Neha Dave Moneycontrol Research

HDFC's, the largest housing finance company in India, Q4 FY18 earnings were ahead of consensus estimates aided by lower tax rate and one-time gains from the sale of its subsidiaries. The broad numbers for FY18 are consistent. Loan growth remains strong, margins are stable and asset quality pristine.

The management’s consistency is worth highlighting. It posted robust profits from 1980 to 2017 at a compounded annual growth rate (CAGR) of 30 percent. This momentum continued in FY18 as well. In fact, HDFC’s return on equity (RoE) was greater than 15 percent for every single year starting 1998 to 2018, except for 2009, where it missed the same by a fraction due to fund raising in 2008. Given such a superior profitability performance, the stock has grown 58 times in the past 20 years, generating 23 percent CAGR.

We believe there is more to follow from HDFC. While its core mortgage business is on a stable growth trajectory, the financial conglomerate stands to gain from equally strong performance of its subsidiaries. Investors cannot ignore this financial powerhouse.

Earnings snapshot

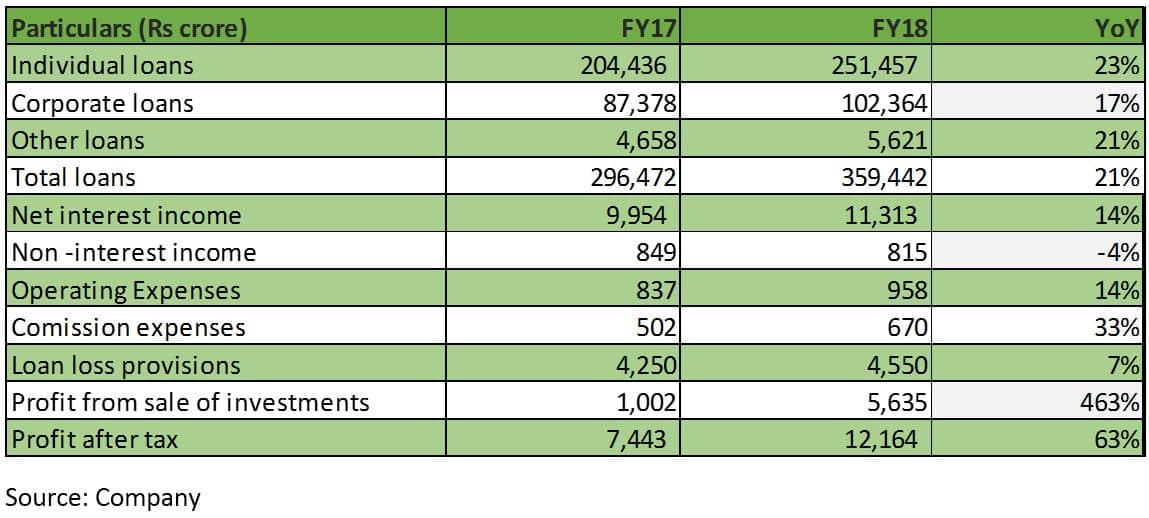

HDFC reported a profit before tax of Rs 15,264 crore, up 42 percent year-on-year (YoY). After adjusting for exceptional items and one-time transactions (i.e. profit on sale of subsidiaries and consequent special additional provisions), FY18 PBT would have been Rs 11,397 crore as compared to Rs 10,082 crore in the previous year, a growth of 13 percent.

Robust loan growth

The company’s core lending book stood at Rs 359,442 crore as at the end of March 2018, growing 21 percent YoY. Individual loan book grew 18 percent YoY and now constitutes 73 percent of the total. Growth in the individual loan book would be 26 percent if we add back loans sold in the preceding 12 months on which HDFC earns 1.27 percent per annum. Non–individual book increased 17 percent, aided by traction in lease rental discounting and construction finance.

Break up of the loan book

HDFC stands to benefit from the structural growth drivers in the sector (GDP growth, under penetration in the mortgage segment, etc) as well as government initiatives (interest subvention scheme, tax incentives, housing for all by 2022, infrastructure status accorded to affordable housing). Despite its size, loan book growth looks sustainable.

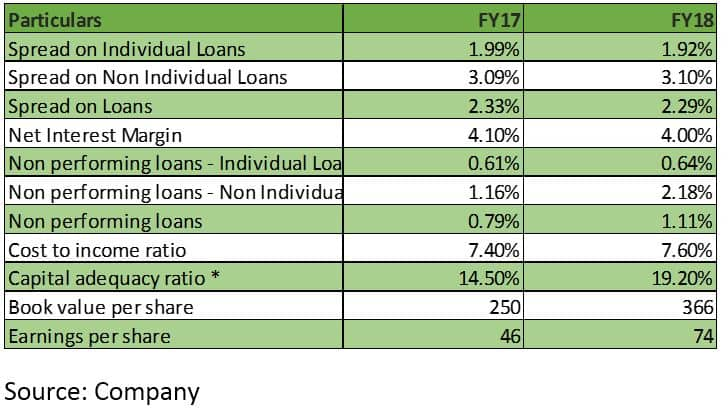

Stable margins

Spreads on the overall book remained almost stable at 2.29 percent (individual book: 1.92 percent and non-individual book: 3.1 percent) indicating HDFC’s ability to maintain spreads across interest rate cycle and amid rising competition.

Impeccable asset quality

With gross non-performing loans at 1.11 percent, asset quality continues to be pristine. Also, the management’s policy of creating 30 percent provisions from one-off gains has resulted in total provisions at 1.39 percent of loan book, which is in excess of the regulatory requirement.

Improving performance of its subsidiaries

HDFC’s superior performance is just not restricted to its mortgage business. Its subsidiaries have an equally blazing track record (HDFC Bank, Gruh Finance, HDFC Standard Life and HDFC Asset Management Company). Subsidiaries and associate companies contributed 33 percent to FY18’s consolidated profit. With increasing scale and profitability of subsidiaries, more than 45 percent of its value is now derived from subsidiaries.

A well-capitalised franchise

HDFC is well capitalised post its fund raising of Rs 13,000 crore and expected warrant conversion. It intends to utilise Rs 8,500 crore to maintain its stake in HDFC Bank (which too is raising capital in view of its promising growth outlook) and the rest for inorganic growth. The impending initial public offering of HDFC AMC will result in additional capital gains.

Compelling valuations

HDFC should be able to maintain its core return on assets (RoA) of over 1.8 percent and core RoE of over 17 percent aided by strong loan growth, steady margins, stable asset quality and low cost to income ratio of around 7-8 percent. With considerable value being created by subsidiaries, its core lending business is currently valued at 2.3 times FY20e forward price-to-book ratio, which is a meaningful discount to its historical average.

Core earnings growth in mid-teens is lower compared to many smaller housing finance companies (HFCs). However, HDFC’s ability to deliver consistent performance across rates and growth cycles, in spite of its large size and high competition, should help it command premium valuations to its peers. It is a rarity to find a quality financial services business (not just a housing finance play) at reasonable valuations. Investors should utilise this opportunity to buy into the stock.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.