If you do not mind taking credit risks in return for a slight kick in returns, which debt fund should you go to? You go to credit risk funds. These are schemes that invest at least 65% of their corpus in securities that are rated AA and below.

Things got easier last year after the capital market regulator, Securities and Exchange Board of India (SEBI) categorized debt mutual fund (MF) schemes into 16 categories (36 categories across all MF schemes), and carved out credit risk funds as those that could invest in low-rated scrips.

But what happens if your short-term fund or medium term fund or even a liquid fund takes as much credit risk? To be fair, there is nothing legally wrong here. When SEBI categorised funds last year, it laid down boundaries depending on what a fund sets out to do. If it intends to take credit risk, then SEBI gave such funds credit (rating) boundaries at the time of making their investments.

But if the fund set out to benefits from interest rate movements, it drew boundaries in terms of the duration (or, in loose terms, the tenure) of the underlying instruments that they can invest in. But what happens if, in the chase for scrips that fit into the tenure criteria, your fund ends up taking credit risk?

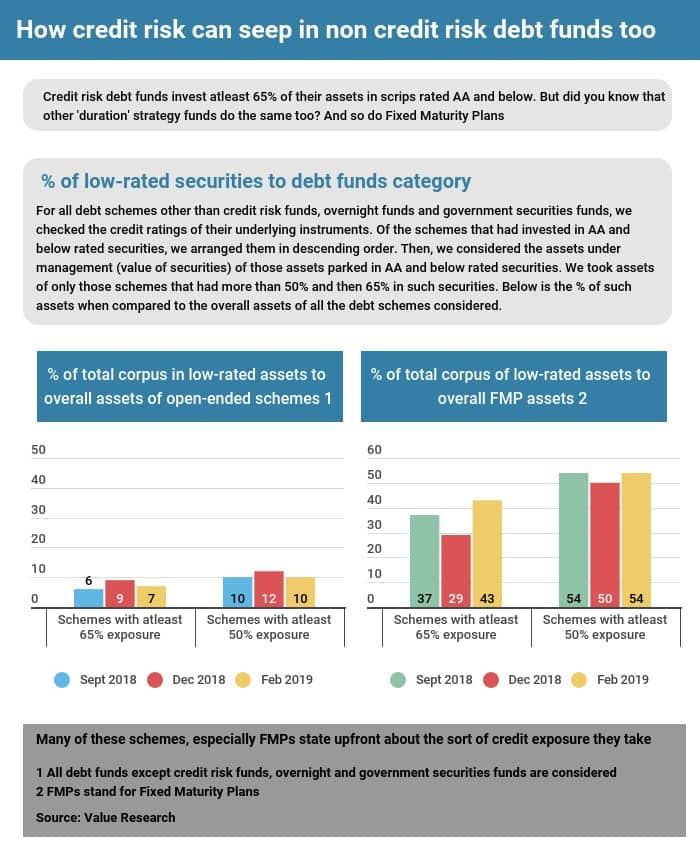

As per a Moneycontrol study, the total assets that open-ended debt funds have invested in AA and lower-rated securities constitute 10% of the overall assets in such funds. This is just for schemes that have invested 50% and more in such securities. Of the schemes that have invested 65% and more in such securities, the total assets that open-ended debt funds have invested in AA and lower-rated securities constitute 7% of the overall assets in such funds. (see table)

Value Research data also tells us that as per the February 2019-end portfolios, some schemes from Franklin Templeton Asset Management (India), Reliance Nippon Life Asset Management, Edelweiss Asset Management and so on have more than 65% of their assets invested in such securities.

This is not to say that these schemes are bad. But did you know that duration-strategy funds or non-credit risk funds also carry credit risk?

Experts say that when fund houses invest in securities, they just do not buy them in one fund; they tend to allocate them across their funds.

Deepak Chhabria, chief executive officer and director, Axiom Financial Services, a Bengaluru-based distributor of financial products explains that a credit risk fund may buy a security that has a low credit rating but fits in a long-term fund as they don’t mind buying and holding it till maturity. But a year or two later, if the manager finds a better security, he could transfer the same paper to his short-term fund as by that time, this security would be closer to its maturity and fits in the duration boundary of the second scheme.

“At this point, the security’s credit risk doesn’t matter so much; he would just focus on its duration and whether or not it matches that of the second fund”, says Chhabria.

The other reason why many debt funds invest in low-rated scrips takes us to prior SEBI’s categorisation rules that came in 2018.

“Before SEBI’s categorisation, some fund houses used to run two schemes with a credit strategy. One scheme bought higher amounts of low-rated securities; the other bought lower amounts of low-rated securities. When SEBI categorised funds and limited one scheme per category, many of these fund houses converted their less aggressive funds to medium duration funds,” said a debt fund manager requesting anonymity.

