When money is tight during an emergency, many people turn to their investments for quick relief. It feels logical - after all, that money is already yours. But using long-term investments to handle short-term problems can quietly hurt your wealth in ways that aren’t obvious immediately.

Emergencies don’t come with warnings. A medical expense, a sudden repair, or a break in income can force quick decisions. And that’s often when long-term plans take a hit.

Why Timing Becomes the Biggest Problem

Investments work best when you can wait. Emergencies don’t give you that luxury. When you need cash urgently, you’re forced to sell regardless of market conditions. Even stable equity investments go through rough phases.

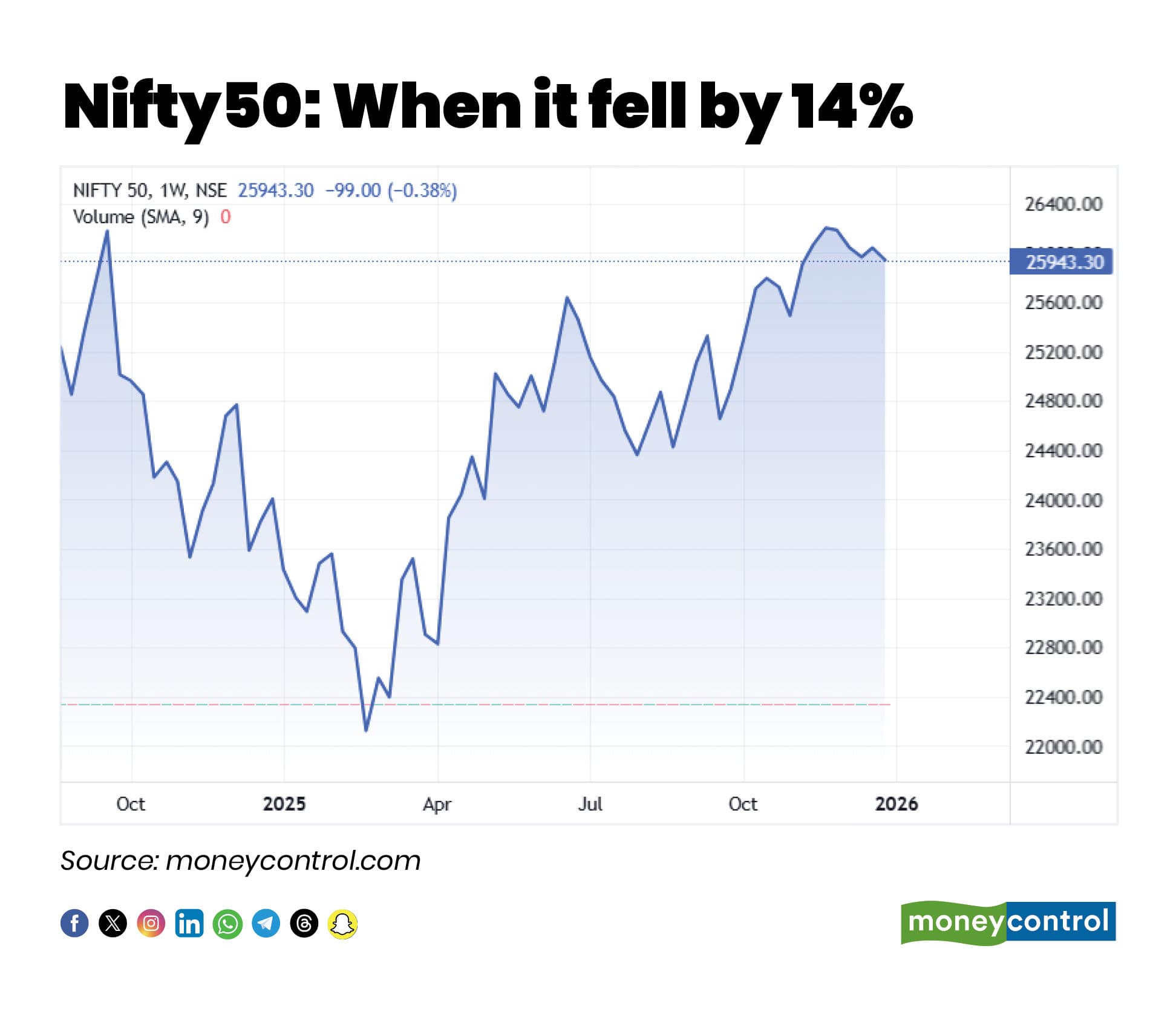

Between October 2024 and February 2025, markets fell by around 14 percent before recovering later.

Anyone who exited during that period had no way to benefit from the rebound.

The issue isn’t that markets fall - it’s that emergencies force you to act when patience would have helped.

