Many of us have grieved for someone we lost due to cancer. While such a health emergency comes as an acid test in one’s life, the treatment cost for cancer can quickly drain the household’s life savings.

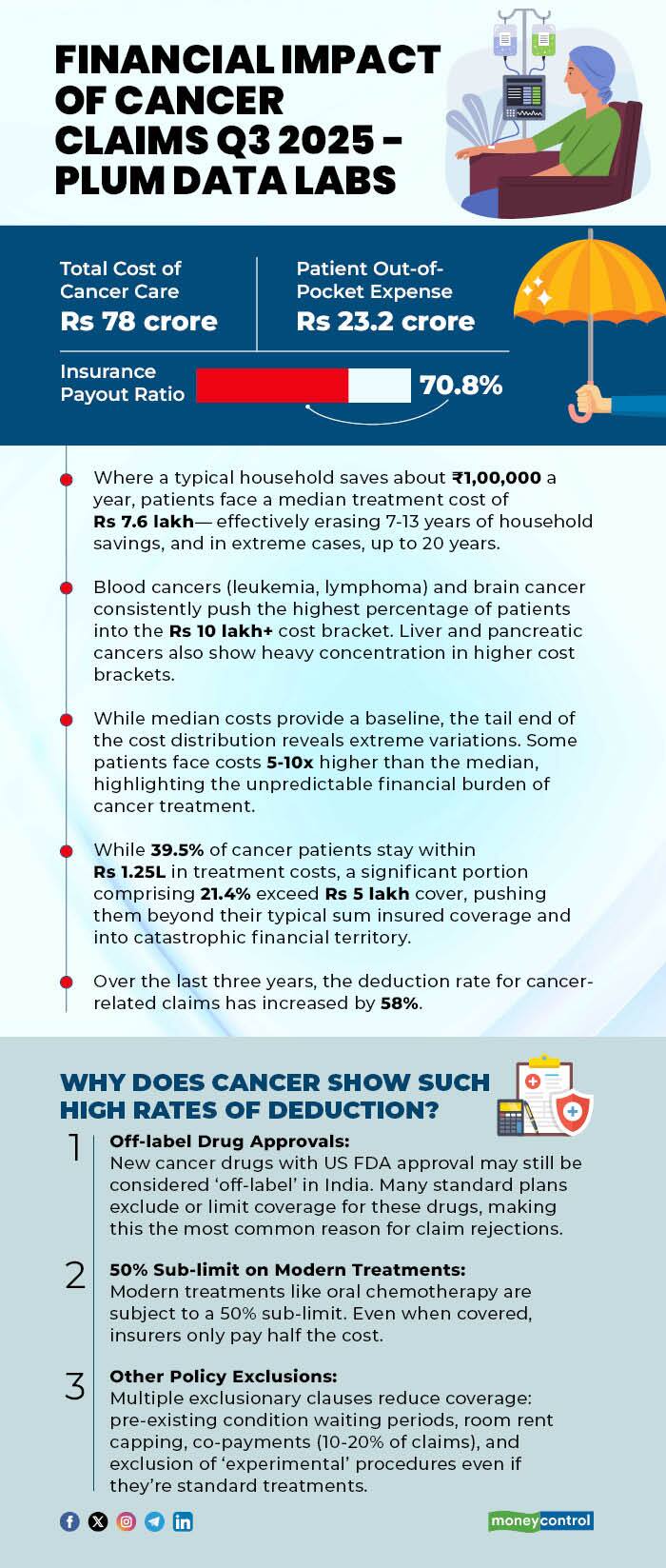

A new report by Plum’s Data Labs, an insurtech startup based in Bengaluru, which studied the last three years' data comprising 8,102 insurance claims till Q3 2025, reveals that the total cost of cancer arising out of these claims has reached Rs 78 crore, where patients' out-of-pocket cost was Rs 23.2 crore, while the insurance payout ratio stood at 70.8 percent.

The data showed that the minimum cost for the treatment of liver cancer patients was Rs 74,600 and can go up to Rs 23.06 lakh. For Leukemia, the cost ranges from Rs 1.65 lakh to Rs 40.56 lakh, Rs 3.43 lakh to 43.68 lakh for brain cancer, and up to Rs 16.16 lakh for ovarian cancer, to cite an example.

The case study of a 30-year-old female showed that she paid Rs 6.31 lakh for her nine-month treatment for early-stage carcinoma in situ. She had three hospitalisations that cost 0.99 lakh, nine chemotherapy cycles of Rs 4.76 lakh, and six pre-post consultations and tests that cost Rs 0.56 lakh.

Another 39-year-old female paid Rs 43.68 lakh for the treatment of breast cancer that lasted for 28.4 months. This included four hospitalisations, 20 chemotherapy cycles, and 10 pre-post consultations. For the first 1-2 months, the initial diagnosis started. The 3-23 months were followed by chemotherapy and monitoring. Her treatment was completed in the 28th month.

How deductions necessitate out-of-pocket costs for cancer-insured patients

The Plum’s Data Labs report further revealed that 1 out of 4.7 patients exceed the Rs 5 lakh insurance limit, and 39.5 percent of cancer patients stay within Rs 1.25 lakh limit. A significant portion, comprising 21.4 percent, exceeds the limit of the Rs 5 lakh cover.

