Whether planning for a regular retirement at 60 or early retirement at 45, the assumptions you make will determine the probability of success of the (early) retirement plan.

This is more important for those who aim for early retirement as they have less time to reach their target (between today and chosen early retirement age) and need to ensure that the retirement corpus lasts longer (after retirement).

For example - there are two friends both aged 30. One aims for early retirement at 45 while other wishes for a regular one at 60. Both have a life expectancy of 85. Now the early retiree has 15 years to save the corpus that needs to last for another 40 years (between age 45 and 85). Whereas the regular retiree has 30 years to save the corpus which should be sufficient to last for 25 years (between age 60 and 85).

To ensure you are early retirement ready, you need to ensure that you don’t make wrong assumptions. Because if you do, you run a real risk of running out of money before running out of years.

So what are these assumptions that many naïve early retirees make and which can derail their early retirement plans?

Wrongly assuming average returns every year (Sequence of Return Risk after Retirement)People believe that the average return that they take in their calculations will be earned every year (which never happens). That is, an average return of 11% means 11%, 11%, 11%, 11%... and so on every year. In reality, its more like 15%, -23%, 4%, -8% and so on where the average turns out to be 11%.

And this matters a lot if you have a bad sequence of returns in the initial years.

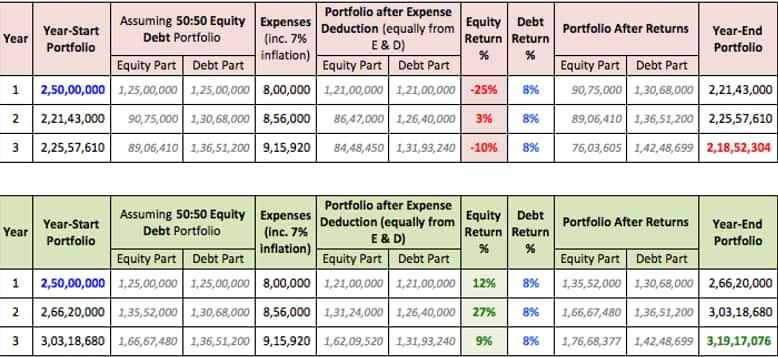

Suppose two friends retire with Rs 2.5 crore today with starting annual expense of Rs 8 lakh. Here is what happens to their portfolio (assumed to be deployed at 50:50 Equity:Debt) for a bad sequence of returns and a good sequence of returns in initial 3 years:

As you can see, there is a big difference in the portfolio size after just first 3 years due to different sequence of returns. The order of returns and how much is the actual asset allocation will impact how long the early retirement corpus lasts.

So those targeting early retirement should never believe that they will get ‘atleast’ the average returns every year. This is the reason it makes sense to de-risk the early retirement corpus as one gets closer to the D-day.

And when making return assumptions, it is always better not to be too aggressive, have reasonable expectations and have a conservatively aligned portfolio when entering the early retirement phase. You never know whether you will get a good sequence or a bad sequence of returns in initial years.

Underestimating Health & Medical Costs‘I am healthy now. I will always be healthy’ - This doesn’t happen.

And when you are in good health, it is difficult to imagine being unhealthy in future. But that is a wrong assumption.

To be fair, during the early phase of early retirement, it’s possible to be healthy and have small healthcare costs. But as one heads towards actual old age, these costs will increase. And planning for these cannot be ignored just because they aren’t immediate for early retirees.

Failing to plan for this spike in the later years of retirement could seriously derail your plans. Additional funds for the unexpected but statistically probable medical expenses need to be accommodated in your corpus when you are still saving to mitigate any medically-triggered financial shocks.

And remember, you will live longer than previous generations. So even if you don’t get hospitalized (for which you might have health insurance), you will have to still spend money on regular medical expenses of old age (that too for several years due to long life expectancy).

Will live frugally later (not today) by changing lifestyle a day after early retirementMany feel that they will drastically cut down their lifestyle expenses when they achieve a basic level of financial independence and take aim at early retirement.

This is easy to say theoretically but isn’t so practical.

Having low expenses is the key to accelerating early retirement but that said, not everyone can do it. And more so when they have lived a life of high expenses. The downgrade isn’t easy and not for everyone.

And also, remember that if you are optimizing your early retirement plan for an extremely frugal lifestyle, then your plan will be vulnerable to unexpected expenses that may come up every now and then. You need to have some buffer.to accommodate any unexpected increase in costs of various things or taxes, etc.

Note - There are few more assumptions that are also applicable to regular retirement plans as explained in this article.All said and done, remember that aiming for early retirement is a wise thing to do because you never know when you might be forced into early retirement. But it still isn’t easy and is vulnerable to several risks if not planned well. As you saw earlier, these risks are real and can derail even the best laid early retirement plans.

So getting your early retirement assumptions right is extremely important.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.