If your salary comes in and disappears into EMIs and card bills within days, you’re not alone. For many households, high-interest debt, especially credit cards, has quietly become the biggest reason they feel stuck financially.

The good news is that getting out of a debt trap doesn’t require extreme measures. It requires a clear plan, and the discipline to follow it. One such plan, widely recommended by financial planners, is the Avalanche Method.

Step One: Stop Digging the Hole Deeper

Before any repayment strategy can work, one rule is non-negotiable: pause new credit card spending until existing dues are cleared.

Credit cards may feel convenient, but they are also the most expensive form of borrowing in the market. Interest rates can climb to 45-50 percent a year, and hidden charges can quietly inflate outstanding balances. If controlling spending feels difficult, temporarily deactivating the card can prevent the problem from worsening.

What Is the Avalanche Method?

If you’re already juggling multiple loans, trying to ‘manage everything at once’ often leads nowhere. The Avalanche Method brings order to that chaos by answering one simple question: which loan is costing you the most right now?

So, instead of spreading your money thin across all debts, this method asks you to:

The focus here isn’t emotional relief, it’s minimising interest leakage. Let’s understand with a realistic example how the strategy works.

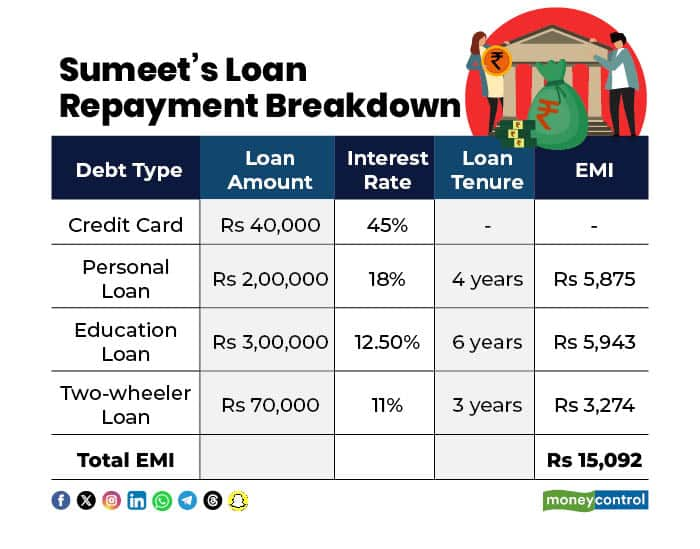

Consider Sumeet, who earns a monthly in-hand salary of Rs 45,000 and has four ongoing debts - 3 loans and 1 outstanding credit card bill:

Sumeet’s total EMIs (excluding the credit card) already come to Rs 15,092 per month.

Under the Avalanche Method, the credit card balance becomes the top priority, not because it’s the smallest amount, but because it carries the highest interest burden.

Let’s make this strategy work in practice now. To prevent the credit card debt from ballooning further, Sumeet converts his Rs 40,000 outstanding balance into a six-month EMI plan at 18 percent interest. This brings his monthly payment to around Rs 7,021.

During these six months:

Once the card dues are cleared, that Rs 7,000-plus monthly outflow doesn’t disappear. Instead, Sumeet redirects it toward aggressively paying down his personal loan, followed by the education loan, and finally the bike loan.

Over time, each closed loan frees up more cash, accelerating the repayment of the next one.

Why the Avalanche Method Works

The Avalanche Method works because it attacks the real enemy in a debt trap: high interest. By prioritising the costliest loans first, borrowers reduce the amount of money lost to interest every month.

In Sumeet’s case, moving credit card debt from a 45 percent rate to an 18 percent EMI plan alone can save several tens of thousands of rupees in interest over time, compared to letting the balance roll over.

Ravindra Rai, MD & CEO of BOBCARD explains, “Having multiple credit cards can be beneficial when each card serves a clear purpose and spending is planned consciously. However, challenges typically arise from limited awareness of repayment timelines, billing cycles, and total credit exposure.” He adds, “Used well, credit cards can offer flexibility without increasing financial stress, help cardholders manage cash flows better, optimise benefits, and gradually build a healthy credit profile.”

That said, the method isn’t magic. It works best when income is stable and spending is kept in check. Missing EMIs or adding fresh debt can undo the benefits quickly. But for borrowers who can maintain discipline, the Avalanche Method offers something many debt-ridden households lack, a clear exit path and measurable progress.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.