Highlights

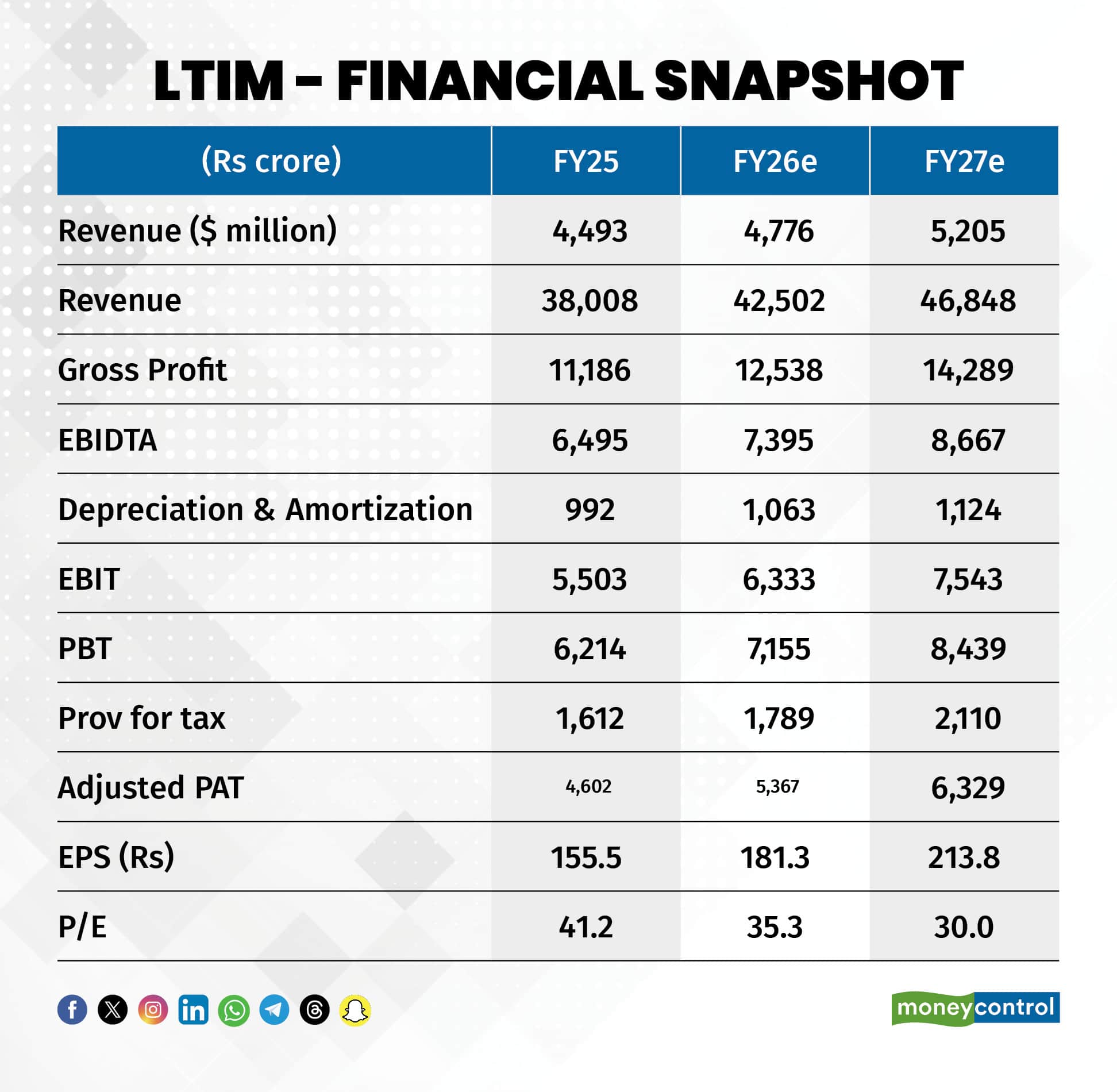

LTIMindtree (LTIM, CMP: Rs 6407, Market Cap: Rs 189,960 crore, Rating: Overweight) reported a good Q3 FY26 with a strong sequential surge in revenue despite the seasonality, uptick in margin, and steady deal flow. The management remains optimistic about clocking close to double-digit YoY growth in revenue in Q4 and maintaining the momentum in FY27. The stock has been an out-performer in the IT pack and has performed in line with the Nifty in the past year. While the headline valuation isn’t cheap, the growth journey makes us constructive.

