The capital ratios of Indian public sector banks (PSB) are currently adequate, not just to absorb shocks, but also to augment credit growth, analysts and experts told Moneycontrol. A large part of this has to be attributed to the government’s capital infusion in some PSBs over the years and the ability of these lenders to raise funds from the equity and debt markets, said analysts.

To put it in perspective, PSBs raised a total of Rs 1.42 lakh crore from the market in the form of both equity and bonds during FY20 to FY22, Minister of State for Finance Bhagwat Karad said in response to a lawmaker’s question in Parliament on July 26. Out of this, Rs 32,293 crore was raised in FY20, Rs 58,697 crore in FY21, and Rs 50,719 crore in FY22, the Parliament paper showed.

“On the capital front, all PSBs have a cushion of more than 100 basis points over the minimum regulatory Tier 1 capital requirements. The government’s capital infusion into PSBs has ensured that the balance sheets of these lenders have improved,” said Krishnan Sitaraman, Senior Director and Deputy Chief Ratings Officer at CRISIL Ratings.

“There is also a steady improvement in profitability visible for banks, and that is expected to continue on the back of higher credit growth and rising interest rates.”

What are the norms?Capital acts as a buffer in times of crisis or poor performance by a bank. Sufficiency of capital also instils depositors' confidence in the bank and prevents systemic risks. Not just the government, the Reserve Bank of India (RBI) as the regulator has also been very particular that banks maintain a certain level of capital on their balance sheets.

According to the RBI, scheduled commercial banks are required to maintain a minimum Capital to Risk Weighted Assets Ratio (CRAR) of 9 percent on an ongoing basis. This ratio measures a bank's financial strength by using its capital and assets. The capital funds, according to the RBI, shall consist of the sum of Tier I capital and Tier II capital.

In addition to the minimum Common Equity Tier 1 capital of 5.5 percent of risk weighted assets (RWA), banks are also required to maintain a capital conservation buffer of 2.5 percent of RWA in the form of Common Equity Tier 1 capital.

