Amid the flurry of activities that Indian retail has been witnessing in the last few years, the Kishore Biyani-led Future Group has been at the forefront.

While Future Retail entered into a deal with Shoppers Stop to acquire Hypercity, Future Lifestyle Fashions has been considering a stake sale of 10 percent to Flipkart (as per an Economic Times report). Future Supply Chain Solutions too got listed on the bourses.

Furthermore, Biyani announced an ambitious target of achieving a USD 1 trillion turnover by FY47 through a ‘Retail 3.0’ (Tathastu) strategy as well. To consolidate its strengths, a recent Press Trust of India update suggests that the conglomerate is in talks to buy Vulcan Express, Snapdeal’s largest distribution arm, for approximately Rs 50 crore in an all-cash transaction.

In the wake of these announcements, what can a prospective investor look forward to in Future Retail (the flagship brand of Future Group)?

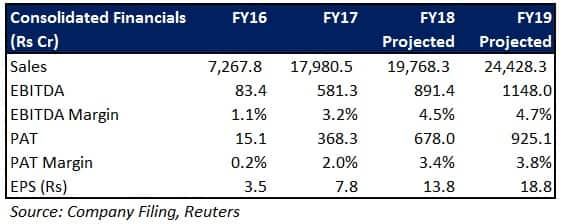

Future Retail - An Overview

The goal is to open an Easyday outlet (with a maximum number of 2,000/3,500 members/SKUs per outlet, respectively) in every two kilometres of the company’s core markets across India.

Besides ensuring timely availability of the company’s products (food, home accessories, FMCG, garments) to the masses through discounts/schemes/privileges, the plan aims at blending the benefits of online and offline retailing, too

Simultaneously, emphasis will be laid on deriving synergistic advantages by virtue of logistical cost savings (through cluster-based expansion in densely populated Indian cities/towns) and tackling competition from e-commerce portals, which, in turn, may result in a margin uptick.

Convenience stores have immense potential to generate operating leverage owing to a high asset turnover rate. This can be attributed to emergence of low cost model (for sourcing, storage, and supply efficiencies), increase in frequency of food purchases, and unwillingness on the consumers’ part to travel long distances to buy basic necessities.

Business integration through Hypercity takeoverThe deal will give Future Retail access to nearly 20 million incremental footfalls and stores with premium positioning. Should Future Retail succeed in making Hypercity’s loss-making operations profitable (from FY19, in all likelihood), the combined synergy will not only reduce its overheads and promotion spends (since Hypercity properties will be functional almost immediately with minimal or no capex required at the outset), but also facilitate economies of scale (because of similarities in business between the two).Robust store visibility pan-IndiaFuture Retail’s outlets are geographically diversified across the country.

Additionally, the company is anticipated to target a higher percentage of overall revenue from branded garments (more specifically from private label ones) as against the comparatively low-margin grocery products.

Industry tailwindsLower logistics expenses, retail industry consolidation, and market share transition from unorganised entities (currently constituting 85-90 percent of Indian retail) to organised ones are some of the key positives that Future Retail hopes to capitalize on.Further, value fashion clothing (constituting about 60-70 percent of Future Retail’s annual apparel sales, and mainly sold through the company’s ‘Fashion Big Bazaar’ stores), benefits from the rejig in GST. Garments with a price tag of less than Rs 1,000 per unit will attract only 5 percent GST, as opposed to a 12 percent rate for those priced in excess of Rs 1,000.

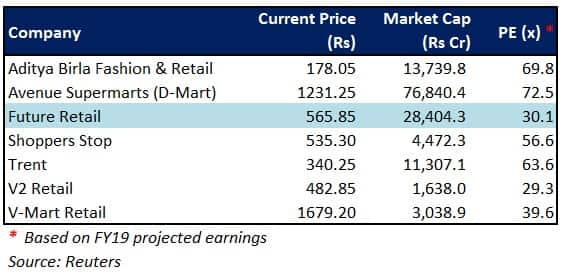

Peer comparison

A gradual reduction in the capital locked in less profitable segments (home furniture, electronics) will enable the company to focus its attention solely on retail of clothing and grocery through its three brand outlets - Fashion Big Bazaar, Big Bazaar, Easyday.

Though Biyani’s Tathastu exists only on paper at the moment, it would be unwise to write him off given the slew of measures that he has undertaken to turnaround the financial performance of Future Group in earlier years.

To achieve a top-line of USD 1 trillion, Future Retail needs to grow at a CAGR of nearly 20 percent for the next 30 years. Inorganic growth opportunities may perhaps pave the way towards achieving the vision, which makes the Future Group an exciting prospect worth keeping an eye on.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!