In the midst of global corporate earnings, International Monetary Fund’s update on global economic health and Federal Reserve’s reassertion on interest rate trajectory, trade war risks is suddenly taking centre stage. While the Fed’s interest rate path remains firm with two more rate hikes pencilled in this year, risks emerging from the US President Donald Trump’s brinkmanship cannot be wished away and can potentially derail the economic goldilocks of high growth and low inflation. While we assign low probability for a full blown trade war, impact on growth and capital inflows due to the length of uncertainty caused by the trade tariff tensions implies higher equity risk premium.

Yet another strong affirmation on growthThe Federal Reserve’s Beige Book report, which is published eight times a year, provides continuum of qualitative assessment of economic conditions in the US. The key message from the July report provides sustenance of positive economic momentum with the majority of Federal Reserve districts expressing moderate growth. The key outlier in the last few reports has been the Dallas District (Texas), which reported strong growth, driven by the energy sector.

On the growth front, the above anecdotal observations were backed by similar but data driven assertion from Fed Chair Jerome Powell. In its semi-annual monetary policy report to the Congress, he submitted that robust labour market, higher after-tax incomes and rising consumer confidence have led to firming up of the domestic economic scenario. Additionally, business investment have grown at a robust rate. Part of this is also reflected in consensus expectation of 4 percent year-on-year (YoY) growth in US GDP in Q2 CY18. The macroeconomic backdrop outside the US has also been supportive of US exports and manufacturing growth.

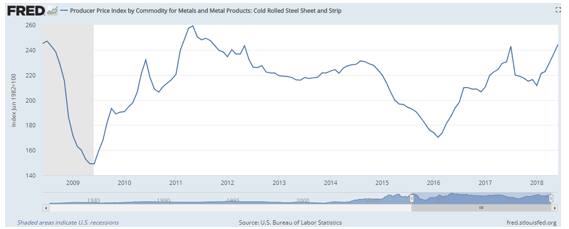

Inflation and labour shortage concerns at the peripheryIn its May Beige book report, the Fed highlighted that input cost increases, labour shortages in some sectors and improving demand have led to higher prices in transportation, construction and manufacturing sectors. In the current report, higher tariffs have emerged as a new factor contributing to price increases for key inputs like fuel, construction materials, freight and metals.

Galloping metal price inflation

The July report suggest that shortage of a skilled labour force has widened across occupations like high tech engineers, specialised construction and manufacturing workers, IT professionals and truck drivers. However, except for a couple of districts, the wage increase has been modest.

Perhaps not alarming yet, but on the margin, higher metal and tariff-led inflation and labour shortage have caught our attention.

The IMF in its recent World Economic Outlook signals a firmer inflation path in the United States that could lead to a shift in market expectations of interest rate hikes, which is currently below its prediction. A further appreciation in the dollar in that case can weigh on the carry trade flows to emerging markets. Already $14 billion have left emerging markets in the last couple of months.

Trade war inching up as is downside risk The key takeaway from the Beige book report is heightened concerns about price increases due to supply disruptions and tightness in the labour market. Minutes of the last Fed meeting highlight this upfront and many Fed participants have cited that developments related to trade policy are posing downside risks to their growth forecasts. Many Federal Reserve Districts indicate that plans for capital spending had been scaled back or postponed as a result of uncertainty over the trade policy.

In his testimony to the senate, Fed chair cited difficult in predicting the ultimate outcome of current discussions over trade policy. He stated that countries that have remained open to trade have grown faster and had higher productivity.

Lengthier the trade war, murkier could be the growth outlook Even if one expects Trump to succeed, prolonging of political manoeuvres, could make the global supply chain more susceptible to disruption. Investment decisions are shifting and some of those could be detrimental to American interest. For instance, chemical major BASF, which was earlier considering its biggest investment to date ($10 billion) in the US to tap feedstock from shale gas decided to opt for China to be closer to the consumption market.

Earnings of commodities players are getting impacted despite higher realisations. Major US aluminium company Alcoa has trimmed its earnings guidance on account of higher tariffs in its Q2 CY18 result.

Nevertheless, a global trade policy threat has emerged as a major downside risk. IMF in its recent publication suggest that if current trade policy threats are realised and business confidence falls as a result, global output could be about 0.5 percent below current projections by 2020. IMF expects such a huge moderation of growth trajectory would have second order effects on deterioration of risk appetite and capital flow reversal.

Overall, the current state of affairs implies higher risk premium is needed to be assigned not just due to the yield curve but also due to current politico-economic uncertainty.

Follow @anubhavsaysFor more research articles, visit our Moneycontrol Research pageDiscover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.