Oil refining companies reported a weak operational Q1 performance, which was countered by unusually high inventory gains. In line with global trends, gross refining margins (GRMs) remained weak. Forex losses and increase in interest costs impacted profitability.

Although there has been a substantial correction in stock prices, we approach the current year with caution given the increasing global uncertainty, rising crude oil prices, growing agitation against higher domestic petrol and diesel prices and government’s unwillingness to reduce taxes on fuel. Margins might see some pressure given higher crude oil prices and the upcoming election season.

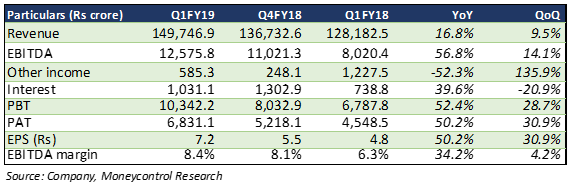

Indian Oil Corporation (IOCL)

Topline grew 17 percent year-on-year and earnings before interest, tax, depreciation and amortisation (EBITDA) saw a 57 percent uptick due to inventory gains. Excluding the impact of these, EBITDA saw a sharp decline. A 52 percent contraction in other income and a 40 percent uptick in interest cost impacted profitability. Reported GRM stood at $10.2 per barrel (bbl), whereas normalised margin stood at $6.8/bbl. GRM was also impacted by 22 day maintenance shutdown at IOCLs Paradip refinery, which has since come back. Foreign exchange loss of Rs 1,800 crore also dragged core performance.

The company has won 18 geographical areas in the recently concluded city gas distribution bidding round, which might bring some earning improvement in the longer run.

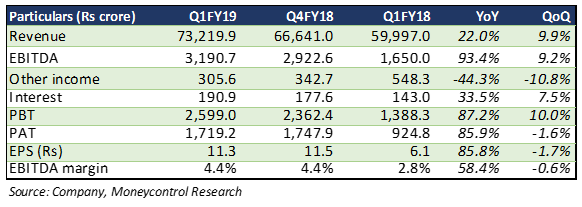

Hindustan Petroleum Corporation (HPCL)

The 93 percent YoY gain in HPCL’s EBITDA was aided by Rs 1,910 crore of inventory gains. The quarter gone by saw a forex loss of Rs 540 crore and Rs 170 crore lost on account of oil bonds. A 33 percent increase in interest expenses and a 44 percent decline in other income led to further weakness in normalised net income. GRM came in at $7.1/bbl, whereas normalised GRM came in weaker at $3.1/bbl. While domestic volumes grew 4.7 percent YoY to 9.6 million tonne, exports remained low at 0.1 million tonne.

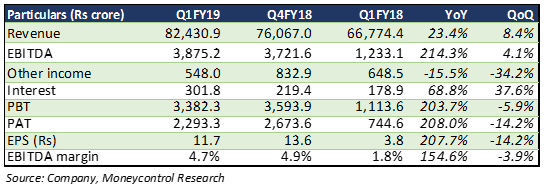

Bharat Petroleum Corporation (BPCL)

EBITDA saw a sharp 204 percent jump on the back of inventory gains during Q1 FY19 and low base of last year. On the operational front, after removing inventory gains, expenses saw a substantial uptick YoY and performance remained weak. The company reported a forex loss of Rs 710 crore and Rs 170 crore loss on oil bonds. GRM stood at $7.5/bbl, with normalised GRM at $4.2/bbl. Crude throughput declined a percent quarter-on-quarter to 7.7 MT, reflecting lower utilisation at refineries. While domestic volumes grew 9.2 percent at 10.9 MT, international segment saw a dip of 36 percent at 0.31 MT.

The management aims to work on improving the product and sourcing mix to enhance margin. To improve diesel volumes, BPCL is working on further enhancing its highway presence.

OutlookOwing to several geo-political factors, crude oil prices have been on an upswing globally, resulting in a sharp upswing in petrol and diesel prices in the past few months. This has created much furore in the domestic market, putting margins of oil marketing companies (OMCs) under the scanner. Expensive crude had a negative impact on GRMs of downstream oil companies globally during Q1.

The current provision made for subsidies on cooking fuel are inadequate as compared to estimated amounts on current crude oil prices. If the latter sustains at current levels, then there might be delays in subsidy payments from the government which could lead to further uptick in interest costs.

Net marketing margins in petrol and diesel has been notoriously tweaked around elections in the past. Given this manipulation of marketing margin of OMC and upcoming state and general elections we remain cautious on the sector.

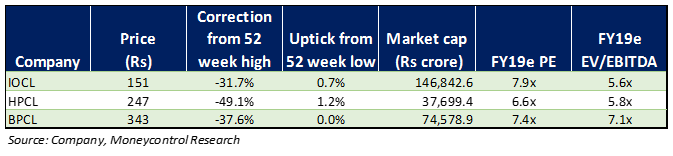

With rising uncertainty, IOCL, HPCL and BPCL have corrected substantially in the last one month, hitting 52 week lows. While the steep correction makes them attractive, we remain cautious as there is genuine concern around the margin profile in coming quarters. OMCs have been protected for now, but the situation might change with populist actions from the government.

Follow @RuchiagrawalFor more research articles, visit our Moneycontrol Research pageDiscover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.