January 17, 2018 / 16:18 IST

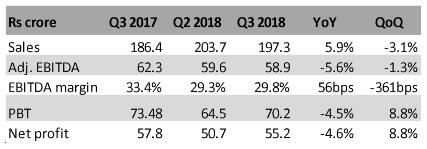

Bajaj Corp, leading manufacturer in the light hair oil segment (61 percent of market share), posted a decent set of numbers for their domestic business in Q3 FY18 results. International business remains a worry but investor attention was directed to the strategic announcement from the company in form of Mission 2020. It aims at becoming diversified FMCG company by 2020 and thus, presents itself a tall asking order. And so execution remains the key.

Q3 2018: Sequentially improved gross margins

Story continues below Advertisement

Mission 2020Bajaj Corp envisages to become complete FMCG company by the year 2020, wherein company would launch new products every quarter. New products are expected to be gross margin-accretive mainly in hair care, skin care space and then expanding into other categories. The idea is to move from a largely a single product company to a diversified FMCG company.Other encompassing idea which management highlighted in the analyst call is that Bajaj Corp is working on improving efficiency in terms of communication (higher advertising spend) and distribution (sales force automation/direct reach in distribution).OutlookWe are encouraged by the company’s Mission 2020 which if executed rightly can alleviate a key business risk for the company i.e. dependence on one single product/category. In this regard, successful pilot distribution for “No Marks” and relaunch of Brahmi Amla is commendable as company looks to diversify.While stock has rallied 35 percent, since lows in August’17, it is currently trading at a reasonable multiple of 35.7x trailing earnings. However, now onwards execution is the key. New product launches, positioning, distribution channels re-alignment are the focus areas. Also, as the company indicated, historical EBITDA margin range of 30% -35%, would be difficult to maintain as the company would also spend on innovation and promotion.

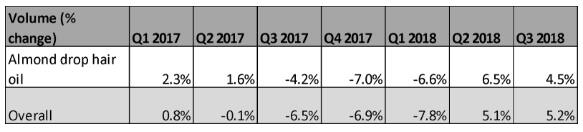

Further, overall volume growth for the traditional business is dependent on rural recovery, repair in international business, distribution and competition. Aspect about competition remains relevant for some key categories in FMCG like hair care and hence it remains to be seen if trend towards down trading gets arrested and premiumisation picks up.Overall, we are positive on the strategic shift and wait for more details on product launches and implementation before getting constructive on the stock.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!