The growth in the assets under management (AUMs) of mutual funds as well as the number of investor folios has been very impressive in the recent years. Sebi, the regulator of markets and mutual funds, has also been keeping up with the pace of the growth and developments in the mutual fund industry to ensure that investors understand the product clearly, and make well-informed decisions. It has been Sebi’s endeavour to see that the schemes stay true to their name and characteristics.

Diversification is the most powerful idea in investments. The concept of mutual fund investing is built on the theme of diversification at a low cost. There are funds that provide the benefits of diversification within a particular capitalisation range such as large cap funds, mid-cap funds, and small cap funds. Within the equity funds category, there are funds which invest across capitalisation.

Sebi’s circular issued in October 2017 on ‘Categorization and Rationalization of Mutual Fund Schemes’ defined multi-cap funds as ones that could invest across large cap, mid cap, and small cap stocks with a minimum of 65 percent investment in equity, and equity-related instruments.

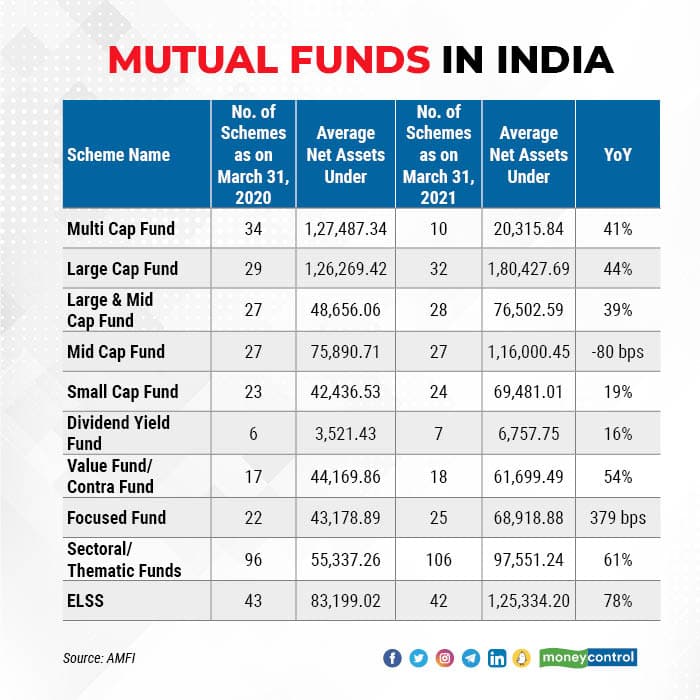

Given the opportunity to invest in a larger securities universe ranging across the capitalisation, these schemes became quite a popular product. As on March 31, 2020 there were 34 multi-cap schemes, the third-highest number after sectoral/thematic funds and ELSS within the (equity) growth. Clearly a larger number of asset management companies offered multi-cap schemes than large cap or mid-cap or small cap schemes. Also multi-cap funds were managing Rs 1,27,487.34 crore, the highest AUM within the equity/growth category.

In 2021, the situation changed dramatically, as can be observed in the table above. The reason could be traced to the Sebi circular issued on September 11, 2020, regarding the asset allocation of multi-cap funds. In order to diversify the underlying investments of multi-cap funds across the large, mid and small cap companies, and be true to the label, Sebi decided to partially modify the scheme characteristics of multi-cap funds. It mandated that at least 75 percent investment in this category is made in equity, and equity-related instruments, in the following manner: at least 25 percent in large cap companies, at least 25 percent in mid-cap companies, and at least 25 percent in small cap companies. The remaining 25 percent can be invested in any of the above three categories.

This move by regulator was to make multi-cap schemes true to their label. Ideally multi-cap funds should provide exposure across the capitalisation range. However, the mutual fund industry viewed it differently. It views it as constraining the allocation freedom of the fund managers. The multi-cap funds now have to necessarily invest 25 percent in small cap stocks. Also, they cannot have more than 50 percent exposure into large cap stocks.

Following the suggesting of mutual fund advisory committee, on November 6, 2020, Sebi re-introduced multi-cap funds in their earlier avatar, naming them flexi-cap funds as a new category under equity schemes. As true to its name, flexi-cap funds can invest across capitalisation ranges without any ceilings.

A flexi-cap fund is defined as an open-ended dynamic equity scheme investing across large, mid, and small cap stocks with a minimum investment of 65 percent of total assets in equity, and equity related instruments. Fund managers have the option to convert an existing scheme in to a flexi cap scheme. Many fund houses chose to convert their multi-asset funds into flexi-cap funds, as greater flexibility for allocation led to better performance if the fund manager had the superior forecasting skills.

As on April 30, 2021, there were 26 flexi-cap funds managing around Rs 1,58,484.39 crore. As evident clearly, many asset management companies chose to believe in the judgement of their fund managers over the regulatory judgement. A year later, it is worth examining to see whether it made sense from a performance perspective.

As it can be observed from the above table, out of 26 funds, 17 flexi-cap funds have underperformed the benchmark. Two funds produced returns very close to the benchmark, and just seven outperformed the benchmark. The benchmark for flexi-cap funds is either the S&P BSE 500 total return index or the NIFTY 500 total return index. The benchmark for all the eight multi-cap funds is the Nifty 500 multi-cap 50:25:25 total return index. Five out of eight funds have outperformed the benchmark.

Against 40 percent of the flexi-cap funds outperforming the benchmark, over 60 percent of the multi-cap funds have generated returns higher than the benchmark. This makes it evident that the regulatory sense is better than fund manager sense when it comes to products that invest across capitalisation ranges for rewarding investors.

(Rachana Baid is Professor, National Institute of Securities Markets. Views are personal, and do not represent the stand of this publication.)Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.