Rising mercury levels are helping cash registers at air conditioner and air cooler companies jingle. Symphony, by virtue of its numerous tailwinds, is well-positioned to reap the benefits. The company is one of India’s leading air cooler brands, catering to residential and industrial clients across the country. The former constitutes nearly 90 percent of the company’s annual sales. It derives 80-85 percent of its turnover from domestic markets.

Symphony’s robust financials, backed by emphasis on core competencies and multi-year growth visibility, make it a worthy inclusion in the list of reliable performers. The company has managed to prove its mettle in the highly competitive consumer durable industry.

Why Symphony?Market share Symphony commands a 50/42 percent market share in India’s organised air cooler segment in value/volume terms, respectively. Its products enjoy a strong brand recall. Even in seasonally weak quarters, its products witnessed strong traction.

GST transition India’s air cooling industry is predominantly driven by unorganised players, that constitute roughly 65/73 percent in value/volume terms, respectively. Post implementation of the Goods & Services Tax (GST), organised companies such as Symphony are likely to gain market share as product pricing differences between the two reduce further.

Rate benefits The effective tax rate for air coolers that stood at 21-22 percent in the pre-GST phase is 18 percent post-GST. These tax savings should translate into better margins. Introduction of the e-way bill and regularisation of trade channels would simplify logistical issues as well.

Consumer tailwinds The rising demand for cooling products is driven by cheaper financing options and increasing electricity coverage, among others. The trend seems unlikely to change, thus putting consumer durable majors in a sweet spot.

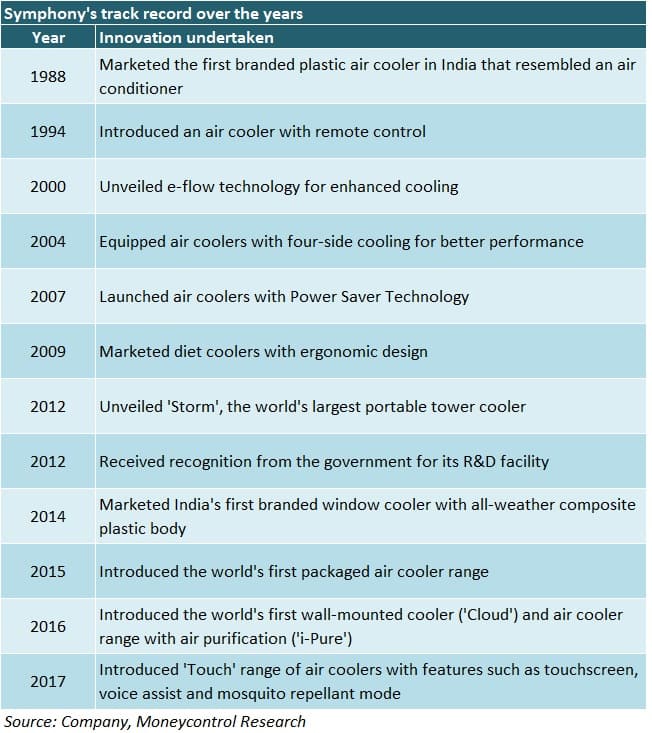

Innovation Symphony’s focus on its core strength is apparent from the series of launches undertaken by it over the years across categories such as portable, window and centralised air cooling. To tackle the stiff competition, especially from AC manufacturers, the company’s offerings are upgraded every two seasons.

Branded product portfolio Symphony’s air cooler offerings span 45/15/20 models for residential/commercial/international customers, respectively. Its key brands include Cloud, Diamond, Silver, Touch and Sense. The former three, in particular, registered healthy growth in domestic markets of late.

Low penetration Vis-à-vis (ceiling/tower) fans, the penetration of air coolers and ACs is low in India. With rising disposable incomes and households moving up the value chain by choosing premium cooling products, there exists potential for a pick-up in demand in underserved geographies.

Soaring temperatures For most part of the year, climatic conditions in India remain warm. Average temperatures appear to be rising with each passing year on account of global warming. This necessitates the use of cooling appliances on a regular basis, making purchase of an air cooler less of a discretionary spend.

Capital-light model Symphony outsources its manufacturing to third-parties. The management distributes its products to most retailers against advances only and is able to keep dealer margins low because of its pricing power. With negligible debt on its books, its return ratios continue to remain healthy. This trend is expected to continue going forward.

Distribution boost In a bid to increase its rural outreach and widen distribution, the company intends to add 10,000 dealers to its existing 30,000-strong network over the next two years. By virtue of this move, the management aims to strengthen its numero uno status in the market and boost revenue growth.

Shift to branded products Traditional air coolers are predominantly commoditised due to their limited features and low aesthetic appeal. They have now been outpaced by superior-quality branded variants over the years. Being a pioneer in this space, Symphony is well-poised to capture a lion’s share of the market given its brand recall.