Of the 42 debt schemes that invest at least 25% in low-rated scrips, 11 are medium-duration bond funds.

Are all low-rated scrips bad?“No”, says Lakshmi Iyer, Chief Investment Officer of Debt and Head of Products, Kotak Mahindra AMC, emphatically over the phone. Iyer’s scheme, Kotak Low Duration invests 68.26% in AA and below rated securities. But Iyer says that credit ratings alone don’t tell us the entire picture.

“Not everything AA-rated is credit risk and not everything that is rated AAA is highest safety. We do also avoid certain business houses or scrips that are rated AAA-rated,” she added.

Iyer says that it is natural for debt funds to offer schemes at varying risk levels, each fund different from the other, even though overall all such funds may belong to the same category.

“There could be one debt fund that invests 50% in AAA-rated and 50% in AA-rated, another scheme would invest in the ratio of 30%-70% and a third that invests 70%-30%. Also, we check a security’s long-term as well as short-term rating to decide whether to invest or avoid that company’s security,” added Iyer.

Iyer further said a non-AAA instrument when issued for a tenure of greater than one year, as the residual maturity gets to below one year, tends to get mapped to short-term rating (in terms of risk) which could be A1+, for most issuances rated up to a rating of ‘A’ or ‘A+’. Hence, pure optics of rating may not reveal the complete picture.

Suyash Choudhary, Head – Fixed Income at IDFC Asset Management Company has a different point of view.

“In some sense credit has been used quite heavily as a strategy over the past few years. This is clearly reflected in the growth of both dedicated credit risk funds as well as those that partly run credit-oriented strategies. So far the market for lower rated credit is quite illiquid, and especially so for A and below rated securities.”

Fund houses, on their part, stress on the need to communicate the products more clearly and loudly.

Shriram Ramanathan, Head – Fixed income at L&T Investment Management knows the importance of communicating what the scheme will do, upfront and at all times.

According to Value Research, one of his schemes, L&T Low Duration Fund has invested 67% of its assets in AA and equivalent rated scrips. An exit load appropriate to the holding period that such schemes demand should also be in place, Ramanathan says, to make sure investors are willing to stick around to ride out the volatility, if any.

And staying consistent to the strategy is important here. Take the case of Franklin Templeton. Around the end of 2015, some of its schemes suffered loss on account of a credit rating downgrade in Jindal Steel and Power (JSPL) debt securities.

At the time, six of its schemes had 2-7% of their corpus in JSPL debt. The fund house sold off its JSPL securities in early 2016 and suffered a loss. But the fund house stuck to its strategy and although it tightened its credit appraisal process, it continues to invest in companies with weaker credit ratings.

Five of the top 10 funds in terms of the highest exposure to AA and below rated securities belong to Franklin Templeton; a strategy that the fund house has consistently and unflinchingly followed throughout across most of its debt funds, aside from its specific credit risk fund.

According to Value Research, Reliance Strategic Debt Fund, a medium duration fund, has invested 75% of its corpus in AA and below rated securities. A closer look at its portfolio shows that it does not go below AA- rated securities.

“This has been the case, consistently, since 2014 when this scheme was launched. There is a distinct credit risk positioning of this fund, while it remains a moderate duration strategy fund and typically invests in scrips that mature between one and four years”, says Amit Tripathi, chief investment officer – fixed income investments, Reliance Nippon Life Asset Management.

Should SEBI revisit its classification?Experts are divided over whether it’s time for SEBI to tighten its categorisation and specify the credit-rating limits for duration funds.

Choudhary says: “Duration boundaries have been defined relatively tightly whereas the judgment on quantum of credit risk to be taken has been largely left to the fund manager for most fixed income products. However, as the categorization settles down, there may well be a case for further nuanced definitions on rating based credit thresholds for all non-sovereign product categories”.

Iyer doesn’t agree and says that there are several investors with varying risk profiles who need different products. She gives an example of Google Maps, using which we aim to reach our destination. “But if there is traffic and we reach half hour late, we cannot blame Google Maps. That role (to select the right fund for our needs) has to be played by the financial advisor”, she says.

What should you do?Debt funds are essential for your portfolio because they provide a convenient way to invest in fixed income securities and help your portfolio in asset allocation. “But credit risks are a part of debt investments, except in government securities and perhaps also in overnight funds. That needs to be appreciated”, says Joydeep Sen, founder, wiseinvestor.in.

Debt funds are not as easy to understand as bank fixed deposits. The good side is they offer you a chance of better tax-efficient returns. Ask questions to your advisor about what the fund does, where it invests, how much credit risk it takes. If you wish to completely avoid credit risk, opt for funds that do so as well. But if you invest in funds with a bit of credit risk, then make sure that you understand the risks that come along with them.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.