To understand the predicament OPEC+ is facing, start with a visit to an Ikea store.

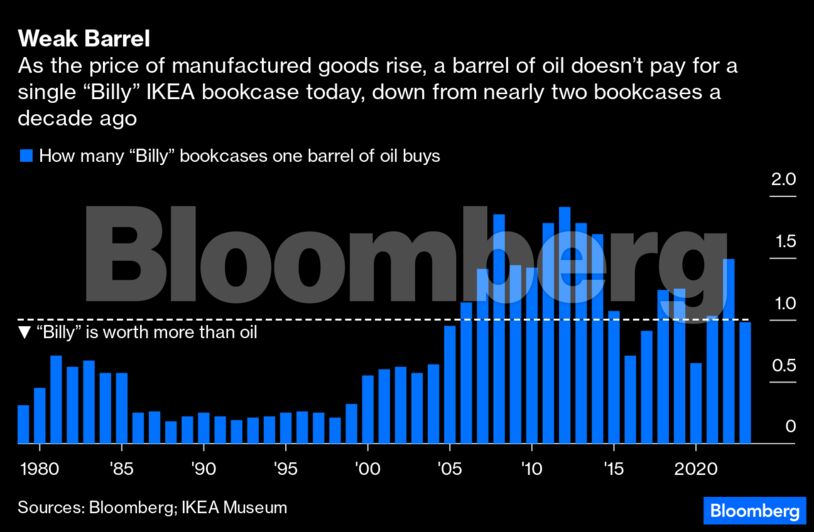

A decade ago, if the Swedish furniture giant had accepted crude as payment, the oil cartel could have outfitted a good portion of the conference room where its ministers will be gathering on June 4 in Vienna — their first face-to-face meeting since the pandemic started — with a single barrel. Today, it wouldn’t even buy a humble bookcase.

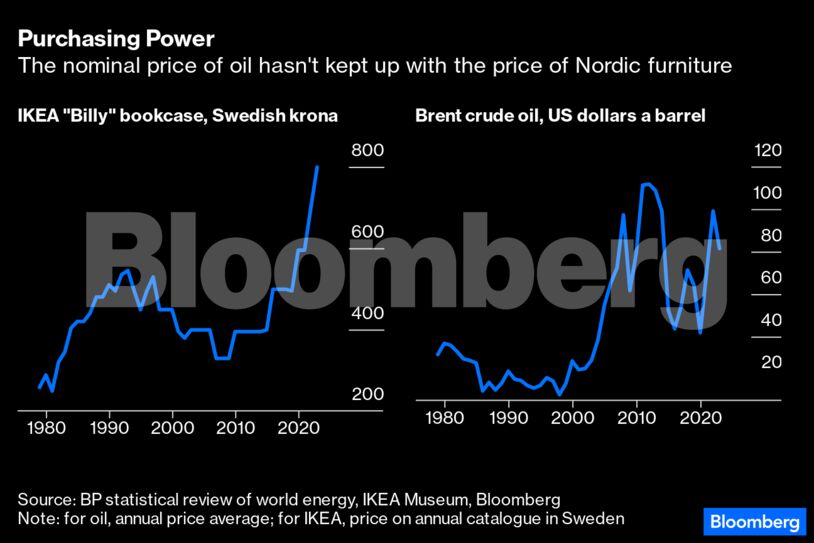

It’s not just that oil prices have fallen 25% since late last year to $75 a barrel, but that relative to the price of manufactured goods oil is even cheaper.

Typically, commodity producers battle a treadmill that’s known as the Prebisch-Singer hypothesis, for the two development economists who proposed it in the 1950s. In simple terms, it says that over the long-term, the price of primary goods, such as commodities, falls relative to the price of manufactured goods. No matter how high producers raise prices, the cost of everything else eventually climbs faster That’s why Raul Prebisch and Hans Singer argued that commodity-producing countries must diversify their economies, industrialising if they wanted a healthier future.

True, over shorter periods, the price of commodities can outstrip manufactured goods, improving the terms of trade of resource-rich nations. For much of the early 2000s, that’s precisely what happened. In 2010, Glenn Stevens, then the governor of the Reserve Bank of Australia, used a graphic metaphor to illustrate the point — and why Australia, rich in minerals, natural gas and grains, was benefiting.

“Five years ago, a shipload of iron ore was worth about the same as about 2,200 flatscreen television sets. Today it is worth roughly 22,000 flatscreen television sets,” he said.

Stevens was speaking at the peak of the commodities super-cycle, when the cost of iron ore, oil, copper and other natural resources jumped thanks to the voracious demand of China. More recently, the terms of trade have changed dramatically: Commodity prices are still high by historical terms, but they aren’t keeping up with global inflation.

Rather than using flatscreen televisions as a benchmark, whose price goes up and down depending on evolving technology, I prefer a different yardstick: IKEA’s “Billy” bookcase. In production since 1979, the spartan shelving unit is everywhere – and thanks to the IKEA Museum, which maintains an online collection of yearly catalogues, its price can be traced back 44 years.

For OPEC+ nations, which import most of their manufactured goods, inflation has become a major issue. When adjusted by inflation, the $75-a-barrel oil of 2023 has the same purchasing power as the $55-a-barrel a decade ago. Back then, nominal oil prices were above $100 a barrel.

To be sure, OPEC+ isn’t the only reason inflation is elevated. Perhaps it isn’t even the biggest reason. Perhaps it was Western central banks’ dawdling before raising interest rates; or the impact of COVID-19 messing with global supply chains, or the Russian invasion of Ukraine, together with US-European sanctions, which all contributed to boost prices even more.

Yet, OPEC+ is racing on a speedy treadmill. The period between 2000 and 2020 saw OPEC+ winning purchasing power. The next decade may be the opposite. As the US Federal Reserve has found, inflation is a complex and determined nemesis.

Javier Blas is a Bloomberg Opinion columnist covering energy and commodities. Views are personal, and do not represent the stand of this publication.Credit: BloombergDiscover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.