Kotak Mahindra Bank didn’t disappoint the Street with its high quality earnings performance for the March 2017 quarter. However, the business growth numbers were significantly softer compared to some of its peers who have recently reported. While being more than adequately capitalised (capital adequacy ratio 16.8 percent), the caution from this savvy bank is intriguing.

A broad look at the Q4 FY17 performance suggests that the standalone bank remains the main engine of growth (70 percent contribution to consolidated profitability) followed by Kotak Mahindra Prime (car finance NBFC), Kotak Securities and Life Insurance. The 33 percent jump in consolidated profitability came on the back of 40 percent growth in the bank, 137 percent in Kotak Securities and 31 percent in life insurance. Qualitatively, however, even the mutual fund business has shown improved performance.

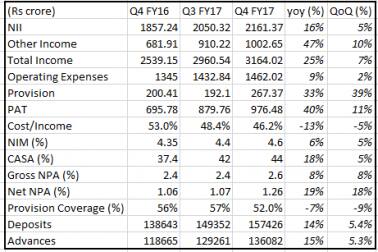

The fourth quarter earnings of the standalone bank was driven largely by non-interest earnings, which grew 47 percent. While fee growth was a predictable 24 percent, the non-fee component had an adjustment: FY16 included reversal of income of Rs 62 crore that has optically distorted the number resulting in a huge reported growth in the non-fee component.

Net interest income growth was a modest 16 percent, on the back of 15 percent increase in advances and 20 basis points improvement in margin.

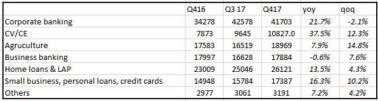

While the growth in advances was relatively modest compared to peers, within advances corporate banking and CV (commercial vehicles) appear to have grown faster indicating that the bank is gaining market share in these businesses. In fact, with the growth in balance sheet, the share of corporate lending book has increased to 59 percent from 56 percent and retail has fallen from 44 percent to 41 percent. The management did bring to the notice of the investors the competitive pressure in most of the retail products.

In terms of deposits, the strong franchise that Kotak has built is reflecting in the numbers. While the overall deposits growth was a more moderate 13.5 percent, CASA (current and savings account, low cost deposits) grew 31 percent and now forms 44 percent of deposits. The strong liability side will help Kotak garner market share in the corporate lending as competitors vacate this space on account of their asset quality woes.

On asset quality, while the numbers look a tad worse than the previous quarters, the same is on account of excessive caution adopted by the management. The gross and the net NPA (non-performing assets) of the bank grew by 13 percent and 25 percent, respectively and stood at 2.6 percent and 1.26 percent.

According to the management, while certain assets (mainly inherited from erstwhile ING Bank) were standard, they decided to recognise all those accounts where there is still inherent weakness as non-performing in this quarter. So the number is not an indication of any overt weakness in asset quality.

The bank had nothing to declare under “RBI’s new divergence criteria” and restructured and SMA2 (special mention accounts) stood at minuscule 0.07 percent and 0.10 percent, respectively. In FY17, Kotak Bank had not transferred assets to ARC (asset reconstruction companies), no 5/25, and no new CDR.

So, in this picture perfect result what’s the concern?

While the bank deserves kudos for the consistently superior performance, we are intrigued by the drop in business momentum. Is it excessive caution, or is it the legacy issues of the merger that’s still not over?

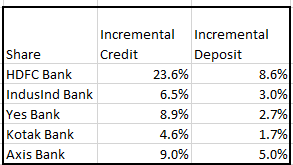

If we compare the business growth numbers – deposits as well as advances of Kotak Bank with its peers that have declared their numbers so far, it throws up quite a few interesting insights. Kotak’s share in incremental deposits of the system is at 1.7 percent which is much lower than HDFC Bank’s 8.6 percent. In incremental credit, Kotak’s share is much lower than HDFC Bank. While Kotak has a healthy capital position, how should the market read into such caution? Managing Director Uday Kotak is cautious by nature and has made the right calls in the past, so on the face of it, it may be best to trust his judgement.

The bank has already announced its intention to raise Rs 5300 crore that will augment its Tier I capital to 18.5 percent and help the bank to participate in the bad loan resolution problem in a big way and provide the requisite dry powder for inorganic growth.

With a savvy promoter, the way forward looks exciting. At the current price, the stock trades at 4X its adjusted book for FY18. Any correction in the market provides an opportunity to accumulate this high quality franchise for a steady double-digit return.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.