Sachin Pal Moneycontrol Research

A standout feature of this earnings season so far has been the strong performance by companies in the consumer space. Purchasing and spending was affected last year because of the Goods and Services Tax roll out. Consumers have now resumed spending on goods and services and this is feeding into the earnings of companies catering to the demand.

From a portfolio perspective, stocks of consumer companies are a good hedge when the macro picture is bleak, as is the case at present.

We have identified some midcap consumer companies which can deliver consistent growth in earnings.

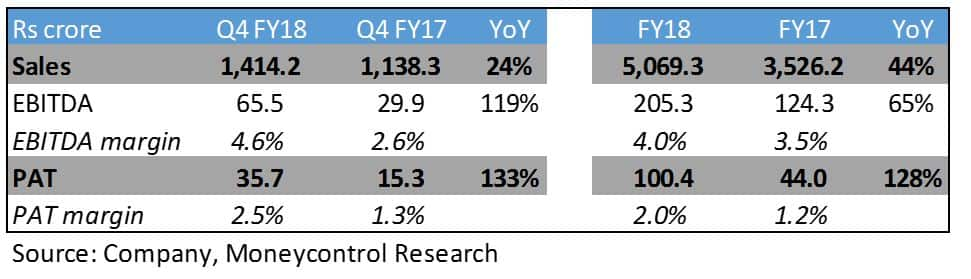

Sanwaria Consumer

Sanwaria Consumer, one of the largest integrated food processors in India, reported a 24 percent growth in topline and 133 percent growth in net profit in the March quarter.

Over the past 3-4 years, Sanwaria has changed focus from commodities processing to end-products. It has launched products under its own brand and has also entered the retail segment with the roll out of Sanwaria Consumer Shoppy (Sanwaria Kirana) outlets in Madhya Pradesh. It has also signed a deal with Patanjali to supply soya chunks to it.

High debt remains a concern, though the promoters recently infused Rs 100 crore (at Rs 35 per share) through a preferential allotment to repay a part of the loan. The company plans to raise another Rs 400 crores towards working capital, capacity expansion and acquisitions.

The realisations of rice and soyabean have improved considerably and this bodes well for a company like Sanwaria which derives 75 percent of its revenue from these two products. The company is gradually transforming itself into a branded FMCG company which should improve margins and thereby, earnings.

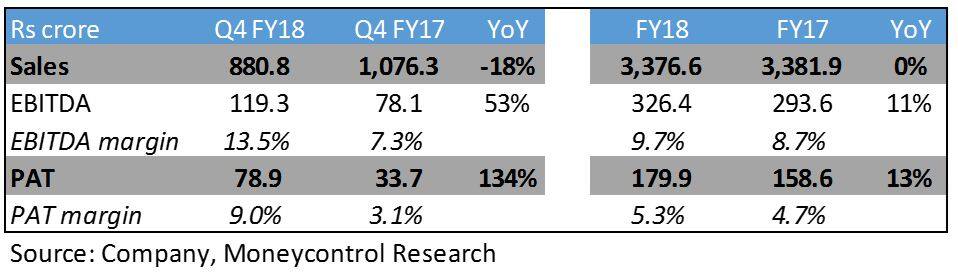

Gujarat Ambuja Exports

Gujarat Ambuja Exports (GAEL) is one of India’s leading manufacturers of agro-processed products and cotton yarn. GAEL’s revenue for the March quarter declined by 18 percent to 881 crores, but net income more than doubled to 79 crores. The topline was subdued as the company has shifted focus to manufacturing from trading of agro processing commodities. The margins improved on the back of higher contribution from manufacturing capacity.

GAEL has recently started operations at its 1000 metric tonnes per day maize processing plant at Chalisgaon (Maharashtra). With this, GAEL is now the largest maize processor in India with total capacity of 3,000 mtpd and a market share of 21-22%.

The company is expected to benefit from the drought in Argentina, the third largest soybean producer in the world. Soybean production in Argentina has fallen 30 percent this year. Lower production in Argentina has resulted in GAEL gaining competitive advantage in processed exports. Besides, GAEL will also benefit from improvement in crushing margins and soybean realisations as soya prices have increased 20-25 percent in the last 6 months.

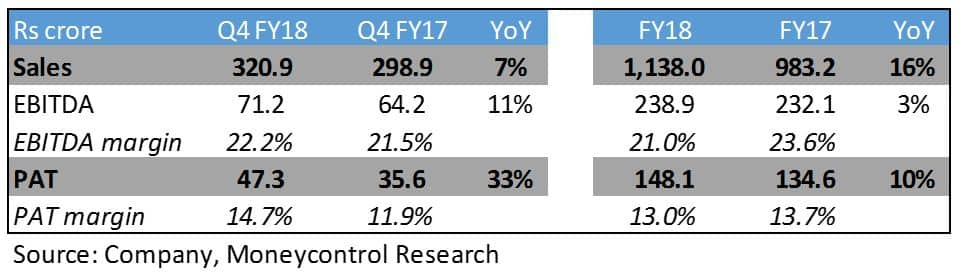

CCL Products

CCL Products (CCL) is India’s largest manufacturer and exporter of instant coffee. The company has an installed capacity of 30,000 MTs of instant coffee across India, Vietnam and Switzerland. CCL exports coffee and related products to more than 60 countries around the globe.

