With Budget 2026 around the corner, expectations are building around a possible increase in the National Pension System (NPS) tax deductions. A higher limit, from Rs 50,000 to Rs 1 lakh, could benefit salaried and self-employed individuals seeking additional tax-efficient retirement avenues, while offering meaningful relief to middle-income earners.

The move may also help align India’s retirement incentives more closely with global practices. However, questions remain on whether enhanced NPS benefits would divert savings from EPF, PPF, or insurance products, and whether tax tweaks alone can meaningfully bridge India’s widening retirement savings gap. If NPS deductions are increased, who stands to benefit the most?

According to Rajarshi Dasgupta, Executive Director (Tax) at Aquilaw, salaried employees shall benefit most from higher NPS deductions due to their current tax profiles. Whereas the self-employed could benefit more in terms of increased retirement participation if policy adjustments target them, too.

“Reduced tax liability can be significant for salaried individuals who otherwise fall into higher tax brackets. The self-employed currently have less automatic retirement coverage, with no EPF benefits, and lower participation in formal pension plans.

“If a higher NPS deduction limit were introduced specifically for them, it could significantly boost retirement savings behaviour, since this group constitutes a large share of India’s workforce and is presently under-covered,” said Dasgupta.

For government employees, he reasons that they already often have structured pension setups (including NPS or legacy pension options), so incremental tax deductions alone don’t change their tax burden as much. The main value for them is in long-term retirement income rather than tax relief per se.