Low maintenance costs For price-sensitive or cost-conscious buyers, more often than not, air coolers are the first preference after fans. This is because initial purchase and subsequent running costs are lower in case of air coolers as compared to ACs.

Inorganic growth To reduce the impact of seasonality in Indian markets, Symphony acquired Mexico-based IMPCO in 2009 and China-based Munters Keruilai (MK) in 2015. The objective was to leverage IMPCO’s tie-ups with large format stores in America and MK’s patented technology in premium commercial air cooling.

The roadblocksSymphony’s international segment continues to lag its domestic business. Of late, demand for air coolers in Europe and South America has been sluggish. Prevalence of an adverse geopolitical scenario in West Asia is another cause of concern. IMPCO and Keruilai, Symphony’s two subsidiaries, are yet to make their presence felt in the company’s consolidated financials. While working capital challenges and high interest costs are a drag for IMPCO, Keruilai has not been able to achieve breakeven yet.

Even though the transaction size in industrial cooling is high, margins generally tend to be lower than residential air coolers. This is attributable to the business-to-business (B2B) nature of the contract, where the pricing power of Symphony is limited.

Managing after-sales services, on similar lines as other consumer durable companies, is a big hurdle in itself. Raw material prices (plastic, copper and aluminium) have been firming up of late. This could be margin diminutive, especially in connection with low to moderate priced air coolers, where competition is stiff.

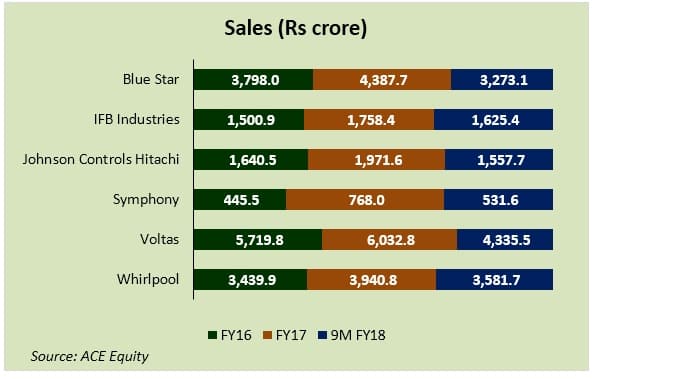

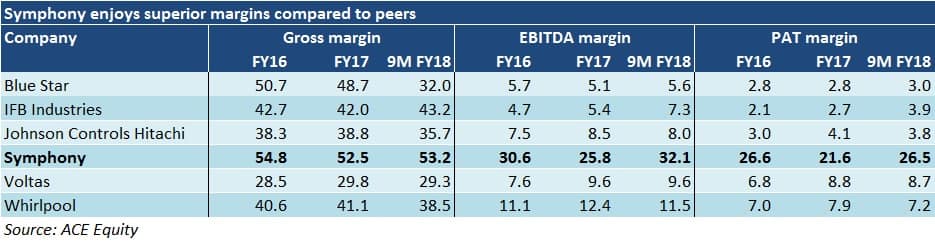

Peer comparison: An overviewDespite Symphony’s topline being much smaller than its peers, it surpasses on the margin front.

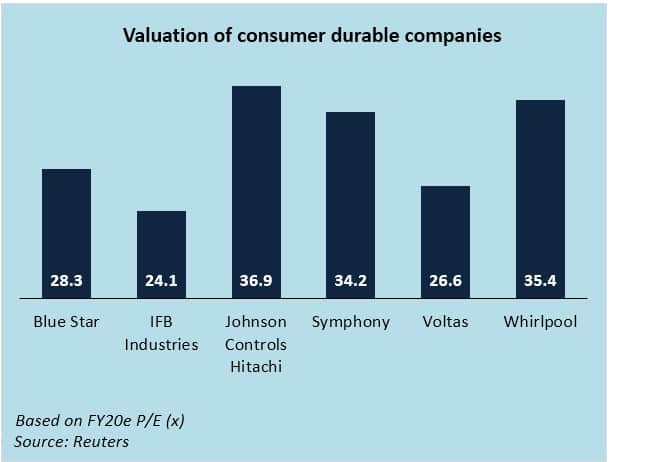

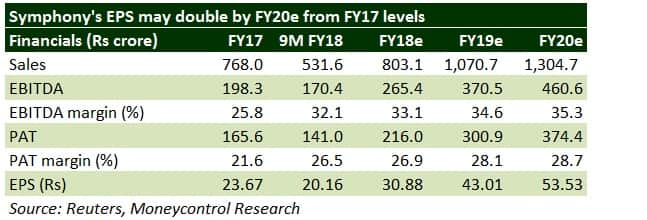

The recent rally clearly reflects in the company’s steep valuation (34.2 times FY20e earnings). Since the investment moats are fully discounted at current levels, there is no valuation headroom. So, going long on downsides is advisable.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.