PhysicsWallah has approved ESOP grants worth around Rs 500 crore, underlining a strong push to reward and retain employees amid its robust financial performance. Issued under the company’s 2025 ESOP plan, the stock options are designed to link employee wealth creation with the company’s long-term growth.

However, while the ESOP grants signal generous rewards, employees must be mindful of the tax liabilities that arise at the time of exercising these options.

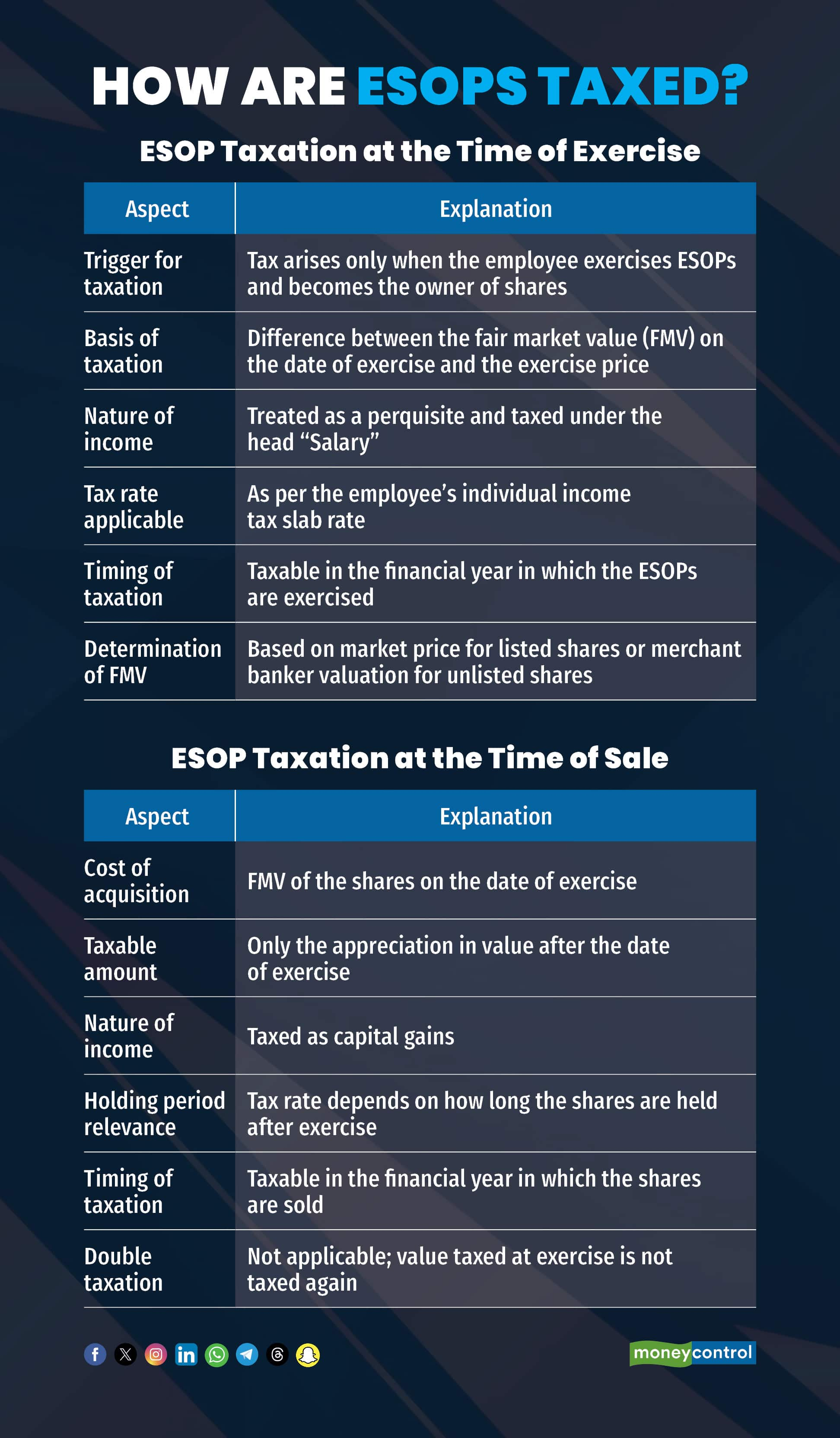

Tax Implications on ESOP Exercise

In India, an ESOP has tax implications in the hands of the employees only when they decide to exercise and own the shares.