The company’s consolidated revenues for the quarter rose 7 percent to Rs 321 crores and net profit PAT rose 33 percent to Rs 47 crores. Growth was driven mainly by the strong performance from Vietnam operations. As the India capacity is working at nearly full utilisation, CCL is looking to grow its customer base in Vietnam after the commissioning of agglomeration capacity in the region. Vietnam’s capacity of 10,000 MT is now running at 70 percent utilisation and provides additional scope for revenue and profitability growth. Back home, CCL’s new 5,000 MT freeze-dried coffee plant is being set-up at Chittoor and is expected commence operations by H2 FY18.

The prices of green coffee have started decreasing and this might result in growth moderation as the customers have started to delay purchases in a low price environment. Accordingly, the management has given a conservative revenue growth guidance of 10-20% in the current financial year, excluding the new plant capacity. The new plant is a high margin business and will further aid the profitability of CCL as volumes pick up.

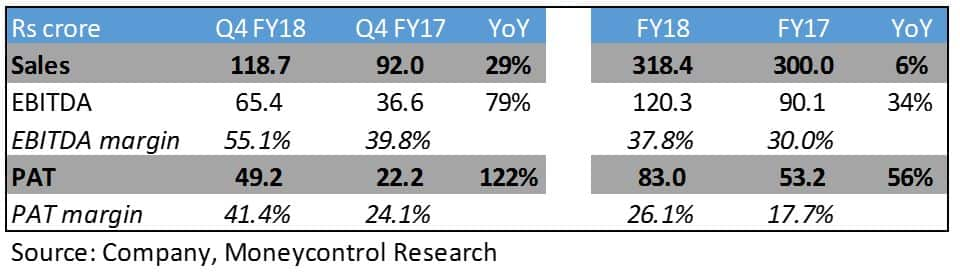

Quick Heal Technologies

Quick Heal Technologies provides security software products and solutions in India, Japan, Kenya, the United Arab Emirates, and other regions. The company has a strong footprint in both the retail and enterprise segments. It has 30,000+ Enterprise and 8.4 million actives licence users and has a 34 percent market share in the retail segment.

Quick Heal’s quarterly revenues rose 29 percent year-on-year to Rs 118.7 crore in Q4 FY18, and net profit jumped 122% to Rs 49.2 crore. The March quarter is generally the strongest in terms of revenues due to renewal of product and service licence agreements at the start of the year. It contributes around 35-40 percent of its yearly sales.

The company operates in the retail and enterprise segments. It derives around 80 percent of revenues from the enterprise segment and the balance from retail. Renewal rate for retail segment stands at 35 percent while that of the enterprise segment is much higher at 75 percent. The management wants to increase the renewal rates in both the segments to aid long term revenue visibility.

The market opportunity for internet security services is huge as there are more than 50 million mobile and laptops on the retail side. Small and mid-sized enterprises which form a major part of the enterprise segment has a market size of 40 million and these enterprises are gradually integrating technology with their businesses. In general, the cyber security market is vastly underpenetrated and proves ample opportunities for growth amid concerns of data privacy.

Quick Heal plans to replicate the success in the consumer security segment to expand its coverage on the enterprise segment. The business is highly scalable and enjoys high operating leverage and looks well positioned to grow in an increasingly digital world economy.

Recommendation

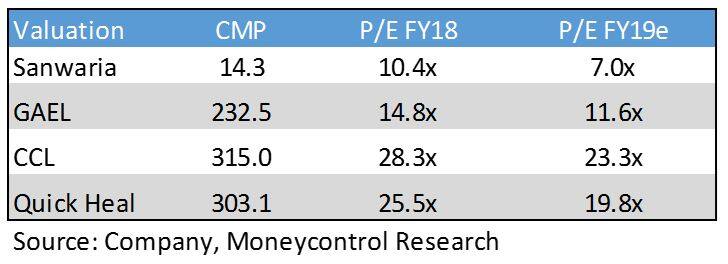

Amongst the four stocks, Sanwaria and GAEL trading at 7.0x and 11.6x one year forward price-earnings multiple offer attractive risk-reward ratio at current valuations. CCL and Quick Heal are relatively expensive at current prices and can be accumulated on minor corrections.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.