Anubhav Sahu Moneycontrol research

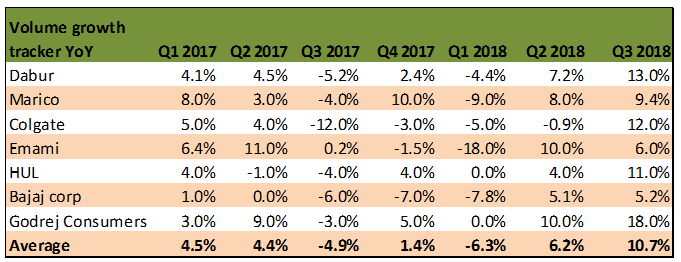

Marico’s quarterly result underlined an improving volume growth trend in the FMCG sector guided by better rural demand and base effect. Though volume growth was lower than expected, the market share gain in Parachute hail oil was positive despite recent price hikes. Having said that, margin pressures and competition remains a key aspect to watch for.

Higher raw material prices weighs on Margins

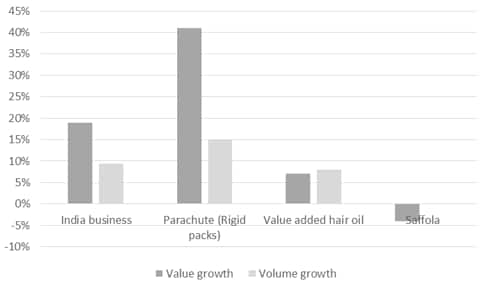

Marico in its Q3 FY18 sales posted a 15.1 percent YoY growth aided by volume growth of 9.4 percent, below consensus expectation of lower double digit growth, in the India business. Gross margin sharply contracted on account of higher copra prices (+91% YoY and 21% QoQ).

As a result, EBITDA margin contracted by 70 bps YoY to 18.6 percent (-70 bps YoY) although partially offset by lower advertising and moderate employee cost.

Company highlighted the lower advertising spending was mainly due to international business and in the domestic business advertising spending has increased by 15 percent YoY.

Parachute Oil – Moving towards price hikes

Marico’s key brand Parachute (rigid packs) continue to witness volume pick up (15 percent vs. 12 percent YoY in Q2 FY18) partially benefitting from lower base (-1 percent volume growth in Q3 2017) and registering a market share gain.

Interestingly, after resisting price hikes for the first half of FY18, company has undergone two consecutive 10 percent price hikes to partially pass on the spike in copra prices. Pricing strategy has so far worked for the company wherein focus has been on volume sustenance followed by price hikes.

Chart: Q3 2018 value/volume mix

Saffola: Business strategy under review

Among other categories, Saffola edible oils remains a problem area. The segment witnessed a flattish volume growth and a decline of 4 percent in value terms. Value de-growth was partially on account of price reduction to pass on the GST benefits. Further, high CSD dependence has also impacted the business in this product category. It is noteworthy that company is undergoing a business strategy review for it.

International operations: Weakness in Vietnam business

International business sales was up 9 percent on the constant currency basis aided by Bangladesh business (44% of international business) but partially offset by sales decline in Vietnam business (South East Asia business: 28% of international business). Macro conditions remain tough in South Africa and business revival seems fragile in MENA region.

Green shoots visible for rural economy

Management highlighted improving sentiments in rural economy leading to better volume growth. However, company called it too early to call a trend for rural recovery.

While there has been a good mix of volume and value, overall result is below our expectations. Higher raw material prices have prompted company for consecutive prices hikes in Parachute hair oil. Though so far company has been not seen any negative impact on the market share, it need to be seen it’s sustenance in coming quarters. Competition from Patanjali and Dabur still needs to be watched for, which may get intensified as the trade channel improves.

Among the key monitorables are copra prices (Company expects lower prices in H2 FY19) and recovery in Saffola refined oil and Vietnam business (Company expects recovery in Q1 FY19). While Marico’s stock is trading (41x FY19e earnings) at discount to the market leader, earnings visibility is marred by margin pressures, in our view.

For more research articles, visit our Moneycontrol Research Page.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.