For investors in listed shares and equity mutual funds, life was simple before the Union Budget of 2018. They didn’t have to pay any tax, provided they stayed invested for at least the first year after investing. But the complexities have increased since February 1, 2018.

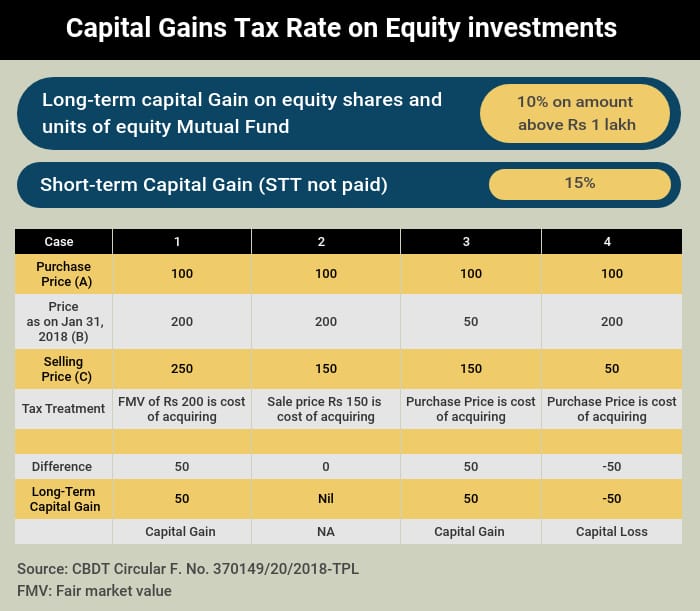

The Government announced a tax levy on gains above Rs 1 lakh from sale of equity shares of listed companies and equity oriented mutual funds held for more than one year too, in effect a long-term capital gains tax. As per the Union Budget of 2018, a long-term capital gains tax at the rate of 10 per cent would be applicable on any amount exceeding Rs 1 lakh per annum earned by way of selling equity investments – namely listed shares and equity-oriented mutual funds – after March 31, 2018.

Though the tax rate of 10 per cent applicable to long-term investments in equities is still lower than the 15 per cent applicable when you sell it within a year of purchase (short-term capital gains), indexation benefit or adjustment against inflation is not available on equities.

It is that time of the year when you need to reconcile all the financial accounts for the year to file your tax returns. If you have sold shares of companies or units of equity mutual funds, you need to understand the nitty gritty of this tax, especially as this is the first assessment year when you would be calculating the LTCG on equity investments.

To calculate the tax applicable on your gains, use the following Formula:

Capital Gain/Loss = (Price of selling the investment - expenses incurred) - Cost of acquisition or purchase.

The gain or loss is considered short-term if sold within a year of purchase and is taxed at 15 per cent.

If the investment is held for more than one year, the gain or loss is considered long term. And, long-term Capital Gains are taxed at 10 per cent if investments are sold on or after April 1, 2018

Expenses such as brokerage applicable on the sale can be deducted while calculating the gain or loss.

GrandfatheringUnderstand that the LTCG tax will be levied only upon transfer on or after April 1, 2018.

If the gains on your equity investment are long-term then you would need not just the purchase price and the sale price, but also the price as on January 31, 2018, which the day prior to Budget announcement, which is grandfathered.

Capital Gain/ Capital Loss = (Selling Price) – (Cost of Acquisition based on 31.1.2018 Fair Market Value)

“This price of various stocks as on January 31, 2018 is available with the stock-exchanges and even brokers and can be easily accessed, while calculating the tax liability,” says Mumbai-based chartered accountant Mehul Sheth.

Mutual Fund SIPs/SWPsWhile the grandfathering clause is one complex area, there is another hassle for mutual fund investors who have systematic investment plans (SIPs) and varying sale dates in terms of systematic withdrawal plans (SWPs).

“Each SIP instalment is considered a separate investment in itself. The units purchased in first SIP are considered and then based on the first-in-first-out method, the holding period is calculated based on the cost and the redemption date,” points out independent tax and investment expert Balwant Jain.

However, instead of racking your brains on calculating the SIP date and the price, there are services offered by registrars and transfer agents, and aggregators. So, a Realised Gain statement of the entire mutual fund portfolio that highlights the capital gains and income for the current and previous financial years across funds can be obtained from CAMS, Karvy Computershare or SBFS through their websites. There is a facility to even download a consolidated statement across all the service providers.

Commenting on the Mailback services for capital gains, Anuj Kumar, President & CEO-CAMS, said “LTCG statement was enhanced to present a single view of capital gain/loss of equity-oriented schemes across CAMS serviced funds. Investor requests for Capital gain /loss statement requests goes through a spike during the tax filing season and it begins as early as April of every year. We have seen over 2 lakh downloads of the LTCG and equity-grandfathered statements since April and the demand will continue into next couple of weeks. We have also sent over 13 lakh as push statements.”

The following path can be followed to get the report emailed to your mail account:

www.camsonline.com/ www.karvymfs.com > Investor Services > Mail back services > Realised Gains statement >

You need to fill essential details such as Financial Year for which report is needed, PAN, registered email address as reported to the fund house. You can set a password for your file as well. Next Select “Capital Gains” in “Income Sources.”

Similarly, if you wish to see the grandfathering statement of your mutual fund holdings, visit the websites of Computer Age Management Systems and Karvy Computershare to get a consolidated list.

Inherited sharesAnother question that arises is that what if the transfer of shares to a person is due to inheritance?

If the transfer of shares happens by way of inheritance, then one doesn’t bear the tax at the time of receiving the shares, clarify experts.

“Inheritance tax is not applicable in India. Hence, when you inherit the asset, in this case shares, there is no capital gains tax liability. But only when you sell the shares then the amount paid by the original holder – maybe your grandfather or descendants – is considered the acquisition cost. Though the grandfathered cost would save you the trouble of tracing the original cost, unless of course the original price paid is higher than the grandfathered cost,” Jain clarifies.

Computing capital loss, if anyWhat if your actual selling price was less than the grandfathered rate as on January 31, 2019? Would your investment be considered as capital loss?

Had Hiren sold the shares at Rs 4,500, he would have been able to claim a capital loss of Rs 50,000.

So, if you have actually made a capital gain loss on or after April 1, 2018, then the same can be adjusted against other Long-term Capital Gain and the balance long-term capital loss can be carried forward to subsequent eight years and set off.

Also, note that loss arising on transfer or sale of equity investments held for long-term between February 1, 2018 and March 31, 2018, will not be allowed to be set off or carried forward.

This isn’t the only misconception. There is another error that low-income taxpayers might make while calculating their tax liability. “A mistake that taxpayers often make is that they apply the Section 87A rebate of Rs 12,500 (earlier Rs 2,500) for those earning an income of up to Rs 5 lakh even to the long-term capital gain amount. But one needs to understand that the rebate of Section 87A will not be available for long-term capital gain on equity and equity mutual fund investment. So, even if you have the income below Rs 5 lakh and no other tax, you will have to bear the 10 per cent tax on the long-term capital gain exceeding Rs 1 lakh,” Jain reveals.

Therefore, consider all the scenarios and calculate the capital gains tax before you file your returns.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.