Are Indians financially prepared for their retired life? They clearly don’t seem to be. A PGIM Retirement Readiness Survey 2020 found that most Indians do not have a retirement plan ready. In February 2020, PGIM conducted a survey to assess whether Indians are saving up for their silver years.

It commissioned market research firm Neilson, which surveyed more than 3,000 people across eight metros and seven non-metros to gauge their attitude towards retirement planning.

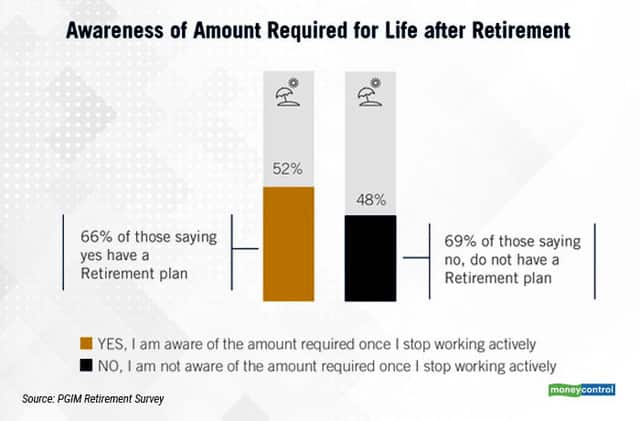

The PGIM Retirement Readiness Survey pointed out that only 52 percent of the respondents knew how much they needed for retirement. The remaining 48 percent did not have any awareness of their retirement kitty. Quite obviously, 69 percent in this set did not have a retirement plan in place.

“A large section of people can tell you vaguely that they would receive their provident fund (PF) and gratuity upon their retirement. What they don’t realise is that the amount only takes care of 30 percent of their total post-retirement corpus requirements,” says Preeti Chandrashekhar, India Business Leader – Health and Wealth, Mercer.

Also read: Go beyond just financial planning for a happy retirement

Besides, she adds, gratuity only grows meaningfully if you continue with the same organisation.

According to estimates made by Tru-Worth Finsultants, you must invest Rs 30,000 to Rs 1 lakh every month, depending on your age, to accumulate a tidy retirement corpus.

Assume you are 30 years old, and plan to retire at 60 and hope to live till 85. In other words, you have 30 more years to earn and 25 years of post-retirement life. Your monthly expenses are, say, Rs 50,000. Let us assume that your expenses increase by 6 percent annually and your investments grow at 10 percent. At this rate, you need an investment corpus of Rs 5.58 crore. “Even if you assume that your PF and gratuity total up to Rs 30 lakh at retirement, you still need to accumulate Rs 5.28 crore (Rs 5.58 crore less Rs 30 lakh) by the time you retire,” says Tivesh Shah, Founder of Tru-Worth Finsultants.

How much do you need to save every month to get there? If you are 30 years old, you need to save close to Rs 16,000 every month, if you increase your annual systematic investment plan amount by 5 percent. But if you are 45, you need to save at least Rs 38,300 every month.

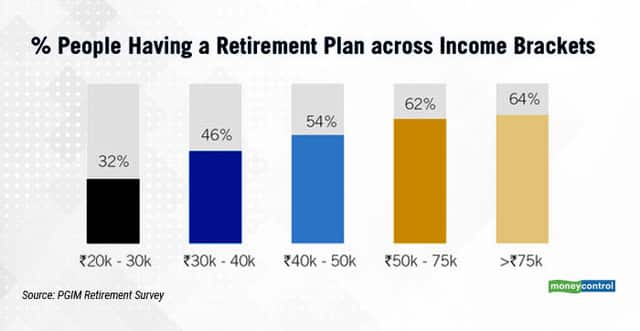

Surplus matters, not ageThe survey found that those with higher incomes got around to making a retirement plan. Those who earned a lower income didn’t put in much effort in the direction. Just 32 percent of those who earned between Rs 20,000-30,000 a month cared to save for their silver years. On the other hand, 64 percent of those who earned more than Rs 75,000 a month made definitive plans.

Suresh Sadagopan, Founder of Ladder7 Financial Advisories says, “If you have a certain level of income and certain financial goals, then those goals would definitely get priority,” says Sadagopan. He adds that in the face of financial goals such as buying a house, saving for children’s’ education get precedence. “Obviously, retirement planning doesn’t get priority,” he says.

Between 2017 and 2019, people focussed more on planning for a better standard of living, fulfilling of dreams and a enjoying a comfortable life, and less one security and safety. This is increasingly is becoming a trend, says Ajit Menon, chief executive office, PGIM India Mutual Fund. “Many of us like to plan for ‘happy’ events of our life. Safety and security are less important. Retirement is not looked as a very positive thing by younger generations these days,” says Menon.

What do people save for?The survey gives insights on how people’s financial goals change with age and income. Those between 26 and 40 are more focused on maximising their wealth. Around 53 percent of the respondents in this age group said they want to generate higher returns and 51 percent said they want to become financially secure.

Priorities changed as income levels grew, the survey observed. Those with lesser income focus on increasing their wealth, saving taxes and generating more returns from their investments. But as people’s income rise, their ambitions become wider. Those between 41 and 60 had a wider horizon of objectives – starting a new business and so on.

When asked where the respondents invest to plan for their retirement, most mentioned a host of instruments: life insurance, fixed deposits, mutual funds and so on.

Here’s the interesting part: Those who do have a retirement plan invest comparatively lower amounts in life insurance and fixed deposits (FDs). The investment pattern was just the opposite for those who didn’t have a retirement plan. “Most people who have a bulk of their savings in life insurance invested there to save taxes. Retirement planning is, typically, a secondary goal here. Those who have a proper retirement plan are more aware financially and about better options to save for retirement,” says Yogin Sabnis, chief executive officer, VSK Financial Consultancy Services.

Mumbai-based registered investment advisor and financial planner Gaurav Mashruwala says that the okder generation invested mainly in insurance policies and bank FDs. “Life insurance companies, for long, had products dedicated towards retirement. And many individuals went for such policies,” he says.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.