US election results significantly influenced global market movements in November. Donald Trump’s presidential victory and Republican control of Congress bolstered expectations of policies aimed at extending US economic and market dominance. Anticipation of tax cuts, expansionary fiscal policies, and a protectionist trade stance propelled the US equity market, with the S&P 500 rising 5.9 percent during the month. The dollar also strengthened significantly, driven by speculation that Trump's fiscal measures might fuel inflation, potentially shortening the Federal Reserve’s rate-cutting cycle.

Emerging markets, however, faced setbacks, as the MSCI EM Index fell 3.6 percent, underperforming the MSCI World Index, which gained 4.6 percent. Concerns over U.S.-China trade tensions weighed heavily on Chinese equities, reflecting broader challenges for developing markets.

Also read | Insurers urge IRDAI to act against automotive dealers’ ‘steep commissions, restrictive practices’

The Fed lowered the funds rate by 25 basis points (bps) in November to a target range of 4.50-4.75 percent, citing disinflation and moderate employment data. However, bond markets experienced limited gains amid concerns that inflationary pressures from likely fiscal policies under Trump could curb future rate cuts.

US equities: a bull run, with caution

The rally in US equities has been remarkable, though concentrated in a few sectors, leading to elevated valuations. Factors like high debt levels, rising interest rates, persistent inflation, geopolitical risks, and a low equity risk premium (ERP) suggest caution. A near-zero ERP implies investors are not being adequately compensated for equity risk, underscoring stretched valuations with elevated price-to-earnings (P/E) ratios for the S&P 500.

Historical data shows that a low or negative ERP doesn’t always lead to weak market performance. In the 1990s, the S&P 500 gained over 400 percent in spite of negative ERPs, supported by robust growth and innovation. While US equities remain a positive long-term bet, adopting a `buy on dips' strategy is prudent amid macroeconomic uncertainties. Conversely, US treasuries appear more attractive, offering favourable risk-reward dynamics for capital deployment.

