V-Mart is a medium-sized hypermarket value retailer that caters primarily to aspirational customers in tier-1, tier-2 and tier-3 cities of India. The company sells apparel, general merchandise and groceries through its 171 outlets (total retail area of 14.4 lakh square feet) across northern, north-western and eastern India.

Growing share of private labels, volume-led revenue growth, rationalisation of costs, an upgrade of technological infrastructure, and network augmentation will pave the path ahead for V-Mart. However, most of these positives seem to be factored into the price of the stock, thus limiting its potential returns in the near term.

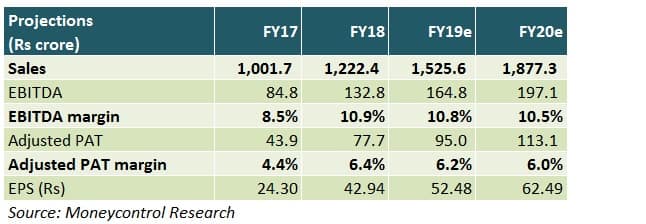

Performance reviewV-Mart fired on all cylinders in the quarter and year ended March 2018. The company registered healthy year-on-year same-store sales growth of 9 percent and 7 percent, respectively, for the quarter and the year. Addition of 30 outlets during the year, strong marketing initiatives, and refurbishment of stores were some of the other factors that contributed to the growth in top line.

Steps to manage costs (on fronts such as merchandising, technology, procurement and distribution), limited promotional expenses, higher proportion of full-priced sales (on account of lower discount rates and days), and reduction in clothing shrinkage led to an expansion of margins.

Shrinkage refers to inventory unsold and written off due to defective quality, sales returns, or stocks sold at heavy discounts at the end of a season. Clothing inventory cannot be carried forward to the next financial year, given the change in seasons and fashion trends.

V-Mart’s own brands, which accounted for roughly half its sales in FY18, will be a priority area because of their high-margin nature. The company’s strategy to maintain average selling prices underscores its inclination to keep its EBITDA margin range-bound (10-11 percent) by passing on price benefits to buyers.

Tier-4 focusTo capitalise on the growth of organised retail in previously-underserved geographies of India, V-Mart will expand its operations in tier-4 areas, particularly in north-eastern India. Owing to a high degree of price sensitivity in such regions, revenue growth will be volume-driven.

To expand its retail footprint in existing geographies, V-Mart’s management aims to grow its retail area by 15-17 percent in FY19. Besides targeting same-store sales growth of 8-10 percent, the company can leverage its in-house capabilities to offset the corresponding increase in staff costs and fixed overheads.

Working capitalConsidering the company’s robust cash flows, the emphasis during the current fiscal year will be on buying goods from suppliers at a lower cost in exchange for earlier clearance of dues. Furthermore, practices aimed at optimising inventory practices using consumer analytics and just-in-time buying should help improve margins in the long-run.

ShrinkagePeriodic stock audits and adoption of requisite information systems should help V-Mart keep a close track of garment shrinkage. The company only recently automated its packing and wrapping processes to reduce losses during the course of transit. Such cost savings should lead to improved gross margins.

Key risksAround half of V-Mart’s annual revenue comes from tier-3 towns, while tier-4 towns account for approximately 10 percent. In tier-3 towns, the company faces stiff competition from unorganised players. Disruptions in Uttar Pradesh and Bihar, which jointly make up for over 60 percent of the company’s total store count, could impact its financials as well.

Is V-Mart investment-worthy?Consistency in quarterly results and superior execution capabilities have resulted in V-Mart’s re-rating. Apart from the moats stated above, gradual discontinuation of low-margin grocery outlets, coupled with the ability of its new stores to break even quickly, will be decisive in driving the company's earnings growth in the upcoming fiscals.

The stock currently trades at a pretty demanding valuation of 38 times the company’s estimated earnings for FY20 estimated earnings. Nonetheless, we believe it still remains a long-term bet, considering the way consumption is on the rise in the Indian hinterland. Investors are, therefore, advised to buy the stock on any sign of weakness.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.