and sells wires and cables and fast moving electrical goods (FMEG) under the Polycab brand.

Considering its attractive valuations, strong financials and distribution network, brand position, and healthy business growth prospects, brokerages are positive on Polycab India and recommended subscribing its public issue.

"We recommend subscribe rating to Polycab given leadership with most versatile product range in cables and wires, strong distribution network, strong manufacturing base, and diversification into premium FMEG segment," Prabhudas Lilladher said.

Steady increase in sales proportion of FMEG will re-rate the stock in the long term, it added.

Ajcon Global believes increase in consumer spending, infrastructure growth, and industrial investments to drive electricals industry.

Here is what brokerages say about the issue:

Centrum Wealth Research

At higher end of the price band - Rs 538, the issue is priced at P/E of 21.6x (post dilution) on FY18 basis, (versus average industry composite of closely comparable listed peers at 44.6x) and 16.8x on 9MFY19 (annualized) basis.

Over FY16-18, Polycab registered revenue and PAT CAGR of 14.2 percent and 41.6 percent, respectively, with average EBITDA margin of 9.7 percent (consolidated). Being a leading player in the Indian wires and cables industry, Polycab could be a key beneficiary with the expected industry CAGR of 15 percent by 2023 (CRISIL).

Expansion into new products (like green products), enhancing market share by targeting growth segments (mining, renewables etc), ramp-up in FMEG business, focus on backward integration (Ryker Plant – for copper wire rods) and good brand identity could help maintain Polycab’s potential business prospects. Given the brand position, financials and business prospects, we suggest investors can subscribe to the issue.

Prabhudas Lilladher

We recommend subscribe rating to Polycab given 1) leadership with most versatile product range in cables and wires 2) strong distribution with 2800 distributors and over 0.1 million retail touch points 3) strong manufacturing base 4) diversification into premium FMEG segment with presence in fans, lighting, switchgears & switches and 5) likely reduction in working capital due to channel financing.

Polycab has strong manufacturing base with 24 manufacturing facilities (3 for FMEG). Polycab has incurred a capex of Rs11bn in the past 5 years, including plants for FMEG. Currently capacity utilization stands between 70-80 percent. In-house manufacturing will provide flexibility in improving the quality and range of FMEG. Backward integration into polymers, wire rods, cable/wire colors reduces costs and improves the quality which will continue to drive superior growth and margins.

Although FMEG is just 8 percent of sales, strong brand would enable faster scale up in the coming years. Recent export order of $137 million for an upcoming refinery is a testimony of quality and growth potential in wires and cable business.

Over FY16-18 Polycab has reported Revenue/EBITDA/PAT CAGR of 14 /24 /42 percent respectively with reported EPS (Pre-IPO) of Rs 26.2 in FY18 and around Rs 25.3 for 9mFY19. The offer at 20.5x FY18 EPS in line with Finolex cables (20xFY18 EPS) but at significant discount to ECD players like Havells (68xFY18 EPS) and Crompton Consumer (44xFY18 EPS).

Steady increase in sales proportion of FMEG will re-rate the stock in the long term.

Ajcon Global

We believe increase in consumer spending, infrastructure growth, and industrial investments to drive electricals industry.

At the upper end of the price band, Polycab IPO is valued at a P/E of 16x at 9MFY19 annualized EPS which is cheap as compared to listed peers like Havells, Bajaj Electricals and KEI Industries. With due consideration to factors like:

a) Well positioned to capture Industry Potential across wires and cables and FMEG segments,

b) Huge market to be tapped,

c) Market leader in wires and cables in India,

d) Diverse suite of electrical products with varied applications across a diverse customer base,

e) Backward integration by manufacturing of essential raw materials inhouse,

f) Strong distribution network (2,800+ Authorized Dealers and Distributors 100,000+ Retail Outlets),

g) Strong brand in the electrical industry,

h) Proven track record of financial performance (FY16 –18): Revenue CAGR: 14 percent, EBITDA CAGR: 24 percent and PAT CAGR: 42 percent, Leverage: 0.34x, decent Return on Equity of 15.76 percent, we recommend subscribe to the issue.

Hem Securities

The company is bringing the issue at P/E multiple of approximately 20 on FY18 EPS basis at price band of Rs 533-538/share. Company being market leader in wires and cables in India has diverse suite of electrical products with varied applications across a diverse customer base with strong distribution network.

Looking after strong fundamentals of the company along with the healthy growth prospects of sector, we recommend subscribe on issue.

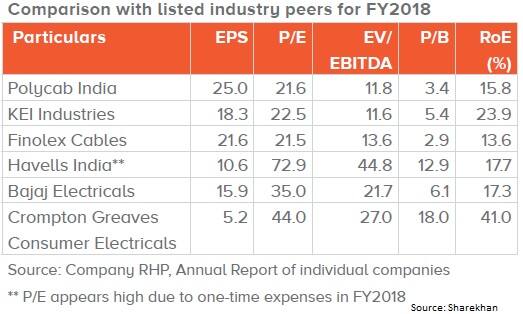

Sharekhan

Polycab has a strong growth profile with revenue, operating profit and net profit reporting a CAGR of 10 percent, 23 percent and 42 percent, respectively, during FY2016-FY2018. Further, it has low net debt/equity of 0.2x as on December 2019.

At the upper price band, Polycab is valued at a P/E of 21.6x its FY2018 earnings which is much lower than the industry average but almost at par with close peers like KEI Industries and Finolex cables. However its return on equity is tad lower than industry players barring Finolex cables.

Disclaimer: The views and investment tips expressed by investment expert on moneycontrol.com are his own and not that of the website or its management. Moneycontrol.com advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.