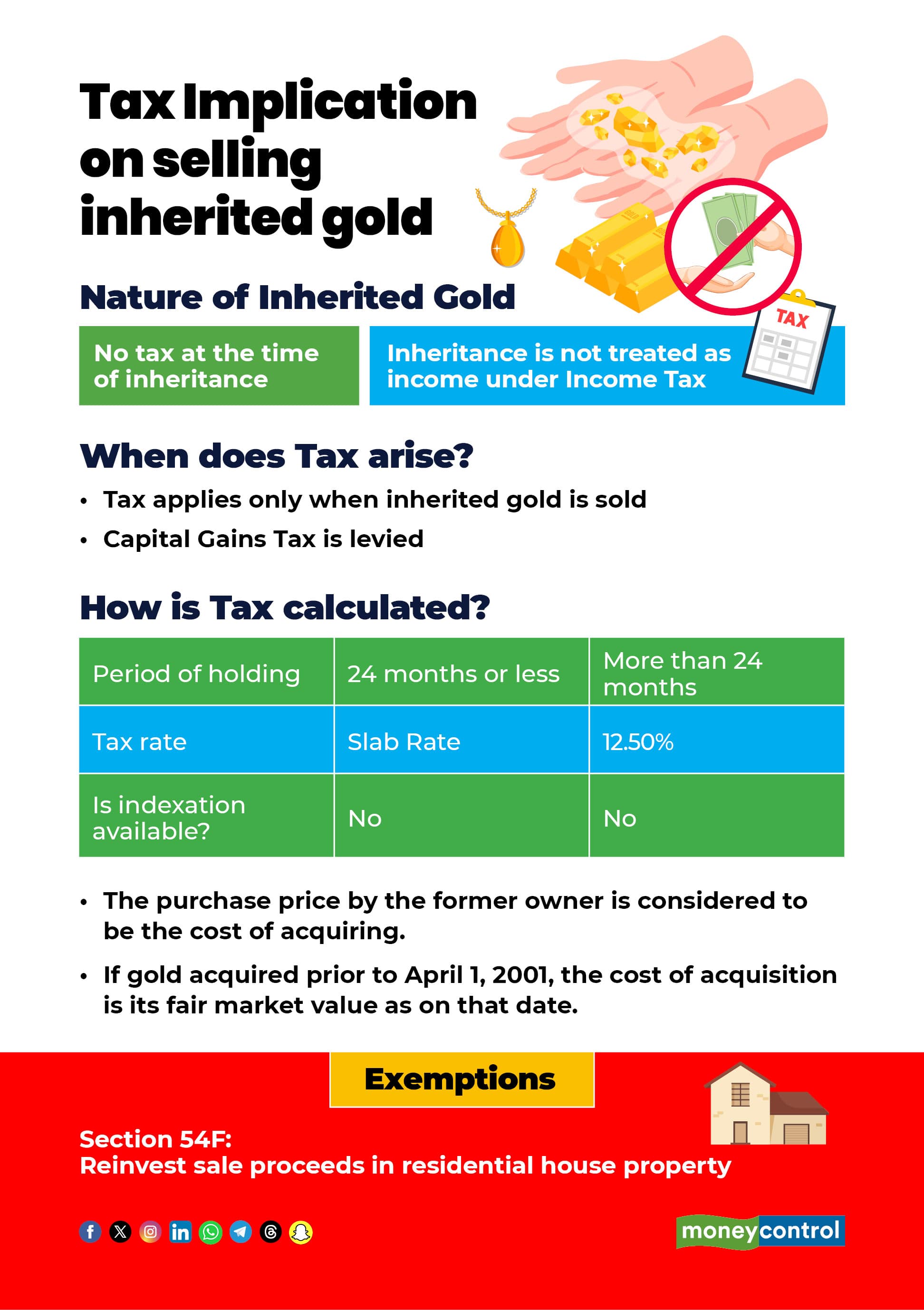

If you have inherited gold jewellery from your parents and are wondering whether it is taxable, there is good news for you! Under Indian tax laws, inherited gold is not treated as income, so no income tax is payable at the time you receive it.

When does tax arise?

The tax aspect comes into play only when you sell the jewellery. In such cases, capital gains tax applies but only on the profit you make from the sale, not on the entire value of the inherited gold.

The gains are taxed as capital gains. “The provision in Section 56(2)(x) of the Income Tax Act, 1961, exempts tax on inherited properties. While there is no tax on any property (including gold jewellery) that is received by way of inheritance, the tax would become payable when any such property is sold or transacted by the assessed,” said Shashank Agarwal, Founder, Legum Solis.

Before July 2024, the tax treatment of inherited gold depended on a 36-month holding period. If the gold was sold within 36 months, the gains were treated as short-term capital gains and taxed as per the applicable income-tax slab. Sales after 36 months qualified as long-term capital gains (LTCG) and were taxed at 20 percent with the benefit of indexation.

From July 2024 onwards, the Finance (No.2) Act, 2024 has changed these rules. The holding period for LTCG has been reduced to 24 months, and long-term gains are now taxed at a lower rate of 12.5 percent without indexation. Gains on gold sold within 24 months continue to be taxed as short-term capital gains at slab rates.

How is tax calculated?

When inherited gold is sold, and capital gains are made, it is liable to taxation. The purchase price by the former owner is considered to be the cost of acquiring. In case the gold was obtained prior to April 1, 2001, then the fair market value as of that day may be adopted. The holding period of both the previous owner and the heir is combined. When this surpasses 24 months, the gain is subject to long-term taxation at 12.5 percent along with surcharge and cess, without indexation. The short-term gains are taxed at the rate of the applicable slab of the individual.

“For assets received by inheritance, gift or succession, the cost to the previous owner is treated as the taxpayer’s cost. Assets acquired before 1 April 2001 may adopt the fair market value as on that date, and the previous owner’s holding period is included to determine the nature of capital gains,” said Nupoor Maharaj, Advocate, Supreme Court.

What are the exemptions and savings options?

The sales of inherited gold can have their capital gain tax reduced or exempted through exemptions. “Section 54F states that in the event that the net sale proceeds are used to invest in a residential house in India and within the specified time limit, the capital gains may either be fully or partially tax-free,” said Ankit Rajgarhia, Designate Partner, Bahuguna Law Associates.

Under Section 54F, capital gains arising from the sale of gold can be exempt if the entire net sale consideration is invested in a residential house property located in India. The investment must be made by purchasing a house either within one year before or two years after the date of sale, or by constructing a house within three years from the date of transfer. The exemption is available only if the prescribed conditions are met, and the maximum cost of house eligible for exemption under this section is capped at Rs 10 crore.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.