On April 2nd, 2025, US President Trump announced tariffs on all countries exporting to the US. This is a live situation – retaliations and counter retaliations have since been announced, and the markets across the world continue to be whipsawed.

Earlier this month, S&P500 Index, that has a market capitalisation of $50 trillion, lost a whopping $4.5 trillion in value over two days. Globally, politicians, central banks, business leaders and investors are scrambling to calibrate the damage and devise an appropriate response.

I believe that with geopolitical entropy rising, India stands out amongst the large economies as being ‘antifragile’.

"Antifragility is beyond resilience or robustness. The resilient resists shocks and stays the same; the antifragile gets better" - Nassim Taleb.

In his bestselling book, Antifragile, Nassim Taleb describes an antifragile system as the one that can not only withstand stress and shocks, but it also thrives because of them. Taleb states that for the system to be antifragile, it must have exposure to stressors, and it must allow for trial, error and evolution. He contrasts such a system with the fragile ones – the centrally controlled, the overprotected or the over-optimized systems.

Surviving multiple shocks

India is not a mollycoddled economy that enjoys the patronage of global superpowers, membership of elite trading blocs, consideration of global ratings agencies or generous portrayal by western media. It is routinely exposed to sizeable stressors – taper tantrum, demonetization, NBFC crisis and Covid pandemic. And with every crisis, India and Indian businesses course-corrected and emerged stronger.

The current dislocation in geopolitics is no different.

First order impact – India is not too negatively impacted

# Proposed tariffs do not have a material negative impact for India: India’s trade surplus with US is only $45bn. India exports $87bn to US and India imports $42bn from US for a total trade partnership of $129bn. This is low for a country with GDP of $4 trillion with nominal growth of over 10%. Trump’s proposed 26% tariff on India is lower than the proposed tariffs in China, Vietnam, Taiwan, Bangladesh, South Korea – and these countries are majorly export-dependent economies. There’s an estimated 30-50bps hit to the GDP if the tariffs go ahead as announced. India has not retaliated to US tariffs and is working to negotiate a deal with President Trump.

