For many investors, the FIRE movement, Financial Independence, Retire Early, sounds like the perfect escape plan, especially freedom from the 9-to-5 grind. Save aggressively, invest smartly, and break free from work decades ahead of schedule. But once real-life expenses, family responsibilities, and rising costs enter the picture, the classic FIRE formula often feels difficult to follow.

This is where flexibility becomes important. Instead of forcing a rigid retirement rule, alternatives like Lean FIRE, Coast FIRE, and Barista FIRE, are emerging as more practical alternatives, especially for investors who want financial independence without extreme sacrifice.

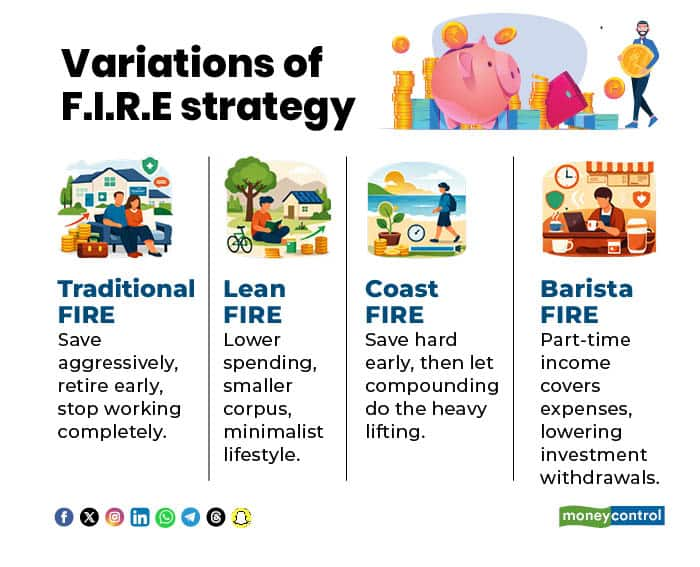

Understanding the Traditional FIRE Model

The FIRE retirement strategy rests on three pillars- saving 50-70 percent of income, living a frugal lifestyle, and investing wisely, usually through low-cost index funds.

The logic is straightforward. You drastically raise your savings rate by cutting expenses, then invest that surplus in diversified, low-cost funds so compounding works in your favour. Index funds matter here because they reduce the risk of costly investment mistakes and high fees eating into long-term returns.

But before any of this works, one key question needs answering: how much money do you actually need to retire early?

Most FIRE followers rely on the Rule of 25. This rule says your retirement corpus should be at least 25 times your first-year post-retirement expenses.

In simple terms, if you need Rs 12 lakh a year after retirement (Rs 1 lakh a month), your target corpus becomes (12 lakh x 25) Rs 3 crore.

This is the well-known 4 percent withdrawal rule. If you withdraw 4 percent annually from a Rs 3 crore corpus, you generate Rs 12 lakh in the first year, with the rest remaining invested. Over time, withdrawals are adjusted for inflation.

However, the FIRE framework that suggests saving 25 times annual expenses often falls short in India.

This is because the assumption of low inflation does not hold true in the Indian context. Lifestyle costs, housing, and healthcare expenses typically rise by 6-9 percent annually, eating into the retirement corpus faster than investors expect. Under these conditions, the retirement corpus can run out much earlier.

Alternatively, investors can aim for a higher safety buffer. For instance, instead of saving 25 times annual expenses, one may consider targeting 35 or even 40 times annual expenses.

Based on this calculation, the required retirement corpus rises to Rs 4.2 crore at 35 times annual expenses (Rs 12 lakh × 35) and further to Rs 4.8 crore at 40 times annual expenses (Rs 12 lakh × 40), compared to Rs 3 crore under the 25X rule. This higher buffer helps absorb inflation shocks, prolonged weak market phases, and rising healthcare costs, reducing the risk of running out of retirement savings.

When Traditional FIRE Becomes a Pain Point

There’s an important catch - saving 50-70 percent of income is not easy when you’re managing EMIs, family responsibilities, children’s education, and rising living costs.

