Madhuchanda Dey Moneycontrol Research

RPG Life Sciences, the smallest group entity in the RPG stable, is primarily a domestic, market focused, small pharmaceutical company that is trying to make its existence relevant by diversifying. While the management has lofty ambitions of achieving a turnover of Rs 1,000 crore in the next 4-5 years, the journey may not be easy and there could be roadblocks and volatility in earnings. While keeping the stock under radar makes sense, the management’s strategic intent will have to start reflecting in its performance before one can look at it from an investment perspective.

Management rejig: A welcome change

The small, sleepy company has been making decent progress under its new management (from 2015). Sales grew by 7 percent CAGR (compounded annual growth rate) between FY12 to FY15 and 14 percent in the past three years. The market has handsomely rewarded this performance, with the stock rallying close to 115 percent in the past three years.

The business

RPG Life continues to remain a predominantly local focused player with 63 percent revenue accruing from domestic formulations. Active pharmaceutical ingredients (API) contributes close to 15 percent of revenue. The international business contributes the rest. Of this, 14.8 percent accrues from regulated international markets and 7 percent from rest of the world (RoW) markets.

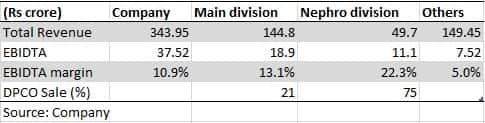

In domestic formulations, the Main Division develops, manufactures and markets branded formulations across a wide therapeutic spectrum that includes vitamins, gastrointestinal, pain and inflammation management, relief from respiratory ailments and cardio-diabetes management.

The company’s major brands include Min Min (vitamins and iron supplements), Tricaine (antacid), Lomotil (anti-diarrhoea) and Serenase (central nervous system).

It also runs a profitable Nephro division. Nephrocare has been a pioneer in launching Azoran (Azathioprine) which was developed and manufactured in India.

While the domestic formulation business has been a driver of growth and profitability, with established brands still growing, the proportion of drugs under price control (DPCO) is also on the rise. At FY18-end, 34 percent of domestic formulation sales was under price control. The management plans to counter this with additional new product launches.

The new domestic divisions so far have been a drag on profitability. Neolife, its oncology division, clocked sales of Rs 17 crore in FY18 but experienced price deterioration on high competition, large institutional sales and commodity products. The urology division (Urolife) experienced lower sales. These businesses are still in investment mode and product launches in established as well as new businesses are critical to its profitable, long-term growth strategy.

International business

Its global generics division commercialises finished dosage forms in highly regulated markets such as North America, European Union and Australia. Azathioprine is a flagship product of RPG Life Sciences, which has a dominant market share worldwide in immunosuppressant therapy. RoW business caters to markets other than the US and Europe. Africa, Southeast Asia and Latin America are the major geographies that the company’s RoW business operates in. Investment in new product pipeline, with a focus on R&D is the key strategic intent in the international business.

Plans to enter the US market is still some time away. The management expects a US Food & Drug Administration inspection in September-October next year and a launch by FY20-end. Aminocaproic Acid, Azathioprine and Mycophenolate Mofetil are products under development for the US market.

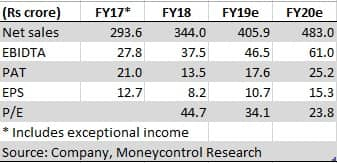

The management’s strategic intent is well understood but execution remains to be monitored. While its medium term goal of Rs 1,000 crore turnover by FY22 looks like a tall task now. The management seems to be open to inorganic opportunities as well. Seen in this context, the stock needs to be on the radar of serious investors. At 24 times FY19e earnings, the current valuation prices in a gradual improvement in the near term.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.