Capital gains arise when an investor sells an asset such as shares, mutual funds, bonds or real estate, at a price higher than the purchase cost. While gains can boost returns, tax treatment often decides how much actually lands in the investor’s pocket. Understanding the rules upfront can help avoid unpleasant surprises at the time of filing returns.

Two types of capital gains: LTCG and STCG

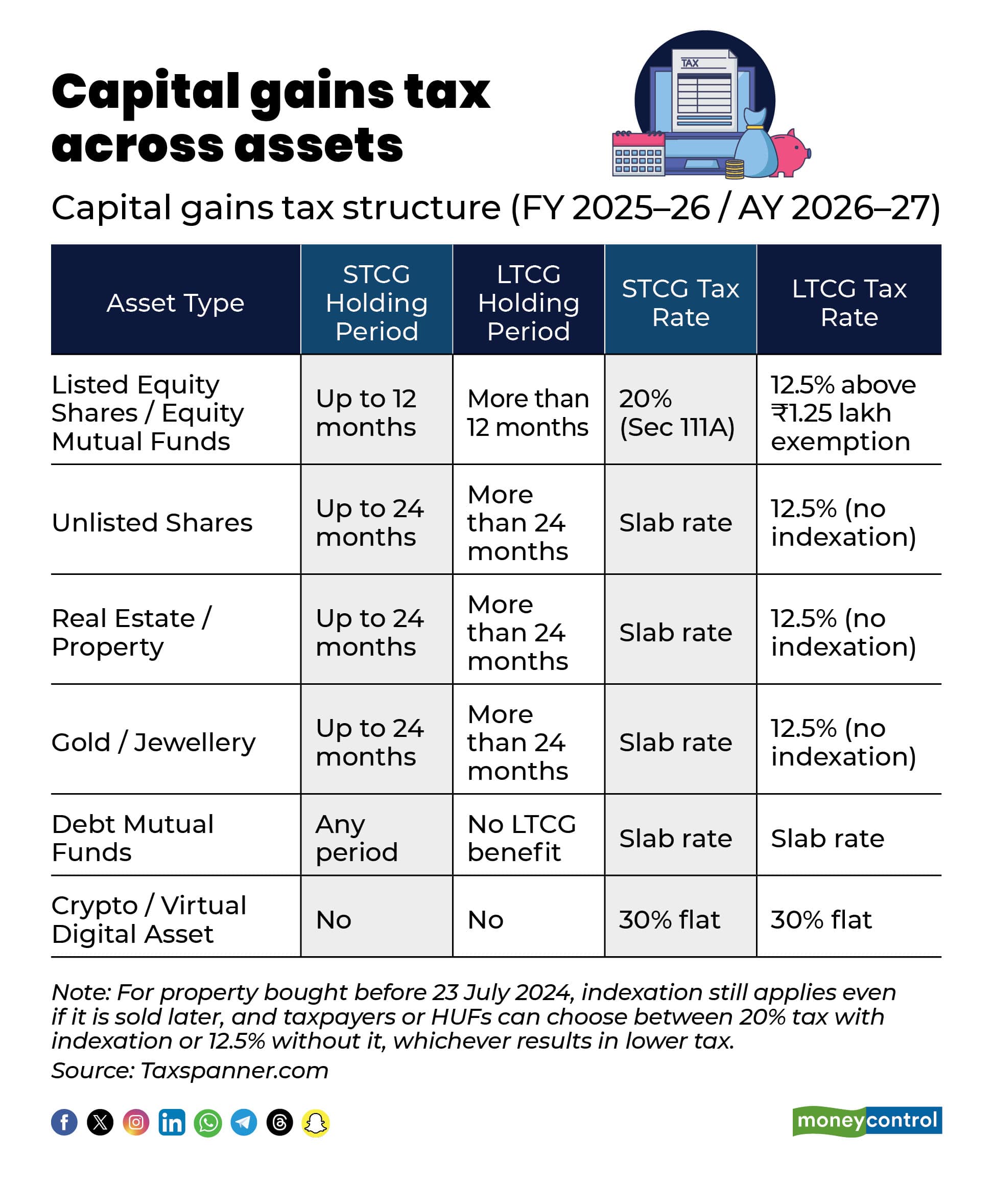

Capital gains are broadly classified into long-term capital gains (LTCG) and short-term capital gains (STCG), depending on how long an asset is held before sale. The holding period varies across asset classes, 12 months for listed equities and equity mutual funds, and 24 months for other assets such as property, unlisted shares and debt instruments. Tax rates differ sharply between the two, making timing critical.

What is indexation?

Indexation is a method that adjusts the purchase cost of an asset for inflation, reducing taxable gains. While indexation was earlier available for several asset classes, recent tax changes have significantly curtailed its use.

Interim Budget 2024 removed indexation benefit on property sales. The indexation benefits apply only to real estate property brought before Jan 23, 2024, while most financial assets no longer enjoy this inflation adjustment.

How different assets are taxed

For listed equity shares and equity mutual funds, gains become long-term after 12 months. LTCG is taxed at 12.5 percent beyond the Rs 1.25 lakh annual exemption, while STCG is taxed at 20 percent.

Debt mutual funds purchased after April 1, 2023, are taxed at slab rates regardless of the holding period, reducing their tax efficiency for long-term investors.

Listed bonds and debentures attract 12.5 percent tax on long-term gains without indexation, while short-term gains are taxed at slab rates. Unlisted shares qualify as long-term after 24 months and are taxed at 12.5 percent.

For real estate, property held for over 24 months qualifies as long-term. Properties acquired after July 23, 2024, attract LTCG tax at 12.5 percent without indexation, while short-term gains are taxed as per income slabs.

Set-off provisions for capital losses

The Income Tax Act provides specific rules for setting off and carrying forward different types of losses.

• STCL can be adjusted against both short-term and long-term capital gains.

• LTCL can only be adjusted against long-term capital gains.

• Non-speculative business losses (like F&O trading) can be set off against any income except salary.

• Speculative losses (like intraday trading) can only be set off against speculative gains.

If losses remain unadjusted in the current year, they can be carried forward, provided the return is filed on time:

• STCL & LTCL: Can be carried forward for 8 years and set off only against eligible capital gains.

• Non-speculative business losses: Can also be carried forward for 8 years, to be adjusted against any business income, whether speculative or not.

• Speculative business losses: Can be carried forward for 4 years and set off only against speculative business gains.

These rules help investors and traders plan their taxes efficiently and make informed decisions around asset rebalancing and exit strategies

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.