It has been over seven years since mutual funds introduced direct plans. Although direct plans were introduced with the aim of helping knowledgeable and self-aware investors access mutual funds without having to pay distributor charges, over time, registered investment advisors (RIA) too started routing their clients’ investments through them. Industry officials say that a majority of the inflows in direct plans come from those who invest by themselves – directly through fund websites or through online platforms and apps.

Significant cost savingsDirect plans result in significant cost-savings over a long period of time. Assume that you invest Rs 5 lakh in an equity fund over a 20-year period that gives you, say, 13 percent returns compounded. Let’s say the scheme’s regular plan charges an expense ratio of 1.5 percent for the regular plan and 1 percent for its direct option. After 20 years, your investment in the direct plan gives you Rs 48.23 lakh and your regular option amounts to Rs 44.10 lakh. That’s a difference of Rs 4.12 lakh or 9 percent!

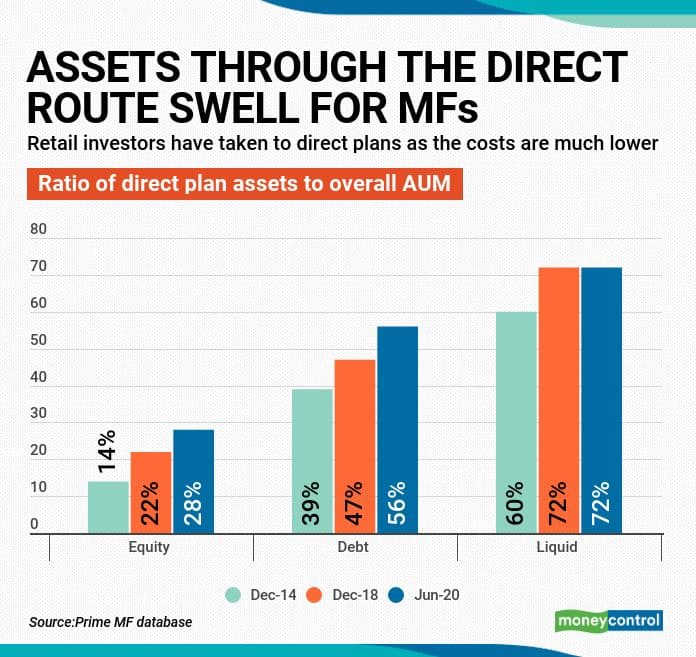

For this reason, large investors such as companies and high networth individuals were quick to latch on to direct plans. Nearly 60-70 percent of investments in liquid funds have consistently been in direct plans. Direct investments in equity funds –retail investors’ favourite avenue – have been slow to pick but have gained traction consistently.

But, in trying hard to save costs, you could land into greater trouble if you choose the wrong fund.

If you are the sort that chooses to invest in mutual funds directly, without anyone’s help, then read on to check if you make the cut.

Do you understand how mutual funds work?Ask yourself: are you game for the gyrations in the NAV (net asset value) of a mutual fund depending on market moves? If you are clueless about where to start, which funds to invest in, you are not suited to invest in direct plans all by yourself. “It takes 3-4 hours to get a good understanding of a mutual fund: which are the various categories, why mutual funds are linked to markets and so on,” says Neelabh Sanyal, Chief Operating Officer, Kuvera.

One way of getting the most out of your mutual fund is to set goals for yourself. Make a plan with details about why you need to invest and when you need the money. Work backwards to determine how much you would need to invest. “If your goal is just about three months away, you might not even need a mutual fund. A simple bank fixed deposit can be a better option. But if your goals are more than five years into the future, then you can park sums in equity funds,” says Neelabh.

If you invested in a gold exchange-traded fund, an international or even a government securities scheme in the last one or two months, then you might have been lured by their recent performances. A scheme’s track record is one of the easiest available indicators to track its health. But it can also be the most misleading. Various fund research firms publish star ratings and rankings, but all of them are based on past results. “There have been plenty of instances that a five-star rated scheme starts performing badly from the time you invested in it. Investing based on star ratings is like investing by looking at the rear-view mirror,” says the head of sales of a large fund house, requesting anonymity.

Equity schemes that got sold at online platforms such as Groww (for the month of July) and Kuvera (sales in the past three months) suggest that many of their customers have invested in recent outperformers. Examples include Nippon India Pharma, Parag Parikh Long Term Equity, Tata Digital India and Mirae Asset Emerging Bluechip. Incidentally, many of these funds have also done well in the past one year. The question is: do DIY (do-it-yourself) investors opt for these schemes as they suit them the most or are they just chasing recent performance?

While many online platforms such as Kuvera insist on customers taking a risk profile test, the reality is that investors are free to invest in any scheme. Neelabh of Kuvera says that the platform constantly sends investor education communication to its customers, ensuring that customers understand the importance of buying the schemes that suit them the most.

Do you get excited about newly launched schemes?Keeping portfolios simple is a good way for DIY investors to not fall into the classical traps of investing. One way of doing this is to avoid new fund offers (NFOs). The lure of NFOs may have gone down in recent years, but many investors still get drawn to the marketing blitz that accompany new rollouts. Investing in multiple NFOs over the years is often the cause for many of our portfolios getting bloated with as many as 20-30 schemes. Says Vinayak Savanur, founder of MoneyMintingMantra, “In rising and bull markets, some fund houses will launch a series of funds. Not only NFOs, you should keep away even from funds that have been around for only one or two years, as a rule.”

The other way to keep your portfolio simple is to stick to asset allocation and passive funds such as index and exchange-traded schemes. “Some investors choose only index funds, because they aren’t chasing alpha (outperformance) and then, perhaps just one or two AAA-rated debt funds,” says Vishal Kapoor, CEO of IDFC Asset Management. Vishal also suggests avoiding funds based on ‘hot’ themes. Bloated portfolios become difficult to track after a point and result in a tax burden when you decide to sell and consolidate your portfolio.

Are you tired of doing your own research?There’s a lot of advice from online platforms and apps. Many such platforms also allow you to invest in direct plans. Are you able to make sense out of those? Sharad Singh, founder of Invezta.com, suggests a method: “In the last three-odd months, when Nifty 50 index fell from 12,200 to 7,610 and then came up to 11,300 a few days ago, what did you do? If you did nothing, then you perhaps do not really need a human advisor to guide you. But if you reacted sharply, say you withdrew in panic or got euphoric and started trading in shares or worse, options, then perhaps, online advice is not for you. You need a physical advisor to hold your hand.”

It all boils down to our behaviour. Vishal takes a harder look at investment advice available online and equates that to self-medication. “Too much online research should be avoided as it cannot substitute expert advisor-based research. While you may get some success, you cannot extend it to more complex situations,” says Vishal.

Online DIY investment done directly with fund houses or through online platforms may be good enough for millennials in their initial earning years. But as incomes rise and responsibilities increase, they should hire an RIA and invest directly based on her advice.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.