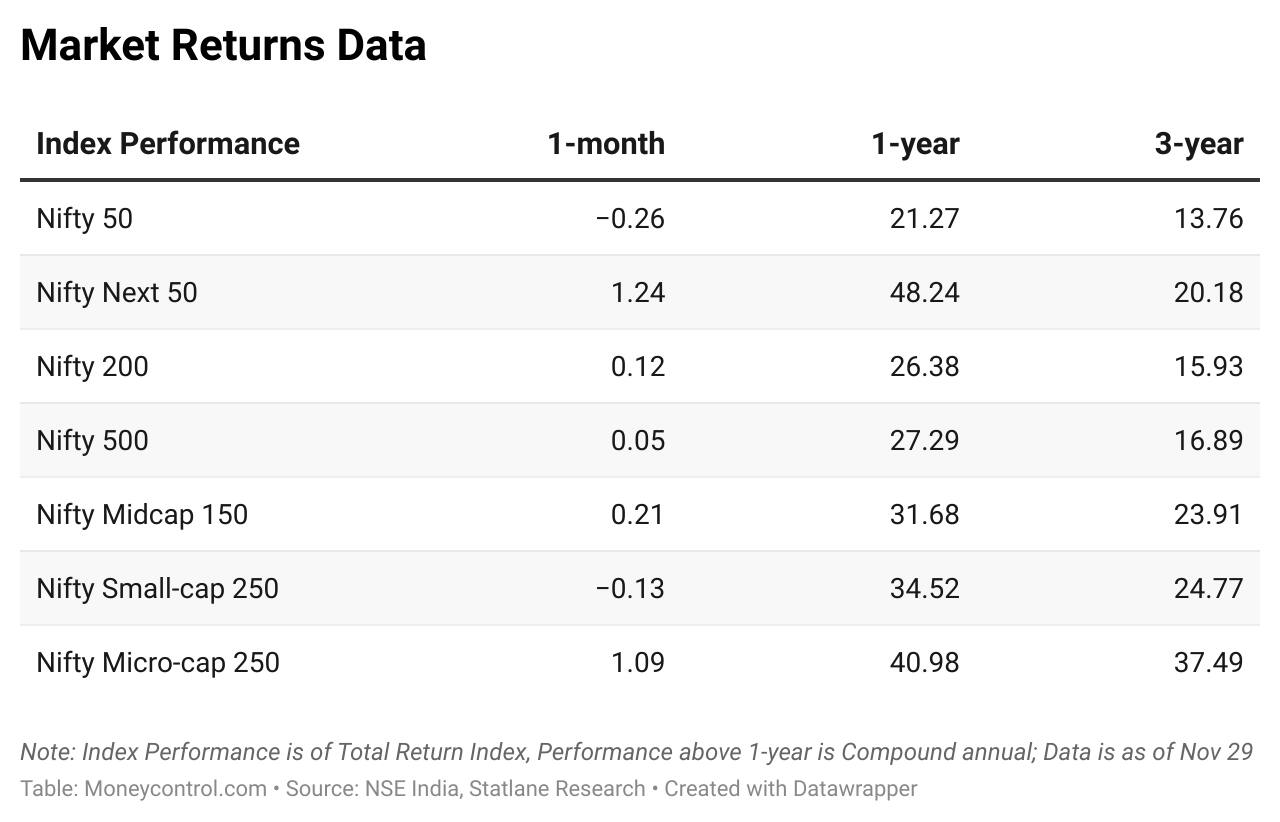

Domestic markets

India’s GDP growth decelerated sharply to 5.4 percent in the September 2024 quarter, down from 7 percent in the previous quarter and 8 percent a year ago. This marks the slowest pace since late 2022, with signs of stress in urban consumption and weaker tax collections. Manufacturing growth plummeted to 2.2 percent, compared to 14.3 percent a year earlier.

Also read | Here's how to teach BASICS of money management to your children

Economists have lowered growth forecasts for FY25, and the Reserve Bank of India (RBI) is expected to follow suit. Elevated consumer price inflation (at 6.2% in October) may delay rate cuts, but liquidity measures like a cash reserve ratio (CRR) cut could help. In the short term, the government and RBI face the challenge of balancing what we call the `impossible trinity' — growth, interest rates, and currency stability.

Foreign exchange and bond markets

India’s forex reserves dropped for the eighth consecutive week, reaching $656.5 billion, partly due to RBI’s market interventions and valuation effects. The rupee remains under pressure amid persistent foreign investor outflows from equities and bonds.

However, Indian bonds offer compelling opportunities:

• A neutral policy stance after significant rate hikes by the RBI (250 basis points since 2022).

• A steady fiscal consolidation path, with the fiscal deficit projected to fall from 6.4 percent in FY23 to 4.9 percent in FY25.

• High yields on AAA corporate bonds (over 7 percent) and potential gains from rate cuts in 2025.

• Growing inclusion of Indian bonds in global indices and increased foreign investor interest.

Equities: pausing the bull run

India’s equity market has surged since the pandemic, with the Nifty 50 and BSE Midcap indices gaining 198 and 351 percent, respectively, between April 2020 and September 2024. Strong corporate earnings, and domestic institutional and retail participation have driven this growth. However, slowing GDP, weaker earnings growth, and stretched valuations signal a pause.

Also read | Your rights to your maternal grandparent's property: What you need to know

Despite near-term challenges, India’s long-term economic drivers remain robust. Its demographic dividend, urbanisation, infrastructure investments, and supply chain diversification would underpin sustainable growth. The IMF projects India’s GDP to grow at 6.1 percent annually over the next five years, positioning the country as the world’s third-largest economy by 2027.

Investors should focus on systematic investments, leveraging dips in the market. Indian equities are likely to experience a time correction rather than a significant price correction, offering attractive compounding opportunities over the long term.

The author is the founder of StatLane, a SEBI-Registered Research AnalystDisclaimer: The views expressed by experts on Moneycontrol are their own and not those of the website or its management. Moneycontrol advises users to check with certified experts before taking any investment decisions.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.