Strong surge in revenue

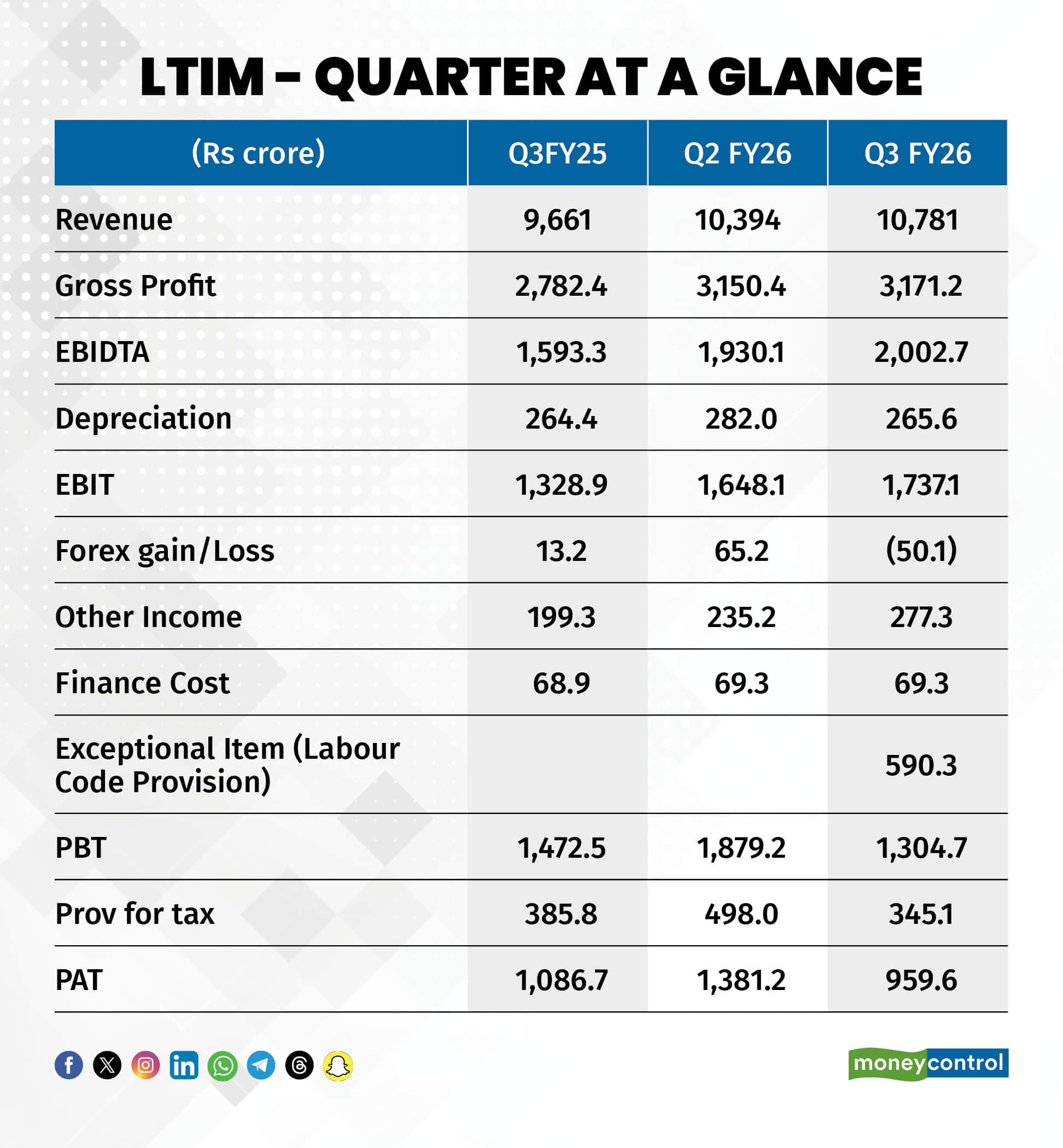

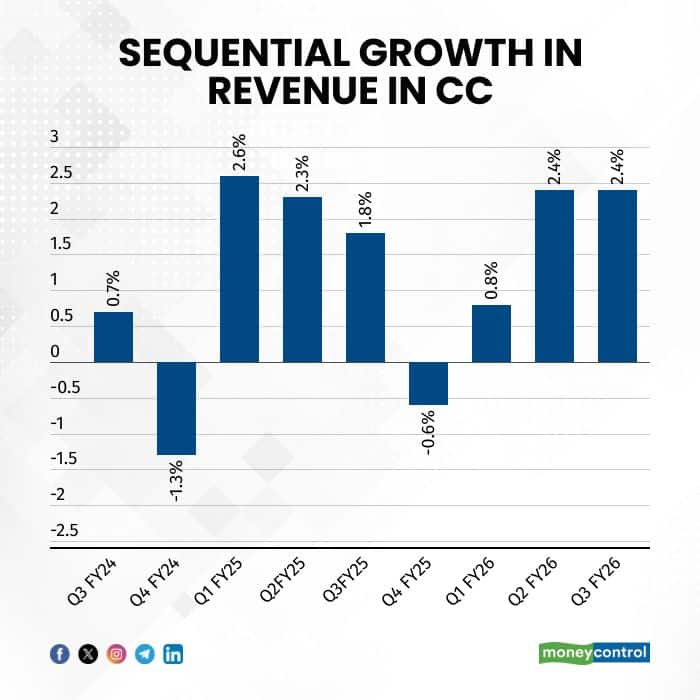

Revenue for the last reported quarter Q3 FY26 at $1208 million represented a sequential growth of 2.4 percent in reported currency and in Constant Currency (CC).