How withdrawals break the power of compounding

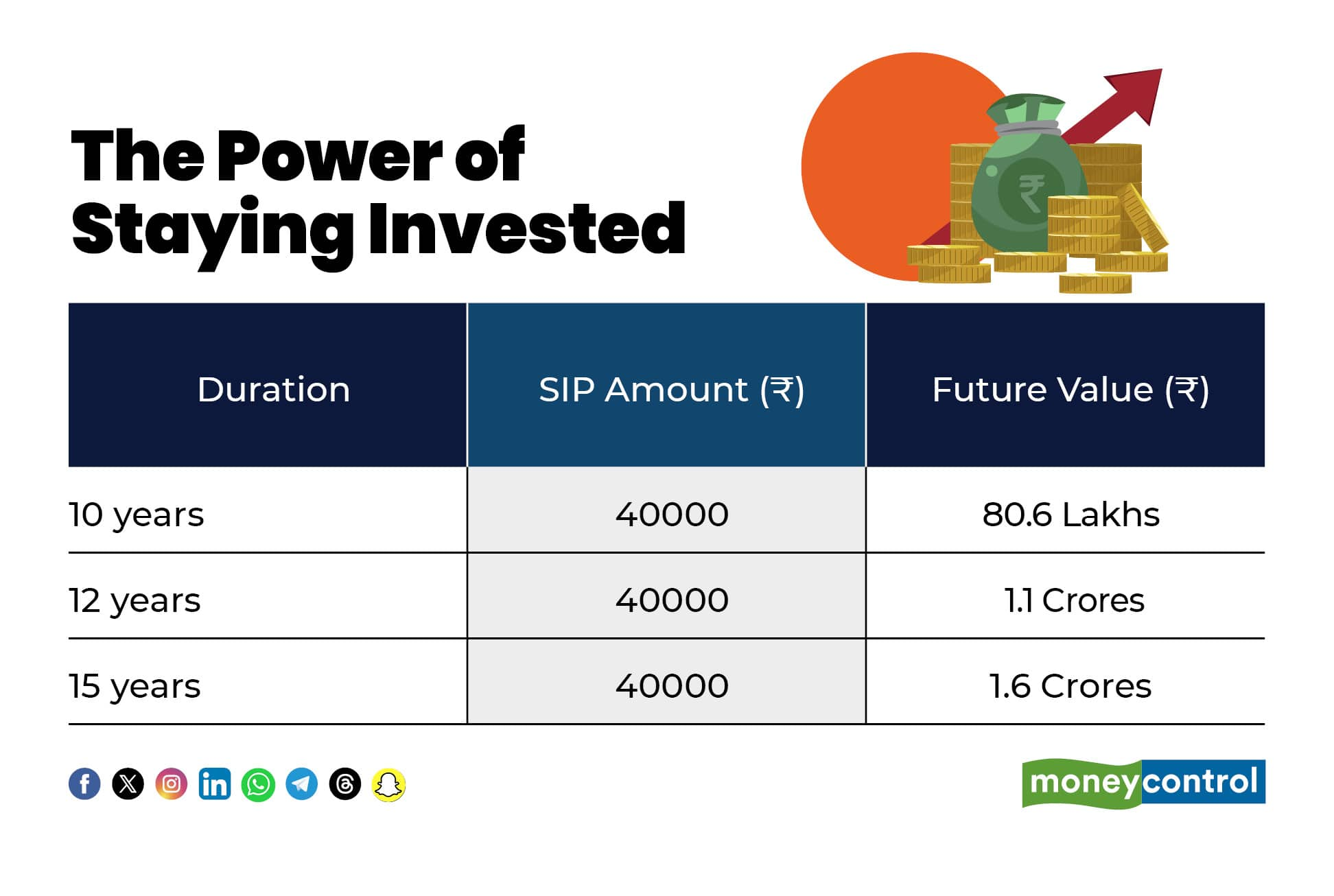

Compounding needs time and consistency. When you pull money out midway, that process gets interrupted.

For instance, investing Rs 40,000 every month at a 10 percent annual return can grow to about Rs 80 lakh in 10 years. Stay invested for five more years, and the amount nearly doubles to around Rs 1.6 crore.

When investments are broken to meet emergencies, this long-term growth slows down - or in some cases, stops altogether.

What looks like a small withdrawal today can mean a much smaller corpus tomorrow.

In an emergency, the goal is to fix the problem quickly - not to optimise returns. That’s when investors end up selling at the wrong time, exiting long-term plans, or deciding to ‘pause’ investing altogether. Once that discipline breaks, restarting with the same confidence becomes difficult.

Why an emergency fund makes all the difference

This is where an emergency fund plays a crucial role.

An emergency fund is money set aside only for unexpected situations, so that long-term investments remain untouched. The common rule of thumb is to keep the equivalent of six months’ salary or expenses as an emergency buffer.

For someone spending around Rs 1 lakh a month, that means setting aside roughly Rs 6-9 lakh purely for emergencies.

Where should this emergency money be kept?

The goal of an emergency fund isn’t high returns. It’s quick access and safety. A simple way to manage it is to spread it across:

This combination ensures money is available when needed, without forcing you to disturb long-term investments.

The bottom line

Using investments to manage emergencies may seem convenient, but it often leads to poor timing, broken compounding, and decisions made under stress. A separate emergency fund helps protect long-term goals from short-term shocks.

Emergencies are part of life. Your investments don’t have to suffer because of them.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.