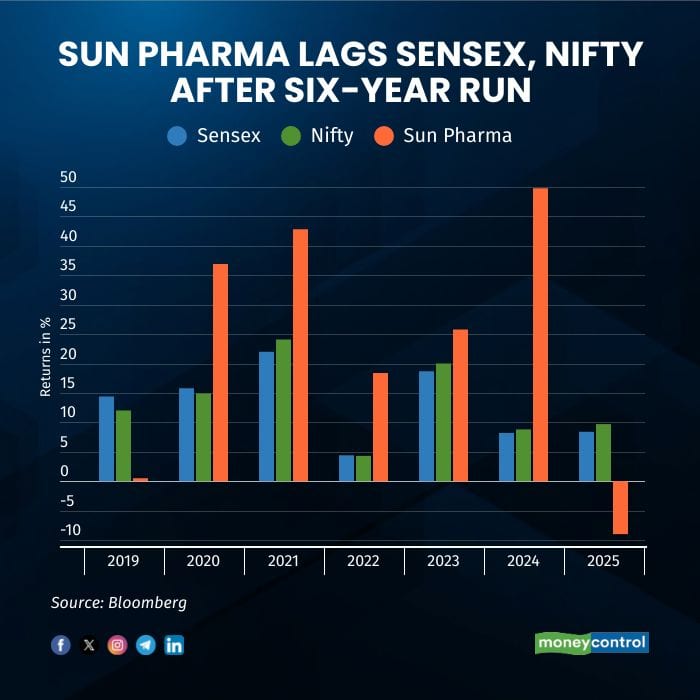

Sun Pharmaceutical Industries Ltd, the country’s largest drugmaker by revenue and market value, has slipped behind the Sensex and Nifty in 2025 — its first spell of underperformance in six years. The weakness reflects softer momentum in the US business, rising competition in generics, sustained pricing pressure at home and abroad, unfavorable currency movements across several emerging markets and continuing tariff uncertainty.

So far this year, the stock has declined about 8 percent even as both benchmark indices have risen close to 9 percent, Bloomberg data show. The broader pharma pack has also seen volatility, with Piramal Pharma down 35 percent, Mankind Pharma lower by 25 percent, Ipca Labs falling 15 percent, Lupin 11 percent, Aurobindo Pharma 8 percent and Dr Reddy’s Laboratories down 7 percent, while the Nifty Pharma index slipped 3.5 percent.

US formulations delivered modest growth as competition intensified and gRevlimid volumes stayed subdued, limiting overall progress despite gains from innovative products. Analysts expect gRevlimid to make only a minimal contribution ahead, while higher research and development spending, elevated operating costs, slower revenue growth and a heavier tax burden continue to weigh on performance.

Regulatory scrutiny remains a headwind for the generics portfolio. Plants at Halol, Mohali, Dadra and Baska are at different stages of review and are implementing Corrective and Preventive Action plans. Recently, the USFDA has classified the Baska site as “Official Action Indicated,” without disclosing the number or nature of observations.

The facility manufactures key generic products including the Albuterol Ipratropium inhalant, which generates more than $100 million annually, and Amphotericin B, with sales of about $15 million. These products contribute an estimated seven percent of US revenue excluding gRevlimid and nearly two percent of core revenue, underscoring Baska’s role in Sun Pharma’s sterile-injectables network.

For now, generics remain outside tariff coverage and the proposed 100 percent tariffs on imported innovator medicines have not yet been implemented. The company does not face incremental import duties and, with part of its manufacturing base located in the US, is positioned to reassess plans if policy changes, analysts noted.

In the domestic market, performance has been steady despite pricing pressure, with momentum expected to build through recent launches such as Cequa for dry-eye disease, Tyvalzi for ischemic stroke, Rytstat for anaemia tied to chronic kidney disease and Lyvelsa to help reduce the risk of kidney failure linked to Type-2 diabetes. Analysts expect Sun Pharma to continue gaining share in the India Pharma Market, supported by strong therapy presence and an expanded field force.

Several analysts view the recent correction in large-cap pharma stocks as a buying opportunity, arguing that earnings visibility remains intact. Sun Pharma’s one-year forward price-earnings multiple stands at 32.15 times versus its 10-year average of 28 times. The stock trades at a premium to peers such as Lupin at 21.5 times, Dr Reddy’s at 20.26 times and Cipla at 25 times. According to Bloomberg, 37 of 43 analysts have a buy rating on the stock.

Brokerage Nirmal Bang has marginally pared estimates, citing firm operating costs, ongoing investment in research and development, softer topline trends and a rising tax burden. Its research highlights longer-term supports including sustained strength in branded formulations in India, the ramp-up of specialty products in the US such as LEQSELVI and UNLOXCYT, opportunities in dermatology, ophthalmology and onco-derma, and margins supported by disciplined execution.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.