Garvit Malhan, a 24-year-old product manager at content creation startup Scalenut, thinks tax planning is best left to his CA. The professional he has hired makes sure that Malhan avails tax deductions under Section 80C, 80D and the house rent allowance or HRA exemption.

While this Delhi-based economics graduate-turned-product manager has his tax planning sorted, many early earners find it an overwhelming task. However, the exercise is crucial as you plan for your other financial goals. Remember, tax-planning is not a one-time job, you may need to do it every year. However, it is better to have a financial plan in place. Before you decide on investments to save on taxes, make sure the avenue fits into your portfolio. Tax saving should be incidental and not the primary reason to put money into any particular product.

Ideally, you should commence your tax-planning exercise well in advance and complement this with your overall investment planning. Many leave it till the eleventh hour to work on their tax burden. But mind you, it is not a one-day activity.

Here are a few points that can be kept in mind if you are new to this vital activity.

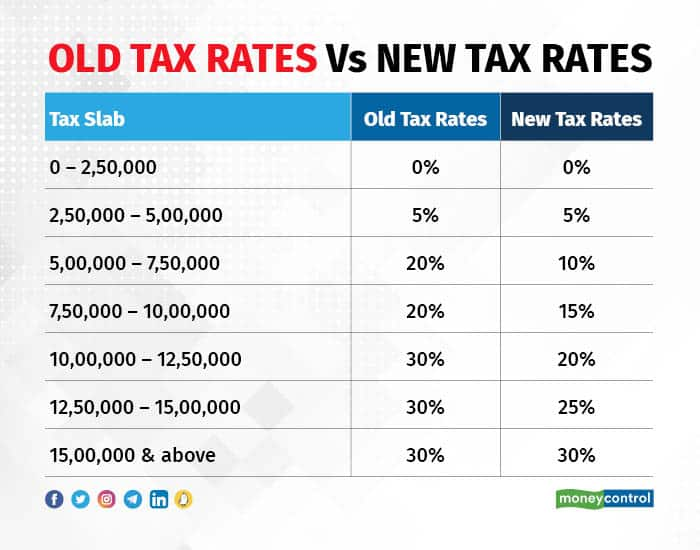

1. Old tax regime versus new tax regimeThis is a relatively new dilemma: Should one opt for the old tax regime or the new one? The new tax regime, introduced in the budget of 2020, differs from the previous one in two ways. For one, it has more slabs with lower tax rates. And two, all the major exemptions and deductions available to taxpayers in the existing (old) system are not allowed under the new one.

While deciding which regime to opt for, many would compute the tax payable by them according to the different slab rates under both regimes to decide which one they should plump for. But that’s not the correct approach, explains Alok Aggarwal, partner, direct tax, Deloitte.

Although the new tax regime offers slabs at a lower rate of tax, it deprives you of deductions under Section 80C and Section 80CCD, standard deduction and even the house rent and the leave travel allowance (LTA) exemption. Thus, it may end up making your taxable income a lot higher compared to the one computed under the old method.

One can, however, change the tax regime they file their income tax return or ITR every year.

The first step towards tax planning is understanding the components of your salary slip. “Finding out what comprises your salary and if tax is being deducted on your income (TDS), helps you plan to save tax,” says Harshvardhan Roongta, principal, Roongta Securities.

Your salary or the cost to the company (CTC) includes basic salary, HRA and contribution towards the provident fund. Knowing what parts of your salary can be exempted (such as HRA, LTA, etc) from being considered taxable will help you start your tax planning as soon as you receive your first salary and not wait till December for your employer to ask for proof of investments in tax-saving products. This will help ease your financial burden as you can spread your tax-saving investments over a longer duration.

3. Know how to file your returnsThere are various ways to file your ITR apart from doing it directly on the incometaxindia.gov.in website. Those confident of filing their ITR themselves can do so via a number of intermediaries authorised to do so. You can check the list of such e-return intermediaries on www.tin-nsdl.com. Many of them operate e-filing websites such as taxspanner.com, makemyreturns.com, cleartax.in, myITreturn.com, and Quicko.com.

These offer various plans; you can choose one according to your requirement.

If not so confident and feel the need for assistance, one can avail of professional help from chartered accountants for fees of typically Rs 500-1,500.

4. Know where you can avail tax deductionsHere are some of the basic exemptions that can be availed of by anyone starting out on their earning journey:

1. All salaried individuals are eligible to claim the standard deduction of Rs 50,000 while filing their ITR.

2. A deduction of Rs 1,50,000 under Section 80C can kick in for individual contributions to employees’ provident fund, public provident fund (PPF) or an equity-linked savings scheme to avail this deduction.

3. All first-time earners should own a personal health insurance cover, apart from the one provided by their employer. This will also help them avail a maximum deduction of up to Rs 25,000 under Section 80D.

4. Another instrument that can be looked at is the National Pension Scheme (NPS). An individual can invest up to Rs 50,000 annually to avail deduction under Section 80CCD.

5. If a student had taken a higher education loan, s/he can also avail deductions under Section 80E for interest paid on the borrowed amount till the time of the repayment of the loan or eight years, whichever is earlier.

6. One can also avail tax benefits under Section 80G for donations made to entities recognised for availing such deduction under the Companies Act, 2013.

5. Align your tax planning with your financial goalsEven though timely tax planning is important, investment planning still tops the priority list. One should always fix their financial goals first and the right way to approach tax planning is to align it with your short-term and long-term financial goals.

For instance, you should not blindly put all your money in a PPF just because it allows you to avail tax benefits under Section 80C. PPF comes with a 15-year lock-in and would block your money if needed for an emergency in the near term.

Similarly, ULIPs or unit-linked insurance plans come with a five-year lock-in period, and life insurance policies can be unfriendly too in terms of availing the benefits while surrendering your policy before two years.

Allocation in instruments like PPF or NPS can be done for longer-term goals because such tax instruments cannot be prematurely redeemed under any circumstances, explains Vishal Dhawan, founder, Plan Ahead Wealth Advisors.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.