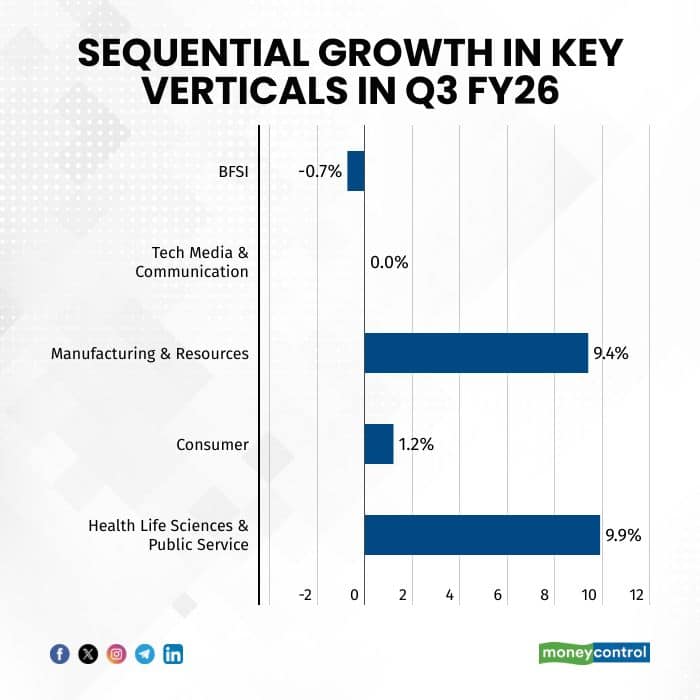

The reporting quarter (Q3FY26) saw strong performance from Healthcare, Life Sciences & Public Services, followed by Manufacturing & Resources. The Consumer business had a positive sequential growth. Weakness was seen in BFSI (banking financial service and insurance) and Technology, Media & Communication because of a combination of furloughs and productivity passthrough in some top accounts. All the three key markets of North America, Europe, and the Rest of the World (RoW) had a positive sequential growth. The PAN deal from India had a positive rub-off on RoW.

Weakness in top accounts transitory

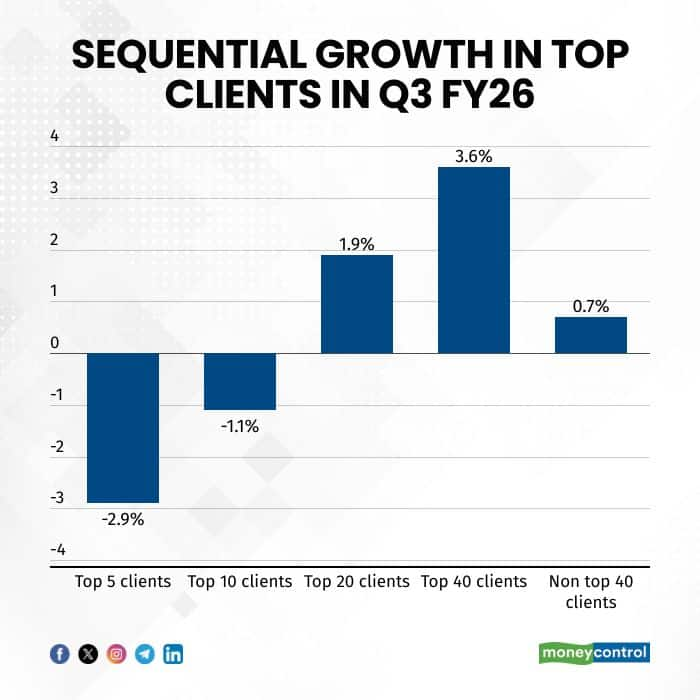

Unlike the strength in the overall business, the top 5 accounts (which include the top hitech and BFSI account) de-grew YoY 8.7 percent and a sequential 2.9 percent in Q3 FY26. The temporary impact has been on account of recalibration as LTIM has passed on AI-driven productivity gains to customers. The top hi-tech account has started growing sequentially and the BFSI segment and the top account is likely to bottom out in Q4. The impact of the AI-led productivity gains is more meaningful in large engagements and the management expects growth momentum from these large accounts to resume from FY27.