What’s worrying the team is that the deduction rate for cancer-related insurance claims has increased by 58 percent in the last three years, as of Q32025.

Insurers often apply proportional deductions when hospital charges exceed limits mentioned in the policy, such as room-rent eligibility and non-medical expenses. The policy wording highlights all these items for which coverage is not available.

“Our studies have also identified that insurers have, at times, denied the cost of certain cancer treatments, which may have used off-label drugs, or it could be that the US FDA has approved the treatment, but not in India. So, deduction is applied for those kinds of drugs and treatments where patients or their family bear the whole amount themselves,” explains Sauroab Arora, co-founder and CTO of Plum, a Bengaluru-based insurtech startup.

So higher the deduction, lower the payout ratio, leaving patients with a higher financial burden, which often leads the family to bear significant out-of-pocket expenses. Arora reasons that it is also extremely hard for insurers to catch up with the advanced drugs and research that are happening simultaneously.

In a health policy, a deductible is not to be misunderstood with co-payment, a cost-sharing agreement where the insured pays a certain percentage of the claim amount, and the remaining is paid by the insurer.

Sub-limit, on the other hand, is a predefined maximum cap on amounts for specific treatments, beyond which the insurer will not pay. There are also exclusions that apply to a particular condition related to cancer of specified severity that the policy explicitly does not cover.

Most comprehensive health plans, particularly cancer-specific plans, have a ‘survival period’ on critical illnesses, requiring patients to survive for a set number of days before the insurers begin to pay for the treatment.

Cancer-specific insurance policies

Unlike comprehensive health plans, which cover cancer treatment as one of the critical illnesses, insurers also provide cancer-specific policies. These are plans that are specifically designed for the treatment of cancer.

The Insurance Regulatory and Development Authority of India's (IRDAI) Guidelines on Standardisation and Coverage of Modern Treatment Methods 2019, consolidated in the Master Circular on Health Insurance Business, 2024, mandate the coverage for 12 modern cancer treatments, including oral chemotherapy, immunotherapy, robotic surgeries, and stem cell therapy— and require clear disclosure of sub-limits and exclusions. We evaluated features of five cancer-specific polices provided by various insurers. Its features are as follows:

| Sum Insured | Rs 10–50 lakh |

| Entry Age | 1–85 years (varies as per plan) |

| Stages of Cancer | Pre-cancerous, early stage of carcinoma, minor and major stages (vary as per plan) |

| Waiting Period | 180 days (standard) |

| Survival Period | 7 days (standard) |

| Premium Modes | Monthly, quarterly, half-yearly, and annually (varies as per plan) |

| Exclusions | All tumours described as carcinoma in situ, benign, pre-malignant, borderline malignant, low malignant potential, neoplasm of unknown behavior, or non-invasive, including but not limited to: carcinoma in situ of breasts, cervical dysplasia CIN-1, CIN-2 and CIN-3; any non-melanoma skin carcinoma; malignant melanoma not beyond the epidermis; all tumors of the prostate; all thyroid cancers; chronic lymphocytic leukaemia less than RAI stage 3; non-invasive papillary cancer of the bladder; all gastro-intestinal stromal tumors; all tumors in the presence of HIV infection. |

Payout ratios for cancer treatment

Plum’s data reveals a troubling pattern wherein insurance payouts are shrinking, and patients are paying the price. The report highlighted that the insurance payout ratio stood at 70.8 percent from 8,102 insurance claims till Q3 2025.

“In just three years, the average payout ratio is down to 70.8 percent, meaning nearly a third of every hospital bill is still paid out-of-pocket. For instance, a patient with brain cancer, even with a Rs 10 lakh policy, may end up paying Rs 4-5 lakh themselves due to exclusions on modern drugs and treatment sub-limits. The median cost of advanced cancer treatment is Rs 7.6 lakh, erasing 7-13 years of an average Indian household’s savings,” said Arora.

He questions, “There is IRDAI, there are insurers, there are hospitals, and members. So, can IRDAI come and try to influence what should be the payout ratios?” adding that “We also want to push insurers to eliminate sub-limits on the first line of cancer treatments.”

How transparent, predictable cancer coverage rules improve insurance payouts

Sunayana Basu Mallik, Partner at King Stubb & Kasiva Advocates and Attorneys, says that insurers manage cancer treatment costs through waiting periods, sub-limits on therapies, co-payment clauses, and exclusions for treatments categorised as ‘experimental’.

“These contractual mechanisms often result in deductions even when the treatment is medically necessary, particularly in the case of newer oncology therapies,” said Malik, adding that IRDAI can improve effective payout ratios for cancer care treatment by ensuring that deductions are predictable, transparent, and not arbitrarily applied.

Another step the IRDAI can take is to standardise cancer care riders that categorise coverage by treatment class rather than individual drug names, says the analyst.

“This will ensure that necessary therapies are not excluded merely because they are new. Riders should include defined limits, permissible co-payments, and lifetime caps, along with a clear list of exclusions backed by objective medical or regulatory criteria. This approach would give policyholders clarity at the time of purchase and reduce disputes at the claims stage, while still allowing insurers to price risk appropriately,” said Malik.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.