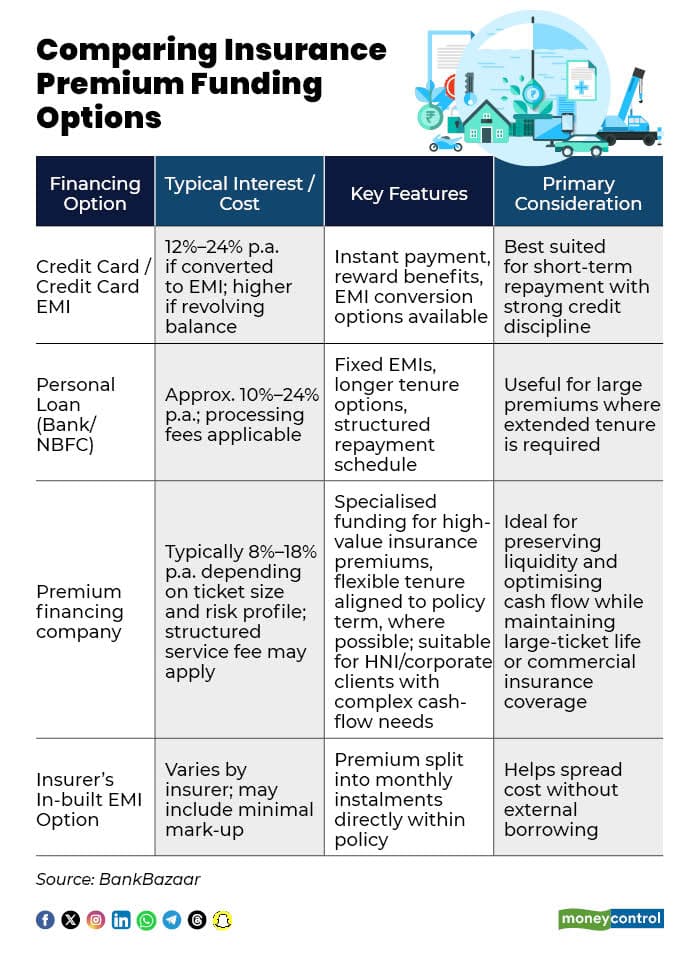

When your insurance premium is due, especially a large annual payment, you don’t necessarily have to dip into your savings. Policyholders today have multiple financing options to spread the cost. You can opt for insurance premium finance companies that specialise in premium funding, use a credit card (and convert the payment into EMIs), or take a personal loan from a bank or NBFC or insurer inbuilt emi options. Each option comes with different interest rates, repayment tenures, processing fees, and an impact on your credit profile.

While insurance finance companies are tailored for policy payments, credit cards offer short-term flexibility but can be expensive if not converted to EMIs, and personal loans may suit larger premiums with structured repayment. Understanding the cost, tenure, and flexibility of each route can help you choose the most efficient way to finance your policy without straining your cash flow.

Paying a premium with premium financing?

Premium financing allows you to pay your insurance premium in instalments, monthly or quarterly, instead of paying the entire amount upfront. Some platforms even provide no-cost EMI options, enabling you to split the payment without paying additional interest. The process is largely digital, requiring basic KYC documents, a copy of the policy, and bank details, with approvals often completed within a few days. Key players in this space include BimaPay, Capital Float, and Bajaj Finserv, along with select banks and emerging insurtech-led lending platforms.

For those who want comprehensive insurance coverage but need to manage cash flow carefully, premium financing can make protection more affordable and accessible.

“Customers generally have access to 6 to 12 EMI options, with customised tenures available for corporate or group policies depending on underwriting structures. This is not just a loan; it is a purpose-driven financial tool designed to prevent policy lapses and ensure that protection remains a constant rather than a discretionary expense,” said Hanut Mehta, Co-Founder & CEO at BimaPay Finsure.

How EMI options work for premium financing?

If your premium is due on March 1, you can apply through an NBFC, fintech platform, or select banks offering this facility. Once approved, the lender directly pays the insurer, and you repay the amount in monthly instalments.

Interest rates, tenure and charges

Interest rates in the market typically range between 12 percent and 24 percent annually, depending on your profile and tenure. EMI options usually span 3 to 12 months, and some lenders may charge a small processing fee. Approval is generally quick, within 24 to 72 hours, with funds remitted directly to the insurer.

Documents and prepayment terms

Documents required typically include PAN, Aadhaar, 3 to 6 months’ bank statements, a copy of the policy, and income proof (for higher premium amounts). Prepayment terms vary: some lenders allow foreclosure after a lock-in period without charges, while others may levy a 2 percent to 5 percent fee. Experts suggest that you should always review the fine print before opting for financing.

Paying a premium with a credit card?

Paying insurance premiums with a credit card allows you to make the payment even if you do not have the full amount available in your bank account at that moment, helping you avoid policy lapses and meet deadlines comfortably. Timely repayment of your credit card dues can also strengthen your credit score, reflecting responsible financial behaviour to lenders.

Additionally, many credit cards provide reward points, cashback, or other benefits on transactions, including insurance payments, adding extra value. With auto-debit or standing instruction options, you can ensure your premium is paid on time, making your overall financial management more streamlined and disciplined.

When it comes to paying insurance premiums through a credit card, “the decision should be driven by cash-flow management rather than convenience alone. Converting a large premium into EMIs can help households preserve liquidity, especially during periods of high annual outflows. However, policyholders must carefully evaluate the effective interest rate, processing charges, and the repayment tenure before opting for this route,” said Mahesh Shukla, Founder and CEO at PayMe.

Paying a premium with a personal loan?

Instead of paying the insurance company directly, you can take out a fixed-rate personal loan from a bank or NBFC. You use those funds to pay the insurer in full and then repay the lender over a set term.

A personal loan offers structured repayment through fixed EMIs, but the overall interest outgo is usually higher because the tenure is longer, and processing charges may apply. “If the insurer provides an in-built EMI facility, it can be a practical way to spread the premium without taking on separate debt. However, always compare the total payable amount against the annual premium to assess the true cost. Ultimately, the right choice depends on repayment discipline, tenure, and the total cost over the full period, not just the size of the monthly instalment,” said Adhil Shetty, CEO, BankBazaar.

Apart from external financing routes, you also have the option of choosing your insurer’s in-built EMI facility. Under this option, the premium is split into monthly instalments directly within the policy itself. The cost varies by insurer and may include a minimal markup. It helps spread the expense without taking external borrowing, making it a convenient alternative for managing cash flow.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.