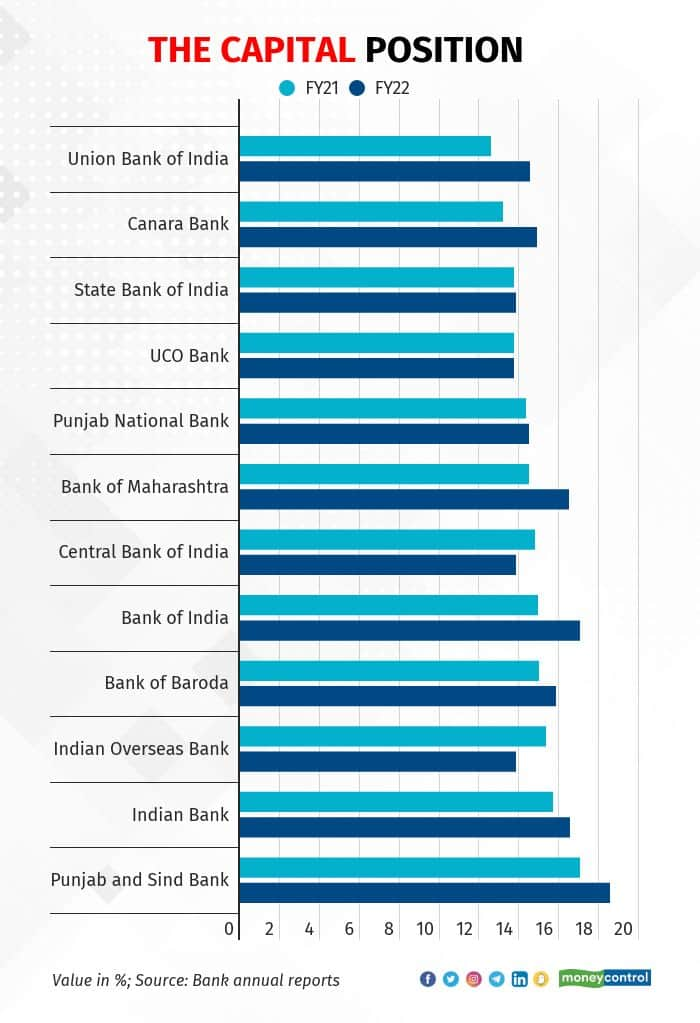

What is the capital position now?As of March 2022, most PSBs had comfortable CRAR. For instance, State Bank of India’s CRAR stood at 13.83 percent as on March 31, up from 13.74 percent a year ago. The CRAR of smaller lenders like UCO Bank, Punjab & Sind Bank and Central Bank of India stood at 13.74 percent, 18.54 percent and 13.84 percent, respectively, according to the banks’ annual reports.

As per the RBI’s Financial Stability Report released in June, macro-stress tests for credit risk reveal that scheduled commercial banks are well-capitalised and all banks would be able to comply with the minimum capital requirements even under adverse stress scenarios.

RBI officials, including Governor Shaktikanta Das, had repeatedly asked banks to raise sufficient capital buffers to deal with COVID-related shocks. Banks had raised adequate debt and equity capital, and made extra provisions for dealing with bad assets. That has protected the balance sheets of PSBs and improved their profitability in recent quarters.

“PSBs have a good amount of pre-provisioning operating profits, and credit costs are expected to come down with COVID subsiding, which will help the profitability, and, in turn, accretion to capital,” said Aditya Acharekar, Associate Director at CARE Ratings.

“Although, we see some stress in the restructured book, contingency provisions held by banks would help banks maintain profitability in case of higher slippages,” Acharekar added.

CRISIL Ratings’ Sitaraman added that based on the current capital position and balance sheets of PSBs, these lenders are expected to raise funds from the market through Tier 1 or Tier 2 bonds or even through equity capital. The appetite of debt capital market investors for bank bonds has increased in recent quarters with the strengthening of the balance sheets, he said.

Moneycontrol had reported on July 18 that recent additional tier 1 bond issuances of Canara Bank, Punjab National Bank and Union Bank had received strong demand from the market.

Strong balance sheetsThe government has also been recapitalising banks to strengthen their capital positions. However, experts have said that this may not be beneficial for the lenders in the longer run.

“If the infusion of funds is made to enable PSBs to meet the capital adequacy norms, this may not be the best solution for better performance of public sector banks,” said Srinivas BR, partner at DSK Legal. “To address this issue, if an advisory from the RBI on the requirement to infuse additional funds in any public sector bank is made a pre-condition, the government will be able to take an informed decision on whether or not to infuse funds, and if yes, with what conditions attached.”

Already, the government has infused capital amounting to Rs 2.86 lakh crore in PSBs during the last five financial years from FY18 to FY22. There is no fresh provision for capital infusion into PSBs in FY23’s budget amid improved capital ratios. At the same time, in March 2018, the gross NPA ratio for PSBs was at 14.6 percent, which now stands at 7.3 percent as of March 2022.

Analysts do not see the need for government support in terms of recapitalisation, going forward. Given that deposit growth has been lower than credit growth so far this fiscal, banks may explore the option of increased borrowing via avenues like certificates of deposits, wholesale term deposits and infrastructure bonds, in addition to raising deposit rates to give a fillip to mobilising retail deposits, rather than depending on government support, they said.

“It is highly plausible that PSBs will maintain their growth trajectory despite the government's capital infusion,” said Sameer Jain, Managing Partner, PSL Advocates & Solicitors.

“The major improvements are credited to restructuring and reviving of non-performing assets (NPAs) which is ending PSBs’ legacy of bad loans (due credit to the Insolvency and Bankruptcy Code). The need for government intervention may not be required if PSBs are able to raise capital from the market and their own assets,” Jain added.

CRISIL’s Sitaraman added that the trend of declining NPAs will continue this fiscal.

“This is largely because we do not expect any material slippages in the large corporate book and some of the legacy NPAs are expected to be transferred to the National Asset Reconstruction Company Ltd or NARCL, this fiscal,” Sitaraman said. He expects gross NPA ratio of PSBs to fall below 6.5 percent in FY23.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.