As these rules are based on long-term US stock and bond market data, applying them blindly to Indian conditions, where inflation, healthcare costs, and market behaviour differ, can make FIRE harder to execute than it appears on paper.

This is where FIRE variations step in, not to reject the idea of financial independence, but to reshape it into something more achievable.

Variations of F.I.R.E

Lean FIRE: Retiring With Lower Expenses

Lean FIRE focuses on one clear lever, reducing post-retirement expenses. Say, if your current annual spending is Rs 12 lakh, Lean FIRE pushes you to consider whether you can retire on Rs 10 lakh, Rs 8 lakh, or even less. That directly lowers the corpus you need.

For instance, if you consider post-retirement expenses as Rs 8 lakh per year, then your required corpus (Rule of 25) comes down to Rs 2 crore.

When can this work? This approach is tough. Inflation pushes expenses up, and medical costs tend to rise with age. But some costs, office commute, work clothing, frequent dining out, may fall after retirement.

Thomas Stephen, Director & Head Preferred, Anand Rathi Shares and Stock Brokers says, “This method probably suits those individuals who are very clear about having a minimalist lifestyle for their entire lives. Therefore, to achieve financial independence here would require a much smaller corpus. Freedom of time is the main priority here.”

Coast FIRE: Save Early, Then Slow Down

Coast FIRE takes a very different approach. Instead of trying to fully retire early, you front-load your savings. In this case you save aggressively in your 20s and 30s, then shift to a lower-stress job later, one that covers day-to-day expenses while your accumulated corpus continues to grow untouched.

Let’s understand with an example; Sunil, a 25-year-old investor with annual expenses of Rs 12 lakh; he invests Rs 30,000 a month through SIPs, increases the investment by 15 percent every year, and earns an expected return of 12 percent per annum.

By age 40, the investor accumulates a corpus of around Rs 3.5 crore. At this stage, he switches to a less demanding job that pays enough to meet household expenses. The original corpus remains invested.

By age 60, that Rs 3.5 crore grows to approximately Rs 23.5 crore, purely through compounding. At this point, he can fully retire, with the corpus supporting expenses well into later life.

When this can work? Industry experts say the key discipline here is not touching the corpus for big-ticket expenses like cars, homes, or luxury travel. Any withdrawal breaks the compounding engine. “The basic idea here is to go on full throttle on one’s investments early on until the returns earned by the portfolio alone is good enough to reach the desired retirement corpus amount. At this inflection point, where portfolio returns will suffice future growth, the individual will stop further retirement contributions,” explains Stephen.

Coast FIRE works well for investors who can save aggressively early and value work-life balance over chasing peak salaries forever.

Barista FIRE: Don’t Quit Work Completely

Barista FIRE is the most flexible of all. The idea is simple: don’t stop working entirely.

Instead, you earn supplemental income through part-time work, freelancing, consulting, or teaching. This income covers part of your expenses, reducing how much you withdraw from your retirement corpus.

Take Sunil’s case. If his post-retirement annual expenses are Rs 12 lakh, earning Rs 30,000 - Rs 40,000 a month through part-time work adds up to Rs 3.6- Rs 4.8 lakh a year. This means he needs to withdraw only Rs 7.2 - Rs 8.4 lakh annually from his retirement corpus, instead of the full Rs 12 lakh. Lower withdrawals help the corpus last longer and reduce stress during market downturns.

The key is choosing meaningful work, something you enjoy and can sustain. Otherwise, early retirement may not feel fulfilling. Stephen adds, “This would benefit someone who does not prefer the pressures of full time employment but enjoys working or seeks fulfillment through organizational structure.”

Bottom Line

The biggest takeaway is this: FIRE is not one-size-fits-all.

Instead of chasing a rigid rule, investors should:

· Be realistic about expenses and inflation

· Choose a FIRE variant that fits their lifestyle and career stage

· Focus on disciplined investing through low-cost, diversified funds

· Avoid withdrawing from long-term investments prematurely

Financial independence is not about quitting work at any cost. It’s about building options. Experts say, depending on the individual, these versions of FIRE allow greater flexibility and practicality, with the aim of “Living Freely” rather than “Retiring Early” taking precedence.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.