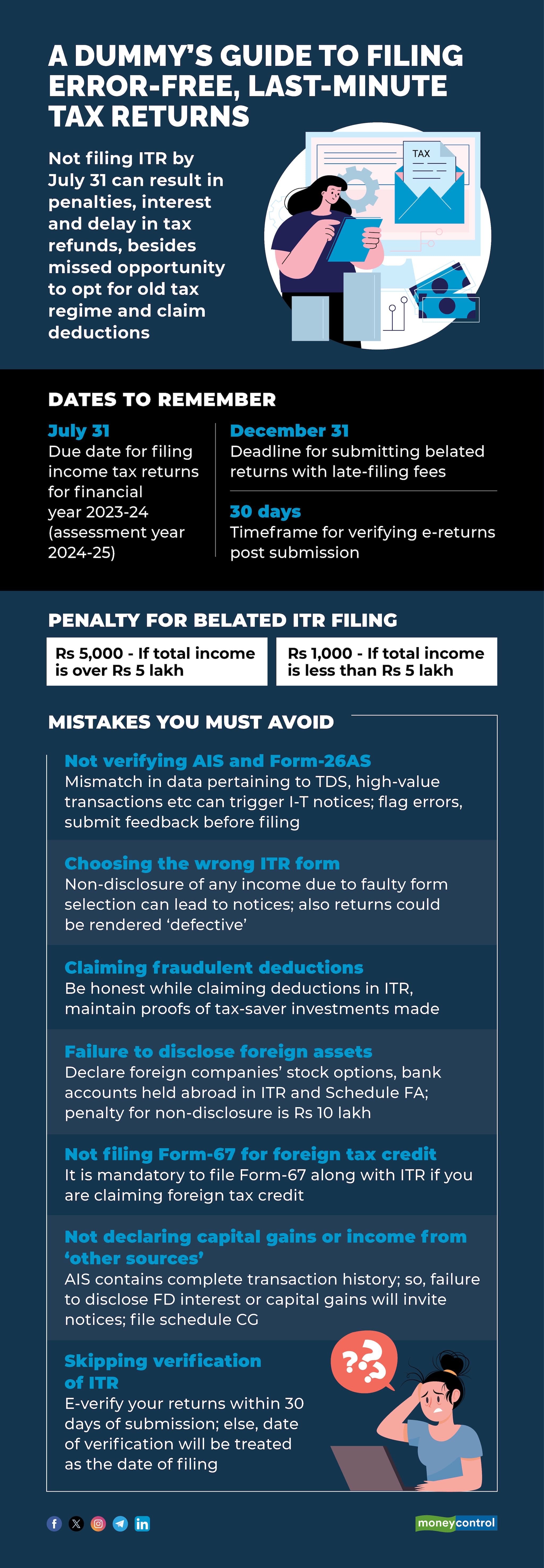

July 31 is here.

If you have not filed your income tax returns already, there is no time to lose.

The consequences of not adhering to the deadline can be severe. Besides late-filing fees, interest and penalties, you could also miss out on the opportunity to claim deductions under the old tax regime.

“Some of our high networth clients do not mind shelling out the late-filing fees of Rs 5,000, so they tend to postpone the exercise. However, if you have chosen the old tax regime and are availing of deductions under chapter VI-A (for instance, section 80C, section 80D), 24(b) and so on, you must file returns by the due date, which is July 31,” says Mumbai-based chartered accountant Chirag Chauhan. Else, you will lose out on the tax benefits, resulting in higher tax outgo.

According to the income tax department, the choice of old tax regime can be made only before the due date of filing the return - that is, July 31 - under section 139(1) of I-T Act. This rule is applicable from financial year 2023-24, when the new, minimal exemptions framework was designated as the default regime.

Individual tax-payers need to bear in mind while filing returns that the relevant financial year is 2023-24 and the assessment year is 2024-25. Also, do note that the announcements made in Budget 2024 on July 23 will not be applicable while calculating taxes and filing returns now; these will come into force for FY 2024-25. This apart, here are ten mistakes you must avoid while filing income tax returns this year.

Also read: ITR filing deadline: 8 tips for filing error-free income tax returns at the last minute

Not reconciling Form-16 and Form-26AS dataBefore you start filing your returns, you must download Form-26AS and the Annual Information Statement (AIS), which can be accessed through I-T department’s e-filing portal (www.incometax.gov.in).

The details of tax deducted at source (TDS) and high-value financial and immovable property transactions and so on must match the Form-16 data as well as bank TDS certificates and other financial records. Any mismatch can trigger a notice from the I-T department.

If you discover any discrepancies in these documents, reach out to the tax deductor – for instance, banks, which withhold TDS on the interest earned on fixed deposits, or your employer, who deducts tax from your salary every month – for clarifications and rectifications.

Likewise, submit feedback on errors in AIS. "Many tax-payers have encountered differences in their records and income reported in AIS this year. There is duplication of entries as well, besides other issues. If you come across such glitches, don’t hold up your returns. File your objections and go ahead with filing returns. But ensure that you follow up and get the issues resolved to reduce the chances of tax demands, refund adjustment and litigation," says Mumbai-based chartered account Suresh Surana.

