When the features of an insurance policy are the same across companies, how do you pick the best plan? Choose the policy offering the lowest rate, right?

Not quite. It’s not just the premiums that separate one policy from another. Here’s why.

The insurance regulator has mandated standardization in different product categories. Currently, all insurers offer the standard health insurance the Arogya Sanjeevani, in which the product features, exclusions and even policy documents are common among all insurance companies.

Standardized personal accident, home and travel insurance covers, too, would be available from April 1, 2021 as notified by the Insurance Regulatory and Development Administrator (IRDA).

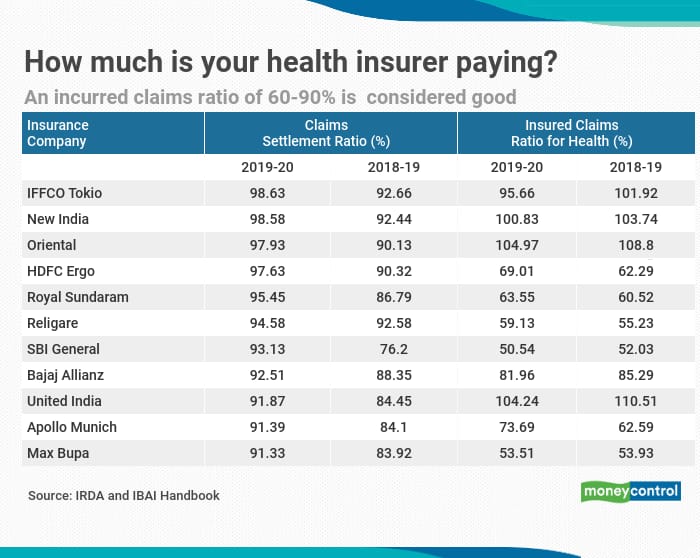

Does your insurer settle your claims on time?This is the most basic check before buying a standardised or any other insurance policy. This shows how much your insurance company pays out, as a percentage of the total claims it gets.

When a high number of claims are outstanding or rejected year after year, then that should be considered as a warning, irrespective of the premium offered by the company.

According to the IRDAI, during financial year 2019-20, insurers have settled 84 percent of the claims registered and have repudiated 8 percent of total number of claims registered and an additional 8 percent of the claims were pending for settlement as on March 31, 2020.

Another matrix is the incurred claims ratio that is the percentage of premiums used to pay claims during the financial year. In simple words, if the company collects Rs 100 as a premium and gives Rs 100 as claim settlement, it is perhaps collecting low premiums. Or, if it pays, say, Rs 50 as claims, then its premium may be usually high. Neither scenario is desirable.

So, an incurred claims ratio of 60-90 percent is desirable.

Is your insurance company on firm ground?It’s not enough that your insurance company pays your claims on time, if its own financial standing is weak. Other parameters such as the company’s financial strength, its ability and willingness to pay the claim, the consistency of paying claims and the ease of procedures also matter.

“More than the price, the company and product are important. Selecting an insurance partner should be based on the quality and the strength of the underlying promise and the consistency,” says Sanjay Datta, Chief-Underwriting, Reinsurance and Claims at ICICI Lombard General Insurance.

An insurer’s solvency ratio, as part of its disclosure of financial statement, is a good indicator on how strong the company really is.

“It is better to go with companies that have a good lineage of products that are long-term in nature such as health insurance, car insurance, etc. For short-term products such as travel insurance, you may compromise on the strength of the company,” suggests Datta.

For instance, the IRDAI disclosed in its annual report that 27 out of 28 private sector general insurers have the required solvency ratio of 1.50 as on March 31, 2020. So, you should avoid opting for companies that have a low solvency ratio.

But how can you measure the strength and consistency of an insurer?

There are two ratios that help us gauge these two parameters. The ratio of claims outstanding and repudiated over a period and the incurred claims ratio help us gauge the consistency of an insurer and the chances of sustenance.

“The claims ratio and the ease of honouring a claim are far more important than the premium,” says certified financial advisor Vivek Damani.

Ease of claimsDatta adds that you should consider whether an insurer offers ease of operations for renewals, technological support, the process for buying a product and making changes or claims.

“Check whether the processes are simple for updating information, renewals and claims if you can find out through the call centre or check through the website,” says Datta.

While the website and the call centre can offer limited understanding of the process, only someone who has dealt with an insurer would know the fine print. “Check in your known circle about their experience with an insurance company,” suggests Damani adding that various online forums can help you assess a particular insurance company.

Limited sum assuredBut before you opt for the category of standardized products, understand that though these offer a good vantage point to assess premium range across insurance companies as the features are the same. However, the disadvantage is that the sum assured is on the lower end of the band. For instance, Arogya Sanjeevani standard health insurance product can offer a maximum sum assured of just Rs 5 lakh only.

“Only first-time buyers are opting for standardised product as they are positioned up to a certain sum assured. They find it easier to compare as the coverage is not different,” says Datta.

Considering that the general insurance penetration in the country is low (0.96 percent in 2019), these standard products have been rolled out to give many their first taste of insurance.

More than the premium, one should opt for a wholesome sum assured, check whether there is any co-payment under claims and network hospitals within your vicinity, suggests Damani.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.