"Taxable value of the ESOP is calculated as the difference between the fair market value (FMV) of the shares on the date of the exercise (or at the value determined by a merchant banker not earlier than 6 months from the date of exercise) and the exercise price at which the ESOPs are being offered to the employees and such difference is taxable as a perquisite under the head of salary,” says SR Patnaik, Partner (head - taxation), Cyril Amarchand Mangaldas.

The value of the perquisite so calculated is added to the taxable salary of the concerned employee and tax is calculated as per the income tax slab rate applicable to the employee. Hence, the employees can estimate the tax payable by multiplying the perquisite value and the applicable tax rate applicable to them. They can also seek guidance from their internal HR or from their personal tax advisors too.

For example, an employee exercises ESOPs offered at Rs 100 per share when the FMV on the date of exercise is Rs 250, as determined by a merchant banker. The Rs 150 difference is treated as a perquisite and added to the employee’s taxable salary. If the employee falls in the 20 percent tax slab, the tax payable on this ESOP benefit would be Rs 30 per share, payable in the year of exercise.

Particularly in the case of ESOPs, the employee can exercise the option by payment of a discounted price, known as the ‘Exercise Price’ for the allotment of shares.

For calculating the tax liability arising on account of ESOPs, the employee would need to be aware of the FMV of the share. While in the case of listed companies, this data is readily available in the public domain, for unlisted entities, this information would need to be obtained for accurate calculation of taxes.

“Where the taxes on such ESOPs are significant owing to the quantum of options exercised and the discount availed on such exercise, employees may opt for the ‘Sell-to-cover’ mechanism, where part or whole of the shares allotted are sold to cover the taxes deductible. This helps to reduce the impact on the cash flow from their regular salary income,” says Shilpi Jain, Partner, Ved Jain and Associates.

The Dual Tax Event: Exercise vs. Sale

It is important to understand that there is no double taxation in the case of ESOPs, whether on the date of exercise or the date of sale. “At the point of exercise, the benefit up to the FMV of the share is taxed in the hands of the employee as ‘salary income’. On the subsequent sale, this FMV is considered as the cost and only any additional upward movement in price is taxed as ‘capital gain’ income,” says Jain.

For example, if an employee paid Rs 10 as an exercise price for a share whose FMV is Rs 100 on the date of exercise, the perquisite taxed on exercise will be Rs 100-Rs 10= Rs 90. If they sell the share on the same date, no further amount shall be taxed as capital gain. However, if they sell the share on a later date when the FMV increases to Rs 150, only Rs 50 will be taxable as ‘capital gain’ and the tax rate on such capital gain will depend on the period of holding for such share from the date of exercise.

For listed ESOPs, you can sell the shares once they are exercised and credited to your demat account, as long as there is no lock-in. ESOPs usually do not have a lock-in after exercise, especially in listed companies. However a lock-in may apply if specified in the company’s ESOP plan, during IPO periods, or due to insider-trading rules.

Timing ESOP Exercise for Lower Tax

It would be advisable for the employees to look for deriving the maximum benefit instead of minimising the tax.

“In case the employee is very bullish about the company, it may be advisable to acquire the shares immediately and hold such shares for a longer period of time so that the FMV is low when shares are acquired and thus, lower tax paid as salaries and earn higher capital gains on which the tax payable is lower at 12.5percent,” says Patnaik.

This strategy aims to shift the majority of the profit from high-taxed salary income to lower-taxed long-term capital gains.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.