The draft Income-tax Rules, 2026, propose a simplified and more transparent framework for taxing employee perquisites. Provisions that were earlier spread across multiple rules have now been consolidated into a structured, table-based format, intending to make the valuation rules easier to understand.

"The draft rules also update several long-standing monetary limits for common perquisites. The valuation of perquisites, which was earlier governed by Rule 3 of the Income-tax Rules, 1962, is now proposed to be comprehensively covered under Rule 15 of the Income-tax Rules, 2026," said CA (Dr.) Suresh Surana.

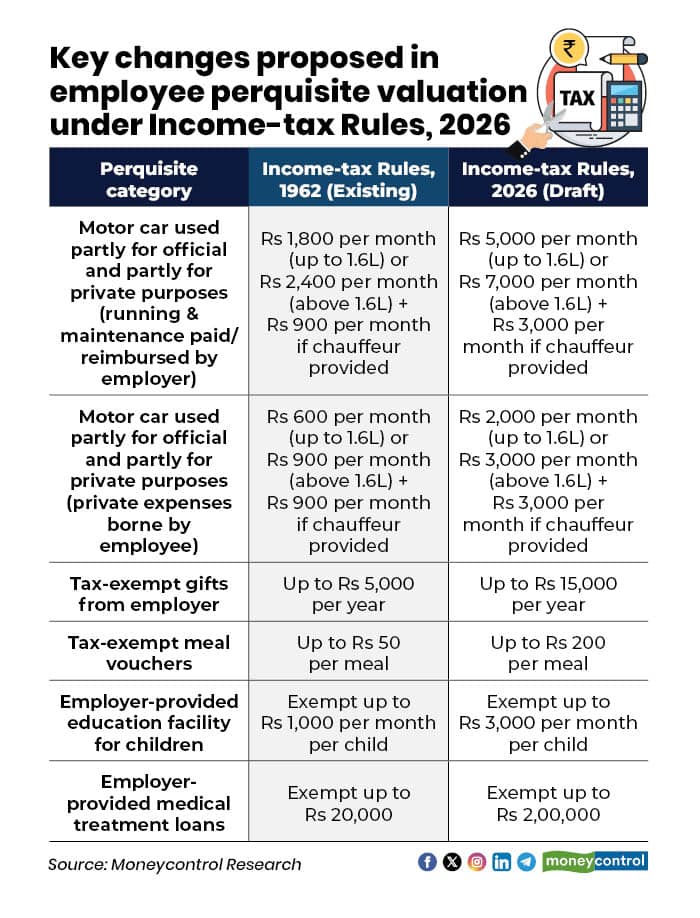

Key changes proposed under the draft rules include the following

Valuation of motor car perquisite

Under Rule 15 of the Income-tax Rules, 2026 (Draft), when a car is used partly for official and partly for private purposes and the running and maintenance costs are paid or reimbursed by the employer, the taxable value is proposed at Rs 5,000 per month for cars with engine capacity up to 1.6 litres and Rs 7,000 per month for cars above 1.6 litres. An additional Rs 3,000 per month will be added if a chauffeur is also provided. In comparison, under Rule 3 of the Income-tax Rules, 1962, the value was much lower at Rs 1,800 per month (up to 1.6 litres) or Rs 2,400 per month (above 1.6 litres), with a further Rs 900 per month if a chauffeur was provided.

Where a car is used partly for official and partly for private purposes but the private running and maintenance expenses are fully met by the employee, the draft 2026 rules propose a taxable value of Rs 2,000 per month for cars up to 1.6 litres and Rs 3,000 per month for cars above 1.6 litres. If the employer provides a chauffeur, an extra Rs 3,000 per month will be added. Under the existing 1962 rules, the corresponding values were Rs 600 per month (up to 1.6 litres) or Rs 900 per month (above 1.6 litres), plus Rs 900 per month if a chauffeur was provided by the employer.

Enhancement of tax-exempt limit for employer-provided gifts

As per Rule 15(5)(a) TABLE IV of the Income Tax Rules, 2026 [corresponding to Rule 3(7)(iv) of the Income Tax Rules, 1962], the annual tax exemption for gifts provided by employers to employees has been increased from Rs 5,000 to Rs 15,000, thereby allowing greater flexibility and higher tax-efficient non-cash benefits for employees.

Proposed increase in tax-exempt limit for employer-provided meal vouchers

As per Rule 3(7)(iii) of the Income Tax Rules, 1962, free meals provided by an employer through paid vouchers, which are non-transferable and redeemable only at eating joints, are exempt from tax, subject to a monetary cap of Rs 50 per meal. "Rule 15(5)(a) TABLE IV of the draft Income-tax Rules, 2026 propose a significant relaxation of this limit. As per the draft, the exemption threshold for such meal vouchers has been enhanced to Rs 200 per meal, provided all other prescribed conditions continue to be satisfied," said Surana.

Enhanced perquisite exemption threshold for employer-provided education facilities

As per Rule 3(5) of the Income Tax Rules, 1962, free or concessional education provided by an employer to an employee’s children was treated as a taxable perquisite, with an exemption limited to Rs 1,000 per month per child, applicable only where the education was provided in an institution owned or maintained by the employer. However, as per Rule 15(4) TABLE III of the Income Tax rules, 2026, this monetary threshold has been enhanced to Rs 3,000 per month per child, with amounts exceeding the revised limit continuing to be taxable as perquisites.

Increase in the perquisite tax exemption threshold for employer-provided medical treatment loans

As per Rule 3(7)(i) of the Income Tax Rules, 1962, interest-free or concessional loans granted by an employer for medical treatment were treated as taxable perquisites, except where the aggregate loan amount did not exceed Rs 20,000 or where the loan was provided for treatment of specified diseases in approved hospitals. "As per Rule 15(5)(a) TABLE IV of the Income Tax Rules, 2026, the exemption has been significantly expanded, and employer-provided medical treatment loans up to Rs 2,00,000 are not treated as taxable perquisites, with only the excess amount, if any, being subject to perquisite taxation," said Surana.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.