Ruchi Agrawal

Moneycontrol Research

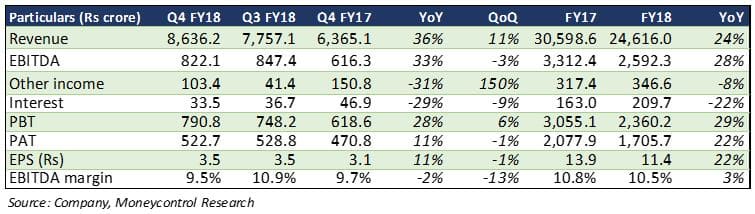

Petronet LNG (PLNG) reported a strong set of Q4 FY18 numbers on the back of a healthy uptick in volumes and utilisation of terminals. While revenue increased 36 percent year-on-year (YoY), net profit rose 11 percent YoY. Earnings before interest, tax, depreciation and amortisation (EBITDA) margin took a 20 basis points YoY hit due to higher employee and other expenses, which increased significantly (around Rs 10 crore one-time expense included in employee costs).

Strong volumes

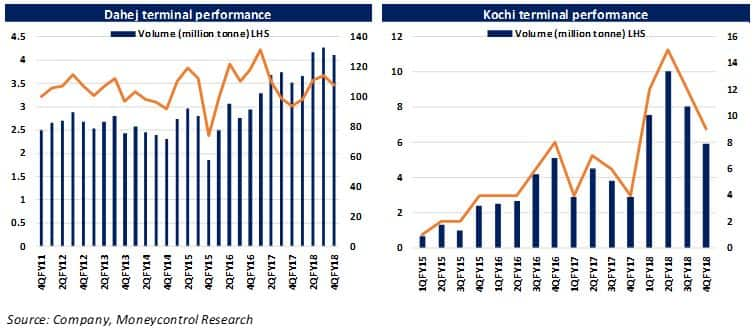

The company reported a strong 18 percent YoY uptick in volumes, though sequentially it fell a percent because of two lesser days in Q4. Lower utilisation and volumes at Kochi terminal were also partially responsible as there was a seasonal shutdown of Fertiliser & Chemicals Travancore (FACT) facility. While the utilisation at the Dahej terminal remained at 109 percent, at Kochi it was 9 percent. Dahej volumes remained strong at 207 trillion British thermal units (Btu) (up 16.8 percent YoY), while at Kochi the volumes were around 5.9 trillion Btu (up 104.2 percent YoY). The pipeline at Kochi is expected to be installed by Dec 2018, post which the volumes and utilisation at Kochi are expected to improve.

Capacity expansion to drive growth

The company is expanding capacity at its Dahej facility to 17.5 million tonne per annum (mtpa) from 15 mtpa, which would be complete between March and June of next year. Given the deficit supply situation in the market, the management is confident that additional capacity would be fully booked. It further plans to expand capacity by 2.5 mtpa.

Threat from domestic producers and competition

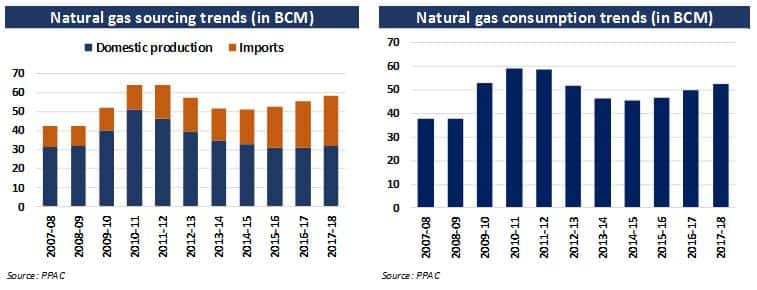

After a period of stagnant domestic production growth, upstream companies like Oil and Natural Gas Corporation (ONGC) and Reliance Industries-British Petroleum (RIL-BP) are planning to ramp up domestic gas production. Around 60 million metric standard cubic meter per day (mmscmd) of gas is expected to flow in from domestic sources by 2022. This is expected to replace the expensive imported liquefied natural gas (LNG) which would have an impact on LNG regas volumes.

The management said incremental domestic gas production will mostly be offshore high pressure gas. Since the production process is expensive, it sees bleak prospects of it replacing LNG. Also, there are numerous issues surrounding the production process itself, so ramping up may not take place.

There is a large gap between overall gas consumption and domestic production at present. Domestic production accounts for less than 60 percent of consumption. A parallel increase in demand, with a preference for gas as an alternate fuel, owing to higher crude prices, increasing pollution and rising demand from the power sector, cannot be ignored. There will still be a market for imported LNG. Moreover, PLNG has almost tied up its entire capacity in long-term contracts, thus limiting the impact on volumes.

The company also faces a threat from increased competition, with a new terminal coming up at Mundra. But the management assuaged concerns, saying operations at Mundra and not expected to begin until March next year. The management highlighted that regas tariffs are very competitive due to which they will still remain the preferred terminal.

International expansion

The company has been eyeing expansion in Bangladesh and Sri Lanka. Capex outlay for the Bangladesh land‐based terminal (7 million tonne) is almost $100 million. The same for Sri Lanka (2.5 MT) stands around $300 million. The management is in talks with the Bangladesh government for assured volumes and offtake. Bangladesh has announced plans to hike domestic gas prices, so that RLNG can be absorbed in domestic markets. The management sees visibility of the Bangladesh expansion in the near-term. However, the Sri Lankan expansion is subject to many approvals and would take time before it comes on stream. The company is also exploring opportunities for integrated expansion in Qatar in the longer term.

Outlook

We see bright prospects for the regasification business as gas demand is expected to ramp up rapidly and owing to limited growth in domestic production. Despite increasing competition in the coming years, the company’s capacity remains fully tied up in long-term contracts. With capacity expansion on cards, we see higher volumes and cost benefits. The stock has corrected almost 7 percent in the past 12 months and is 23 percent below its 52-week high. The stock is trading at FY19e price-to-earnings of 14 times. With continued shortage of LNG domestically and capacity expansion that should boost future volumes, we see the stock as a steady long-term performer.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.