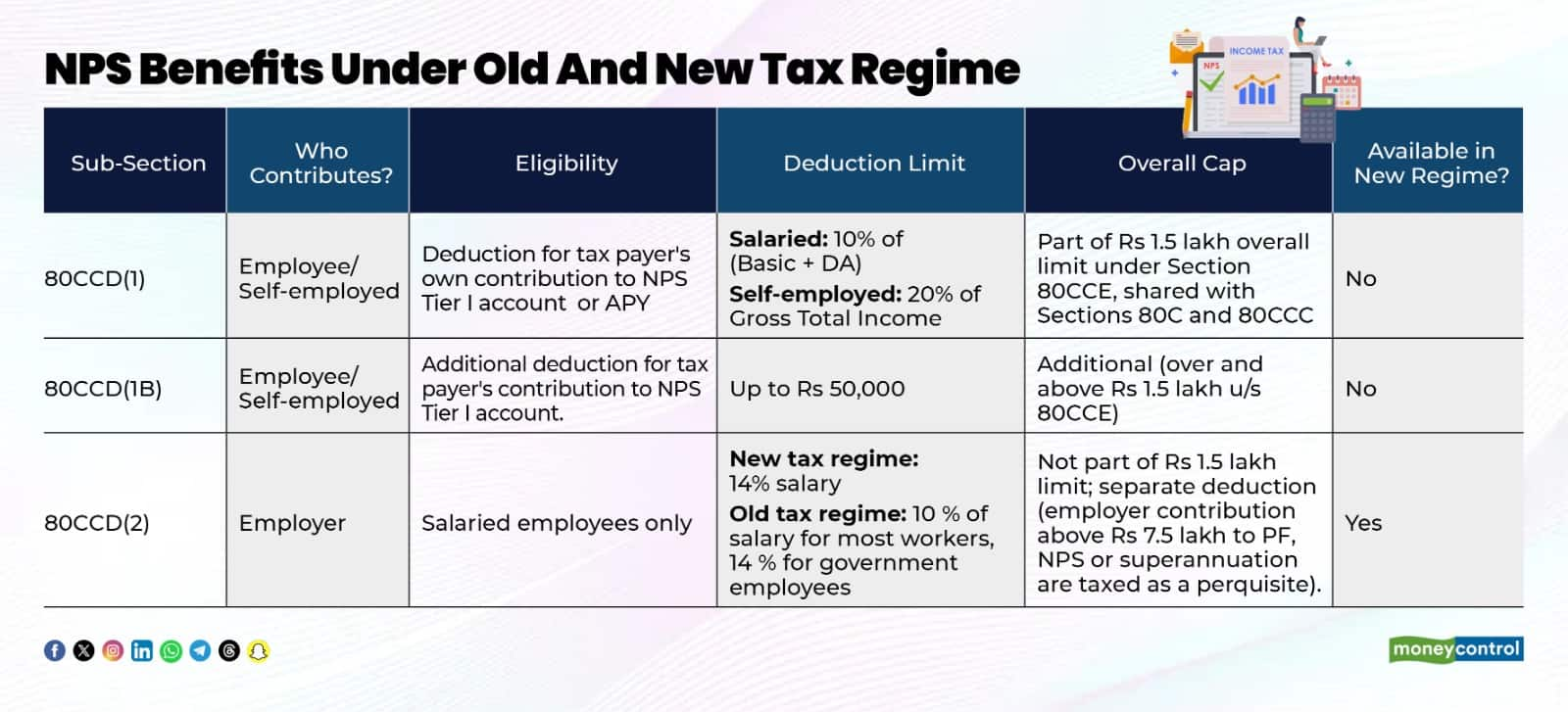

Employer contributions to NPS are eligible for tax deduction under Section 80CCD(2), up to 14 percent of basic salary plus DA in the case of government employees, while the limit for private-sector employees is 10 percent.

Separately, individuals—including private-sector employees and the self-employed—can claim an additional deduction of up to Rs 50,000 under Section 80CCD(1B), over and above the Rs 1.5 lakh cap under Section 80C of the Income Tax Act.

“The incremental relief from increasing the NPS cap is proportional to one’s marginal tax rate— higher earners save more per rupee contributed. But for middle-income taxpayers, even a modest increase could shift some of their income into a lower effective tax bracket,” says Dasgupta.

He argues that if the limit is raised to Rs 1 Lakh or Rs 1.2 Lakh, a middle-income earner (say Rs 8-15 lakh per year) could reduce taxable income by an extra Rs 50,000-70,000 over the current cap, which could translate to Rs 10,000-21,000 in immediate annual tax savings from the incremental deduction alone.

Can a higher NPS limit reduce reliance on EPF, PPF, or insurance?

A higher tax deduction limit would indeed benefit salaried and self-employed individuals seeking additional tax-efficient retirement avenues. However, could this exemption lead to reduced dependence on other employee-linked pension schemes like the Employee Provident Fund (EPF), the Public Provident Fund (PPF), or insurance-linked savings?

Rohitaashv Sinha, Partner, King Stubb & Kasiva, Advocates and Attorneys, said, “An enhanced NPS limit would not replace EPF, PPF or insurance-linked products, but would rebalance retirement planning by promoting market-linked, pension-oriented savings over fragmented instruments.”

Dasgupta also seconds the thought. “Higher NPS deductions could channel some retirement savings away from other instruments toward NPS, but fundamental differences in risk, liquidity and purpose mean they will continue co-existing in a diversified portfolio.”

He explains —

Employees’ Provident Fund (EPF) offers fixed returns and is extremely secure. An increased NPS deduction might divert some voluntary savings, but it won’t replace the mandatory EPF structurePublic Provident Fund (PPF) is popular for its zero risk and fully tax-free status, especially among conservative savers. NPS, even with higher deductions, involves market risk and long lock-in, so many will continue to use PPF for safety.Insurance-linked savings products are often used by people for life cover and specific goals. Some may trim these in favour of NPS if it becomes more tax-efficient per rupee.Higher NPS vs. retirement gap

Tax analysts argue that higher upfront tax incentives can expand pension plan participation rates– particularly among voluntary savers, formal workers, and middle-income earners– but they must be part of a broader policy push to truly broaden retirement preparedness across India.

“Expanding NPS deductions can play a critical role in narrowing India’s retirement savings gap by nudging households toward disciplined, long-term pension accumulation while easing future fiscal pressure on social security systems,” said Sinha.

However, tax incentives alone aren’t enough.

“There are also coverage gaps that stem from lack of awareness, irregular incomes, and financial literacy issues, especially in rural or informal segments.

NPS tax perks help those already in the tax net more than those outside it. Without complementary policies– like auto-enrolment, portability improvements, incentives for employers in the private sector– higher limits mainly benefit formal workers,” said Dasgupta.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.