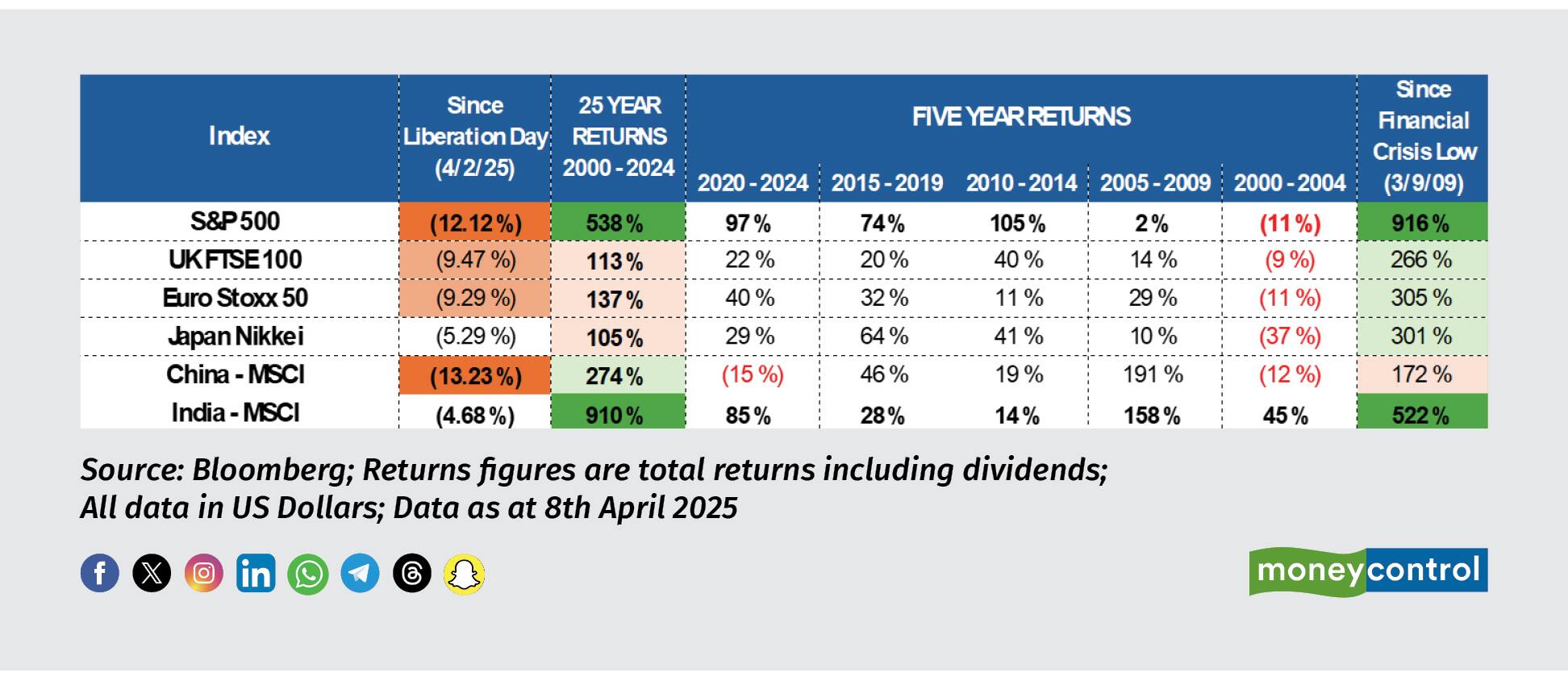

So, on both an absolute and relative basis, India is not materially hurt by the tariff announcements.# Domestic investors continue to provide strong support to the Indian stock markets: India has been the best performing stock market since President Trump’s tariff announcements. This is because of the strength of its domestic equity inflows. In the first few days of April, foreign investors redeemed a whopping $3bn from Indian equity markets, but domestic investors deployed $2.5bn and cushioned the blow. Year-to-date, foreign investors have redeemed $16.5bn out of India and domestic investors ploughed in $24bn. The domestic investors are shifting their savings from physical assets to financial assets. This is a structural trend as currently less than 5% of the population invests in stock markets.

At 16.8% of the Indian equity markets, the foreign investor ownership is at an all-time low, yet Indian equity markets are resilient due to domestic demand. This is comforting.

# Indian stock markets are less correlated to the US and other developed countries: India was the best performing market from 2000 to 2005 when US and all other key markets were reeling from the aftermath of the internet bubble. India was also one of the best performing markets from 2005 to 2009 when US and developed countries were recovering from the financial crisis. Since the Covid pandemic, India has outperformed other major stock markets (except US) by a wide margin. This is remarkable given the dollar strength has had a material negative impact on Indian rupee since Covid.

Over the next few months, we expect lower oil prices, weaker-to-stable dollar and stable to lower interest rates in the US – all positive signals for Indian economy and the Indian equities.Second order impact – India to emerge a beneficiary of the dislocation in geopolitics

"The enemy of my enemy is my friend" - Old proverb

"Never, ever, think about something else when you should be thinking about the power of incentives" - Late Charlie Munger

# US Pension Funds need to rethink how they allocate capital: Based on my conversations with US investors, there is an increasing sense of discomfort around investing in China. But they cannot deviate too much from the benchmark against which they are measured today. This is untenable. China and India merit their own allocations just like Japan and the UK.

Are Americans comfortable with the idea that when they invest 100 dollars in an emerging market ETF to diversify their US exposure then about 31 dollars get invested in China? Is a US Pension fund comfortable getting India exposure via an EM Fund manager where for every three dollars they invest in India five dollars get invested in China!# American CEOs need to answer to their Boards: Trade war during Trump’s first presidential term and the Covid pandemic exposed the concentration risks in global trade. The Boards will now be asking their CEOs tough questions about their China exposure – both for revenue and from a supply chain perspective. India is a natural, viable and scalable alternative on both counts. India is an English-speaking democratic country that has friendly commercial ties and strategic military ties with the US. India has a large and growing engineering and technology talent pool and low costs. India has a growing middle class with increasing spending power. Since the pandemic, CEOs of many large US corporations have been exploring options in India, and I expect these efforts will only accelerate now as US companies seek new markets and new suppliers for their products.

Apple established manufacturing footprint in India post-Covid and now produces 25% of its iPhones in India and counting. India also ranks as its top five market in just two years. Contrast this with the fact that iPhone sales declined 17% in China last year and I would be surprised if this year it is not worse.# European politicians need to answer to their voters: Since President Trump’s advocacy of an America-first policy, the European voters are increasingly questioning their elected representatives why they are not being protected against an onslaught of Chinese goods. The European auto industry and other engineering-related industries have been suffering from heavy taxes, environmental regulations and the generous worker benefits required of them and are increasingly uncompetitive against their Chinese counterparts that operate unencumbered by such considerations.

Last month, EU Commission President, Ursula von der Leyen, visited India along with all (!) of EU’s 26 Commissioners to discuss free trade agreement with India. Such a scale of the EU delegation to a country for a bilateral discussion is unprecedented and denotes a marked shift in the attitude of Europe towards India.We are living in historic times. Century-old alliances are being tested. Countries are holding each other accountable for protecting shared values. Global trade partnerships are being redrafted. Two wars rage on and the threat of serious escalation is never too far off the mind. South China Sea is one diplomatic mistake away from becoming the third war front.

My contention is that India is “antifragile” – it will not only emerge relatively unscathed from the tariff-related turmoil, but it is also going to benefit from the displacement in the medium to long term.

(Sachee Trivedi is Founder & CIO, Trident Capital Investments, Luxembourg.)

Views are personal and do not represent the stand of this publication.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.