The escalation of US tariffs on most major global trading partners, particularly Asian economies, has exerted significant pressure on regional trade and currencies.

India and Indonesia have been among the hardest hit, with global risk aversion and a strong US dollar weighing on both. For India, however, domestic factors have intensified the strain, making the rupee’s depreciation more pronounced.

Although India and China face similar elevated tariff levels, the divergence in their currency performance is stark. The rupee has emerged as the worst-performing currency in Asia this year, while the Chinese yuan has remained relatively stable. This resilience stems from the People’s Bank of China’s tight management of the yuan through daily fixings, strategic interventions, and the support of extensive foreign exchange reserves.

Additionally, China’s capital controls curb speculative flows, allowing policymakers to prioritise stability, inflation management, and the strategic objective of renminbi internationalisation, an advantage freely floating Asian currencies do not enjoy.

Both the Indian rupee and the Indonesian rupiah have weakened, but the degree of depreciation highlights a gap: the rupee has fallen 4.35 percent so far this year, compared with a 3.98 percent decline in the rupiah. Economists note that while global factors have influenced both currencies, India-specific challenges, such as weaker capital inflows and persistent external vulnerabilities, are deepening downside pressure on the rupee.

The rupee’s slide in recent months culminated in a breach of the 91 mark to the US dollar, prompting the Reserve Bank of India (RBI) to intervene. While such measures may temper sharp movements, the broader trend reflects a combination of global headwinds and domestic imbalances that continue to shape currency dynamics.

Capital flows emerge as the biggest differentiator

According to Gaura Sengupta, Economist at IDFC First Bank, the sharper depreciation in the rupee is primarily driven by a significant slowdown in capital inflows.

Sengupta added that, overall, FPI (foreign portfolio investment) inflows into emerging markets has picked up to $219 billion in FYTD26 (till November) vs $175 billion (till November FYTD25). Meanwhile, for India, net FPI inflows has slowed to $0.4 billion in FYTD26 vs $7.5 billion in FYTD25. “The slowdown in inflows into India reflects moderation in return on investment, which is captured by the slowdown in nominal GDP growth.”

This is in stark contrast to Indonesia, where currency weakness is more closely linked to outflows driven by domestic economic challenges. For India, however, the moderation in rate of return on investment, reflected in a slowdown in nominal GDP growth, has weighed on foreign investor appetite, intensifying rupee pressure.

Apart from this, many other Asian currencies weakened against the US dollar as investors sought safer assets and a stronger dollar pushed emerging-market FX lower, after the imposition of tariffs.

However, there were episodes of resilience and recovery for certain currencies when tensions eased or alternative drivers emerged.

US trade deal uncertainty leaves India exposed

The uncertainty around the India–US bilateral trade agreement (BTA) has been an additional drag on sentiment. Aditi Gupta, Economist at Bank of Baroda, highlights that unlike Indonesia, which has already signed its deal with the US, India’s negotiations have faced repeated delays, keeping investors waiting on the sidelines.

India also faces a higher dependence on US markets as roughly 20 percent of India’s exports are US-bound, compared to a lower reliance for Indonesia.

As Gupta notes, “The pressure on Indian rupee is much more pronounced due to the lack of clarity on the trade deal with the US,” even though domestic growth remains robust.

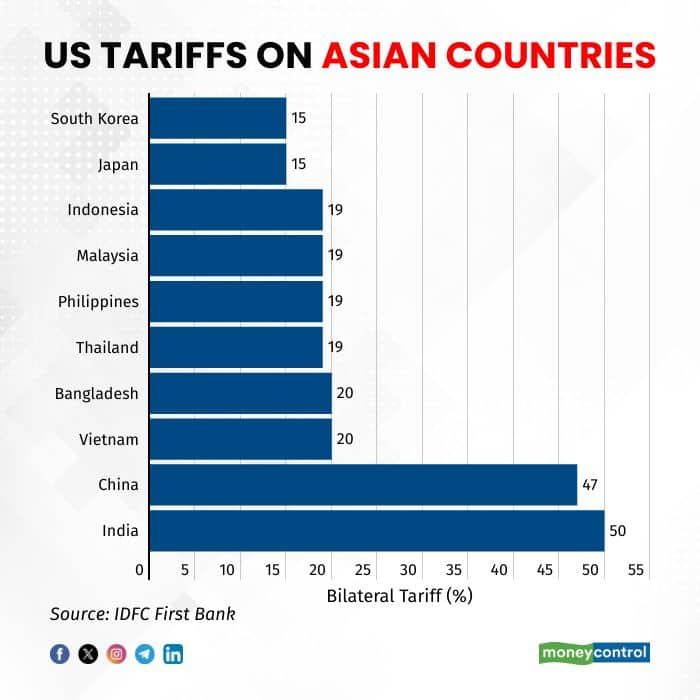

India stands out in Asia for facing some of the steepest bilateral tariffs, with the rate hitting around 50 percent, higher than many of its regional peers. This elevated tariff level places India second only to China, which faces a 47 percent rate, while countries like Bangladesh and Vietnam are significantly lower at 20 percent, and South Korea and Japan are as low as 15 percent.

Such a stark contrast underscores the disproportionate tariff burden India carries in Asian trade flows. It also raises questions about how tariff structures may influence India’s export competitiveness and trade negotiations, especially at a time when global value chains are shifting and countries are re-evaluating supply chain dependencies.

What further complicates India’s position is that, unlike export-heavy economies that rely strongly on the US market, such as Mexico or Vietnam, whose exports to the US account for more than 20 percent of GDP, India’s exposure is relatively modest at about 2 percent. This means India is simultaneously facing higher tariffs yet deriving a relatively smaller share of economic output from the US market, reducing its leverage but also its vulnerability.

Tariff structures create contrasting risk profiles

Tariff differentials are another factor shaping market perception. India currently imposes tariffs as high as 50 percent on US imports, significantly above many of its Asian counterparts, including Indonesia.

This has led to fears of export disruptions, although the impact so far has been less severe than expected. After a dip in October, outbound shipments to the US rebounded sharply in November, supported partly by front-loading of exports earlier in the fiscal year. That resilience has helped India’s current account deficit forecast hold near 1 percent of GDP for FY26, Sengupta notes.

Still, economists warn that if a trade deal is not concluded, the FY27 CAD could deteriorate, potentially widening the depreciation gap further.

RBI’s constrained defence adds to volatility

While central banks of India and Indonesia have intervened to smoothen volatility, the RBI faces a unique challenge: a large forward book and elevated net dollar shorts. This restricts the RBI’s ability to deploy buy-sell swaps to sterilise spot intervention.

As Sengupta puts it, “RBI’s ability to defend the Indian rupee is limited. Hence, even with a trade deal, we expect depreciation pressures to persist, but at a more moderate pace.”

Gupta adds that the RBI has shifted to a more cautious intervention stance, allowing some depreciation to support export competitiveness while containing disorderly moves.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.