If you pick the wrong form for filing returns, for instance, ITR-1 when ITR-2 was the form relevant for you, you will be seen as – even if inadvertently – having concealed income and transactions that you ought to have disclosed in ITR-2. For example, say, you made capital gains through sale of stocks or had a foreign bank account in 2023-24.

If you use ITR-1, you cannot make these disclosures. You could end up with a notice for non-disclosure from the I-T department. Moreover, selecting the wrong form could also render your return ‘defective’.

Claiming deductions you are not eligible forSince no documentary proofs need to be attached while submitting I-T returns, some misuse this relaxation to secure higher tax refunds. As Moneycontrol has pointed out earlier, some taxpayers tend to fraudulently claim deductions under section 80G on donations made to charitable organisations or deductions under section 80U for disabled taxpayers.

However, this could mean inviting I-T notices, as many salaried individuals have discovered over the last one year. Thanks to the use of AI tools and Annual Information Statement (AIS), the I-T department is able to verify the accuracy of your (faulty) disclosures.

To avoid landing in the crosshairs of the tax department, you need to be completely honest while filing your returns, instead of inviting trouble later.

Relying solely on Form-16 while filing returnsFor salaried employees, Form-16 is the key document while filing returns. However, Form-16 does not display many incomes and transactions.

For instance, your savings account balance would earn interest, which is subject to tax (though savings account interest up to Rs 10,000 is allowed as deduction under section 80TTA). Likewise, you will not see capital gains that you may have made on sale of shares or mutual fund units in your Form-16.

Relying only on Form-16 would mean missing out on reporting these incomes and running the risk of triggering a tax notice for non-disclosure. Ensure that you go through AIS as well as your bank statements and capital gain statements issued by mutual fund intermediaries, and broking houses to make accurate disclosures.

Not disclosing income from previous employerIf you switched jobs during the financial year, you ought to exercise extra caution. Such salaried taxpayers will have dual Forms-16, issued by their previous and current employers.

You must make sure that disclose the income earned from both organisations and do not ignore short deductions of income tax, if any, by any of your employers. The AIS captures all your income details, so income earned from both employers will get populated.

If your ITR does not contain these details, you could end up tax notices for failure to declare all incomes.

Not disclosing foreign assetsSeveral Indian employees, particularly from the IT sector, are often posted abroad. In such cases, they usually have to open bank accounts in their destination countries. However, many miss disclosing these accounts once they come back to India, acquire resident (and ordinarily resident) status and file their ITRs.

Note that you have to disclose these bank accounts even if the balance is nil. Likewise, you have to declare any shares received via stock options from foreign companies, property or pension account that you may have overseas, etc, in the ITR and Schedule FA (foreign assets). "Many tend to believe Indian authorities do not have access to details of assets held abroad, but they do receive such details under information exchange agreements with other countries," says Mousami Nagarsenkar, Partner, Deloitte India.

Non-disclosure of foreign assets can attract a penalty of Rs 10 lakh and, in rare cases, even penal action under the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015. Also, ensure that you file Form-67 for availing of foreign tax credit.

Also read: Avoiding double-taxation: How Form 67 can help you claim foreign tax credit

Not preserving documents detailing deductionsThe new, minimal tax exemptions regime was declared the default tax regime starting from financial year 2023-24. So, all employers adhered to the rule which meant that employees who failed to expressly choose the old tax regime while filing proposed investment declarations in April 2023 saw a higher-than-anticipated tax outgo.

Such employees can pick the old tax regime even at the time of filing returns, but a mismatch in Form 16 and ITR data could lead to notices. Make sure you preserve all the documentary proofs for your deductions to enable you to fend off the queries should they arise.

Not declaring income from capital gainsSince the AIS and Form 26AS contain the complete history of a taxpayer’s transactions, no income will go unnoticed. If you fail to report, say, the sale of shares or mutual fund units, you will get a notice for non-disclosure when the I-T department processes your returns.

Entering wrong personal information, bank account detailsPre-validated bank account details ensure that you receive income tax refunds, if any, on time. Any errors in your bank details would mean a delay. Double-check the account number, IFSC, bank name and other details in your ITR form before submitting the returns. Likewise, reconfirm your name, mobile number, email-ID and other personal information entered in the ITR forms.

Do not ignore the I-T e-return verification processThe process of filing ITR does not end with uploading and submitting the returns online. For your return to be processed by the I-T department, you have to verify it within 30 days of filing. You can easily do this online through the I-T e-filing portal using your Aadhaar, pre-validated bank account, demat account and so on. It is best to complete this process along with ITR submission instead of waiting for another 30 days.

If you do not complete the process within 30 days, the date of verification will be treated as the date of filing returns. So if you verify your returns after 30 days and the July 31 due date has passed by, it will be seen as return-filing post the due date, and you might have to shell out late-filing fees of Rs 5,000 (Rs 1,000 if income is less than Rs 5 lakh).

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.