Anubhav Sahu Moneycontrol research

Thirumalai Chemicals, the second‐largest manufacturer of domestic Phthalic anhydride (PA), reported weak topline numbers in the June quarter amid plant shutdowns in both Ranipet and Malaysia. The project expansion updates though drew investor interest. On account of this, we pencil in improved volume growth from FY20 onward, though at a gradual pace.

At the same time, we remain wary about the product price realisation trend given the potential removal of trade protection measure and the limited pricing power of the chemical commodity business.

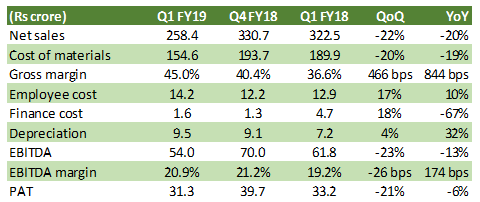

Q1 FY19: Sales volume impacted by the maintenance shutdown

The standalone business, which mainly consists of Phthalic anhydride reported a weak performance in Q1FY19 on account of a month-long closure of plant facility for maintenance. Net sales were down 31 percent year-on-year (YoY) but earnings before interest, tax, depreciation, and amortisation (EBITDA) margin improved 277 basis points (bps) YoY due to the better operating efficiency. The bottomline was less impacted due to lower finance costs.

Malaysian unit posted 22 lower sales quarter on quarter (QoQ) due to a plant shutdown.

Table: Consolidated financials

Source: company

Projects update

The company’s major plants are near optimum utilisation and hence, capacity expansion is the key driver for volume growth. In the case of PA, the company is going through a revamp at its Ranipet plant which will be complete by Q4FY19 and result in improved productivity and safety.

Further phase-1 (60,000 tonne) of PA project at Dahej, is expected to commence operation by May 2019. The company has an expansion plan for Dahej after phase-1 and together the PA capacity will increase from 140,000 tonne to 240,000 tonne.

In case of Maleic Anhydride (MA), Malaysian subsidiary has decided to enhance capacity by another 20,000 tonne to 65,000 tonne which will take another two years.

The expansion of food ingredients and derivatives plants are complete and operational now. This relatively high-margin business now contributes about 20 percent of India business sales. The company is also studying a plan to establish food ingredients and maleic anhydride plant in the USA with a key benefit of accessing cheap feedstock.

We expect near-term capacity expansion plans to lead to volume growth of 7-8 percent (CAGR) for next four years with the further upside possible from the acceleration in the phase-2 expansion of Dahej. We opine this is reasonable given the domestic industry growth rate of 4 percent annually and there is a scope for substituting imports in the domestic market.

However, this can change if there are any pricing and demand-supply disruptions caused by the removal of anti-dumping duty.

Anti-dumping duty on PA under review

As we have mentioned in our earlier note that Directorate General of Trade remedies has started the sunset review investigation concerning imports of PA originating in or exported from Korea, Taiwan, and Israel. Imports from these countries constituted about 56 percent of the imports of PA in FY17.

In our interaction, management representatives of both IG Petrochem and Thirumalai Chemicals have downplayed the risks citing that bulk of the PA imports are under advance license and do not attract anti-dumping duty. Under advance license, importers are obligated to export value added products within stipulated time period.

However, having said that removal of anti-dumping duty would make the product pricing more competitive. Particularly, it was mentioned that imports from Russia (Under anti-dumping till CY2020) need a closer watch which on account of higher state subsidy can potentially dump.

Outlook

The company’s turnaround in its business over the years has been remarkable which has partly been guided by improved end markets, operational efficiency and trade protection.

In the recent interaction with the management, a few business updates have been laudable. The balance sheet is leaner and the management plans to fund the upcoming projects from internal accruals.

Its near-term capacity expansion plan for PA would be on stream by FY20 onwards and in the first year of operations we assume 20 percent utilisation on account of plant stabilisation period and the time lag it might take to displace imports in the domestic market. Similarly, new MA capacity in Malaysia would be available in FY21. This means in the current year volume growth would be flat, at best, if the company is able to recoup volume growth lost in plant shutdowns.

As far as operating margins are concerned, we believe the company is at the upper end of margin range in this largely commodity business wherein more than 80 percent of revenue is from the chemical intermediate business. In fact, given the expansion plans, chemical commodity sales contribution is expected to increase from here. Further, cost of materials as a percentage of sales have nudged up recently though it has been offset by the operational efficiency.

In our projection for current fiscal, we have kept the operating margin at this upper end of 20.5 percent with the caveat that downside risk to it is there given the prospects for removal of anti-dumping duty.

Nevertheless, even if we assume cost management for the operations is maintained at current levels, the stock is currently trading close to the levels warranted for the commodity companies. Hence, we continue to remain on the sidelines until clarity emerges on higher supply headwinds.

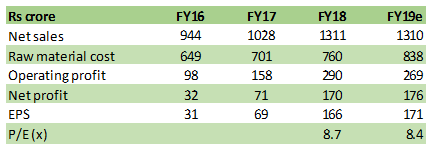

Financial projection

Source: Moneycontrol Research

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.