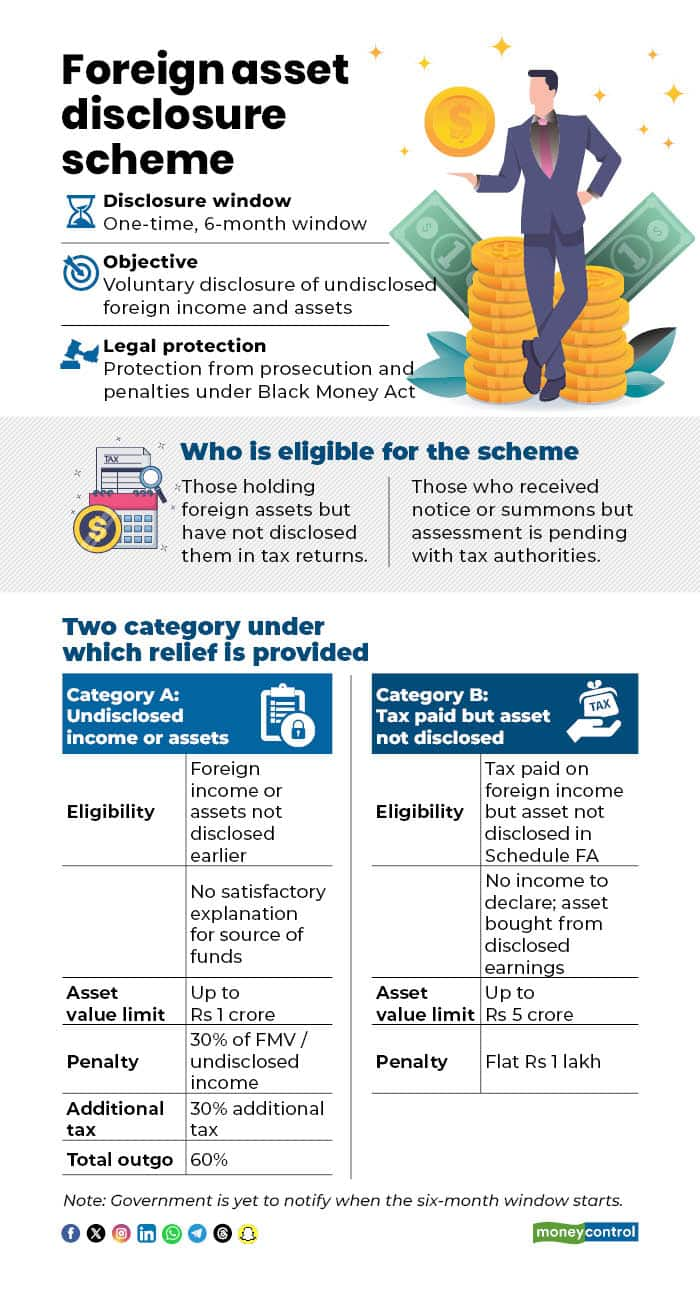

If you have foreign income or overseas assets that were not disclosed in your income tax return, it is important to correct the omission at the earliest. The Union Budget 2026 has introduced a voluntary disclosure scheme to enable taxpayers to disclose foreign asset or income that were either not offered to tax in earlier years or not reported in schedule FA of ITR.

The scheme is primarily intended to provide relief to small taxpayer (e.g. student, employee, relocated non-resident, etc.) who may hold foreign asset or derived foreign income (e.g. foreign bank account, ESOP, retirement account, etc.) but failed to comply with reporting or tax requirements in the past.

“To address practical issues of small taxpayers like students, young professionals, tech employees, relocated NRIs, and such others, I propose to introduce a one-time 6-month foreign asset disclosure scheme for these taxpayers to disclose income or assets below a certain size,” FM said in the Budget speech.

“This scheme is a golden opportunity for the people who have missed (inadvertently/intentionally) declaring foreign undisclosed assets and income. By doing so, not only the payment of penalty and prosecution can be avoided, but also unnecessary litigation costs can be avoided as well,” said Shashank Sharma, Tax Counsel, Supreme Court.

Who is eligible for this scheme?

The scheme would be applicable to taxpayers who did not disclose their overseas income or assets and those who disclosed their overseas income and/or paid due tax, but could not declare the assets acquired.

“The scheme offers a clean exit through voluntary compliance, granting immunity from prosecution once the prescribed payment is made. It is a one-time opportunity to close past lapses and avoid severe consequences under the Black Money framework,” said Alay Razvi, Managing Partner, Accord Juris.

What types of income or assets can be disclosed under the Scheme?

The Scheme covers— undisclosed foreign income; undisclosed assets located outside India; and

specified foreign assets acquired from foreign income when assessee was a nonresident or from income already offered to tax in India, which have not been reported in the relevant Schedule of the return of income.

The Scheme does not apply to income or assets representing proceeds of crime under the Prevention of Money Laundering Act, 2002, or to cases where assessment proceedings under the Black Money Act have already been completed.

The scheme has two categories under which amnesty is allowed

Category A: For complete non-disclosure (up to Rs 1 crore value). Reportable items include undisclosed income from dividends, shares, or any other asset.

Category B: For the taxpayers who disclosed the income and paid tax, but didn’t declare the asset acquired, the limit proposed is up to Rs 5 crore. Reportable items cover foreign bank accounts, stocks, ESOPs/RSUs, real estate, financial interests, or signing authority abroad, even if no income was generated.

What are the cost implications?

Category A: The declarant is required to pay tax at the rate of 30 percent of the value of the undisclosed foreign asset as on 31 March 2026 or of the undisclosed foreign income, as the case may be, together with an additional amount equal to 100 percent of such tax. The total amount payable will be 60 percent of the value of the asset or foreign income, as the case may be.

Category B: In case where the foreign asset was acquired from explained sources but not reported in Schedule FA, "the taxpayer may regularise the disclosure by paying a flat fee of Rs 1 Lakh per asset. Where non-reporting spans multiple years, the fee will be levied only for the first year of non-disclosure for each asset," said Varij Sharma, Partner & Co-Founder, Gravitas Legal.

What happens when you miss the deadline?

“The six-month window (Scheme shall come into force on such date as may be notified by the Central Government in the Official Gazette) offers immunity only if met; missing it triggers Black Money Act consequences like 30 percent tax on undisclosed income, up to 3x penalty (120 percent), Rs 10 lakh annual non-disclosure fine per asset/year, and 6 months to 7 years imprisonment. Assessments can reopen up to 16 years; no Double Tax Avoidance Agreement relief is available,” said Divya Alexander, Advocate, D.M. Harish & Co.

What difference does it make to pay under this scheme?

Suppose Suresh received dividends worth Rs 40 lakh from foreign stocks but did not pay tax. If action is taken under the Black Money Act, he would be liable to a penalty of Rs 10 lakh, a 30 percent flat tax of Rs 12 lakh, and an additional penalty equal to 300 percent along with the continued risk of prosecution. In comparison, if Suresh declares the income under the proposed scheme, he would have to pay a consolidated penalty of 60 percent of the income, or Rs 24 lakh, and would receive immunity from prosecution, making the scheme a far more attractive option.

How to disclose foreign income under Foreign asset disclosure scheme

“The Central Government will notify the date from which the scheme will come into force, the last date for filing declaration and procedure for making such declaration,” said Gopal Bohra, Partner -Tax, N.A.Shah Associates.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.