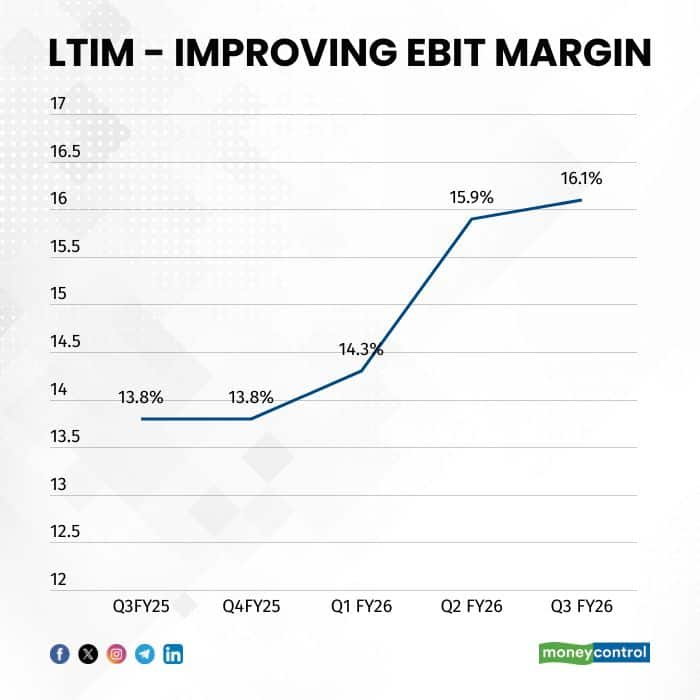

Guiding to margin stability

LTIM’s EBIT margin expanded 20 basis points QoQ in Q3 FY26 to 16.1 percent. Tailwinds from the Fit-for-Future efficiency gains programme and forex were partially offset by furloughs and lower working days. The management remains confident of sustaining margin improvement supported by levers, including AI-driven productivity gains, pyramid optimisation through fresher hiring, and continued cost discipline. It has started a new programme called New Horizon for steady focus on cost and margin. The likely wage hike in Q4 to be spread over two quarters is likely to cause 1 percent margin headwind each quarter.

LTIM reported a net headcount addition of 1,511 employees in Q3FY26, including 1736 freshers, taking the total workforce to 87,958. This further bolsters confidence on future execution.

Gaining the AI edge

The key initiatives from LTIM are launching "Blueverse Studios" in Mumbai and London as AI collaboration hubs for clients. The company has completed the GenAI Foundation training programme for 80,000 employees and has won multiple AI-specific deals, including developing agentic solutions and GenAI-based platforms for global clients.

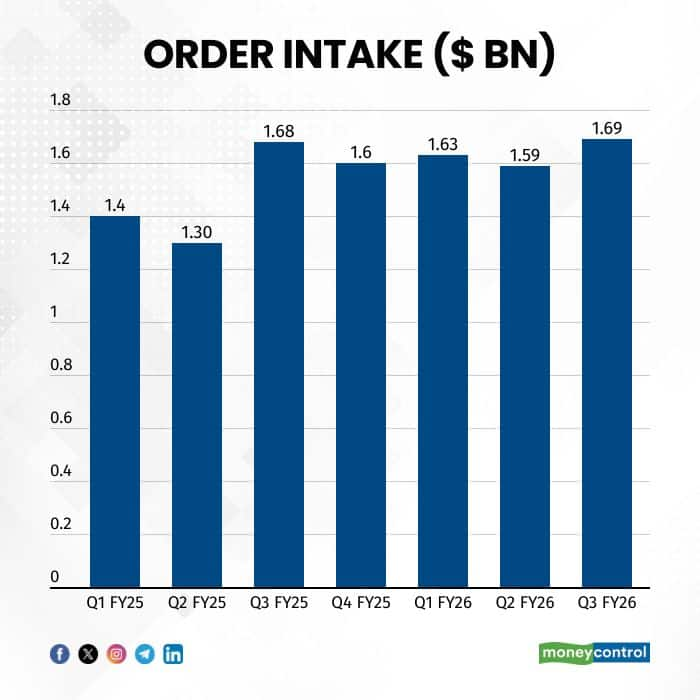

Bookings steady

The Q3FY26 order book TCV (total contract value) stood at $1.69 billion, flat YoY but up by over 6 percent sequentially. This marks the fifth consecutive quarter with TCV above $ 1.5 billion.

The management remains optimistic about achieving close to double-digit USD revenue growth in Q4 and maintaining the momentum, supported by robust deal wins, strong execution, continued operational efficiencies and opportunities arising from AI. Thanks to the outperformance, the stock isn’t cheap, but the growth trajectory warrants attention of long-term investors.

Key risks: Severe macro challenges impacting technology budgets and AI-led disruptions

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.