On June 1, more than 5,500 trades took place in the secondary market for government bonds. But the 10-year Wholesale Price Index (WPI)-linked bond, which matures today on June 5, was traded just 802 times in its entire lifetime.

The story of the WPI-indexed bond is that of collateral damage – one that was caused by a shift in the Reserve Bank of India's (RBI) focus to Consumer Price Index (CPI) inflation in early 2014.

The central bank began issuing inflation-indexed bonds linked to WPI inflation in June 2013. Till the end of the year, some Rs 6,500 crore worth of these bonds were auctioned. The RBI held another auction for Rs 500 crore of these bonds on January 29, 2014 but it rejected all the bids it received.

The rejection in what proved to be the final auction of these WPI-linked bonds was not a surprise because it was held a day after then RBI governor, Raghuram Rajan, adopted the CPI inflation glide-path set out by the Urjit Patel-led committee on revising and strengthening the monetary policy framework.

WPI inflation crushedThe Patel committee, which recommended the RBI adopt a flexible inflation targeting framework spelt out in terms of CPI inflation, had submitted its report a week prior to Rajan's announcement.

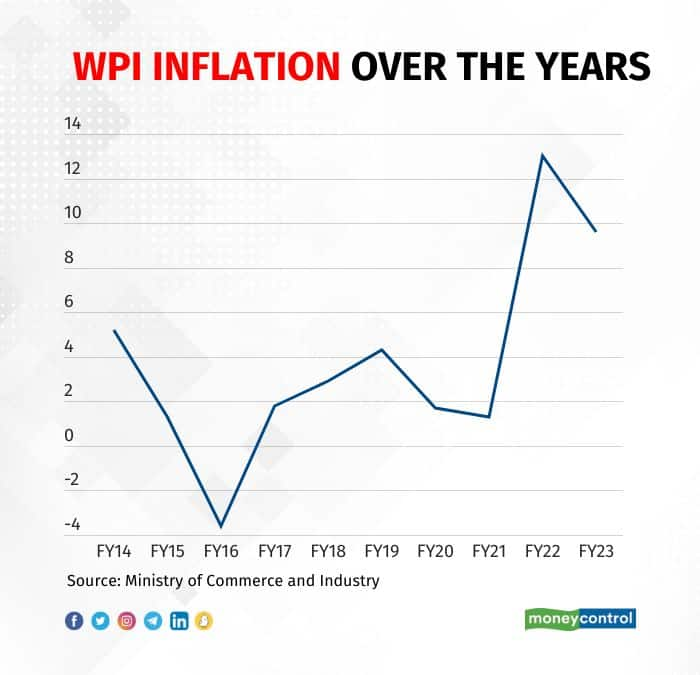

In December 2013 – when the last of these WPI-linked bonds were issued – wholesale price inflation was a healthy 5.88 percent and averaged 5.2 percent in 2013-14. Issued at a real coupon rate of 1.44 percent, this roughly meant a return of more than 6 percent in the first year.

But matters soon took a turn for the worse as the Rajan-led central bank tightened financial conditions to rein in double-digit growth in retail prices. As CPI inflation began to cool off, paving the way to meet the Patel committee's glide-path target of 6 percent by January 2016, wholesale inflation plunged to 1.3 percent in 2014-15 and went sub-zero to -3.6 percent in 2015-16.

Bond prices move in the direction opposite to that of yields. If yields rise, prices fall and result in notional losses for bond holders.

With retail inflation becoming the nominal anchor for Indian monetary policy, the market for WPI-indexed bonds collapsed as the RBI policy was no longer responding to the sharp fall in wholesale inflation. Those who bought the bonds were saddled with them and found no exit route. Such was the concern among these institutional investors that on more than one occasion, the now-defunct post-monetary policy interaction between the RBI and the analyst community saw the central bank's top management being asked what the future held for these instruments.

Incomplete repurchaseTo end the stalemate, the RBI decided to buy them back. The first of these repurchase auctions, held in January 2016, was a washout, with the central bank rejecting all offers made by holders of these bonds. But in the subsequent three repurchase rounds, it managed to buy back Rs 5,347 crore of these bonds at a steep discount of 10-15 percent.

What remained was Rs 1,153 crore worth of these bonds, which will finally mature today.

"Post repurchase, I am not sure what price was available. For somebody holding the bond, where does he go?" a market participant who had purchased the WPI-linked bonds said on the condition of anonymity.

Indeed. After being issued on June 5, 2013, the bonds were changing hands at a discount within a week. Before the end of the month, the discount was a huge Rs 5. By the end of January 2014, these bonds with a face value of Rs 100 were trading at just over Rs 81.

Graveyard of bondsTo be fair, 2013 was a bloodbath for fixed-income products. And, the 1.44 percent WPI-indexed bond was not the only 10-year government security to meet an untimely death.

On May 22, 2013, then Federal Reserve chair Ben Bernanke said the US central bank might soon start scaling back its asset purchase programme, triggering a wave of panic, volatility, and uncertainty that crashed over world markets. The 'taper tantrums' caused by Bernanke's comments led to a rapid increase in capital outflows from India and other emerging market economies, resulting in a sharp rise in bond yields.

The carnage that followed was such that the 10-year government bonds issued on May 17, 2013 never really became a benchmark for the Indian market. Issued at a coupon of just 7.16 percent, a true picture of the bond market emerged when the next 10-year bond was issued by the RBI in late November 2013 at a significantly higher coupon of 8.83 percent.

Late flourishWith the rate of interest on the WPI bonds linked to wholesale inflation, the return on them was desperately poor. But, after years of getting a pittance, those who still hold them got a bumper return in 2021-22 and 2022-23 after inflation flared up dramatically because of the supply disruptions caused by the coronavirus pandemic and the surge in global commodity prices following Russia's invasion of Ukraine.

WPI inflation, which averaged less than 5 percent every year from 2014-15 to 2020-21, surged to 13 percent in 2021-22 and 9.6 percent in 2022-23. In absolute terms, the amount of interest received by the holders of these bonds increased to Rs 20.11 crore in 2021-22 from Rs 18.77 crore in 2020-21, the RBI told Moneycontrol in response to a Right-to-Information query.

Needless to say, the final two years of the bond's life did not make up for the sub-par returns of the first eight years. But its maturity serves a reminder of a seemingly distant past of India's policy framework.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.