The Reserve Bank of India’s Monetary Policy Committee (MPC) has decided to keep the repo rate unchanged at 5.25 percent, opting for a pause after cumulative easing over the past year. The decision was in line with expectations, as inflation remains within the RBI’s comfort band and growth indicators stay resilient.

For home loan borrowers, the status quo means no immediate change in EMIs or lending rates, especially for loans linked to external benchmarks such as the repo rate. Banks are unlikely to revise home loan interest rates in the near term unless there is a change in policy stance or liquidity conditions.

While today’s decision does not offer fresh relief, borrowers have already benefited significantly from the 125 basis points of cumulative repo rate cuts delivered earlier. These cuts have translated into lower EMIs and substantial interest savings over the loan tenure for those whose loans have fully transmitted the rate reductions.

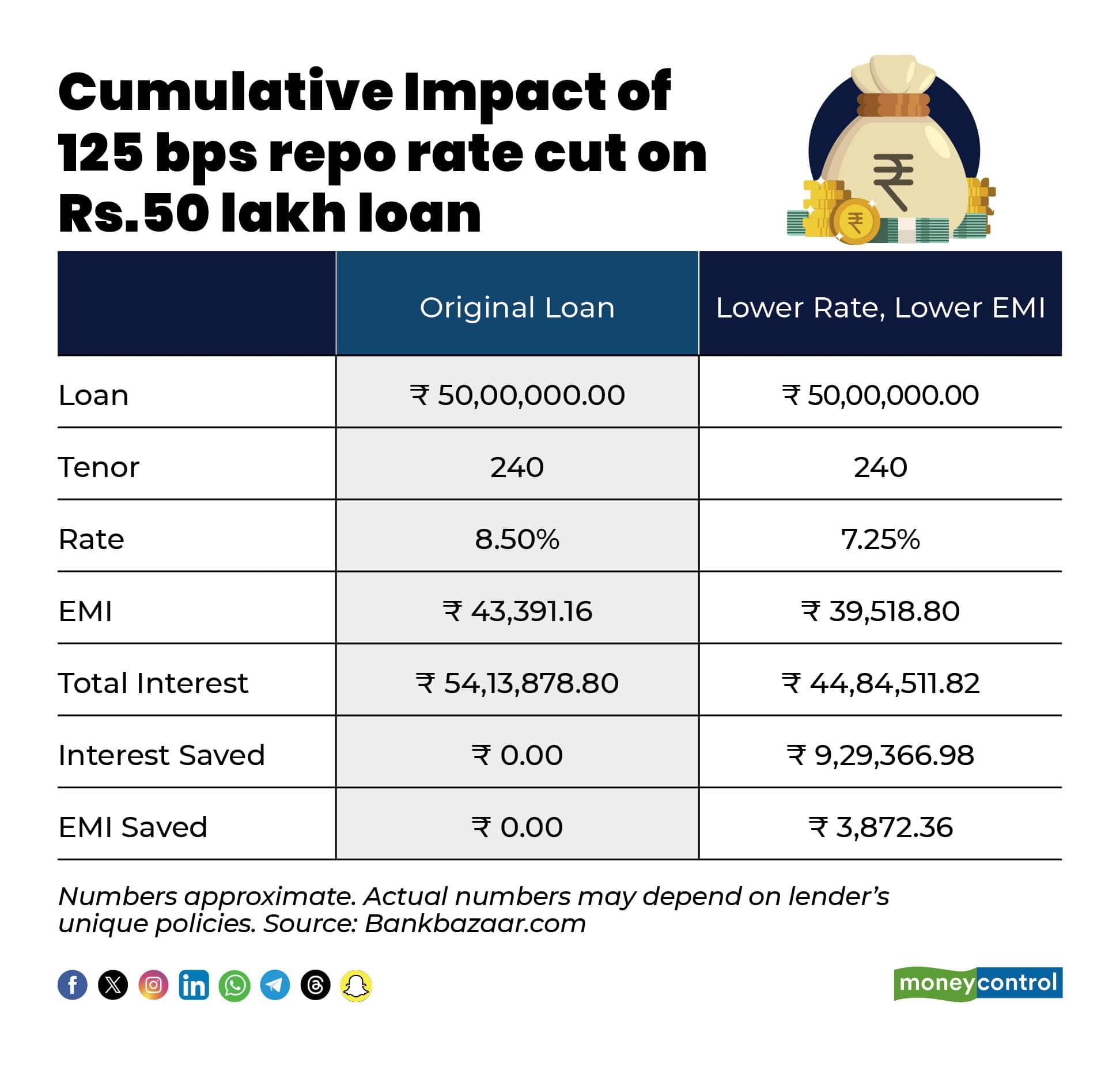

How much borrowers have already gained from past rate cuts

The data shows that borrowers with a Rs 50 lakh home loan over 20 years could save over Rs 9.29 lakh in total interest due to the cumulative reduction in rates, with monthly EMIs falling by nearly Rs 3,900.

What unchanged rates mean now

With the RBI pressing pause, floating-rate home loan EMIs are expected to remain stable in the coming months. Fixed-rate borrowers will see no direct impact unless they choose to refinance or switch lenders. Experts say the central bank’s focus is now on ensuring full transmission of earlier cuts rather than rushing into further easing.

"With the RBI maintaining a status quo on the repo rate at 5.25 percent, policy continuity has brought much-needed stability for home loan borrowers. An unchanged rate has ensured that EMIs on floating-rate loans remain steady, offering predictability at a time when housing demand continues to stay resilient across major urban markets," said Manju Yagnik, Vice Chairperson of Nahar Group and Senior Vice President of NAREDCO Maharashtra.

"Borrowers can continue to optimise savings by retaining higher EMIs to compress loan tenures and reduce total interest costs. Balance transfer opportunities and loan restructuring options also remain relevant for those seeking incremental efficiencies. Stable rates, combined with sustained housing demand and improved project execution, create a conducive environment for long-term home buyers, particularly end users focused on financial predictability rather than short-term rate movements.” said Adhil Shetty, CEO BankBazaar.com.

Borrowers planning to take fresh home loans may not see further rate reductions immediately, but the current environment still offers relatively attractive borrowing costs compared to previous years.

Going ahead, any further movement in home loan rates will depend on how inflation evolves, global interest rate trends, and the RBI’s assessment of domestic growth. For now, borrowers can expect stability rather than fresh relief, while continuing to enjoy the benefits of the earlier rate cuts already baked into their loans.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.