Highlights

India's fourth-largest cement manufacturer, Dalmia Bharat, posted strong Q3 FY26 results, overcoming GST-linked demand disruptions in the previous quarter.

Going forward, the management intends to scale the business through capacity additions, geographic diversification, cost optimisation and potential inorganic growth opportunities.

Quarterly result highlights

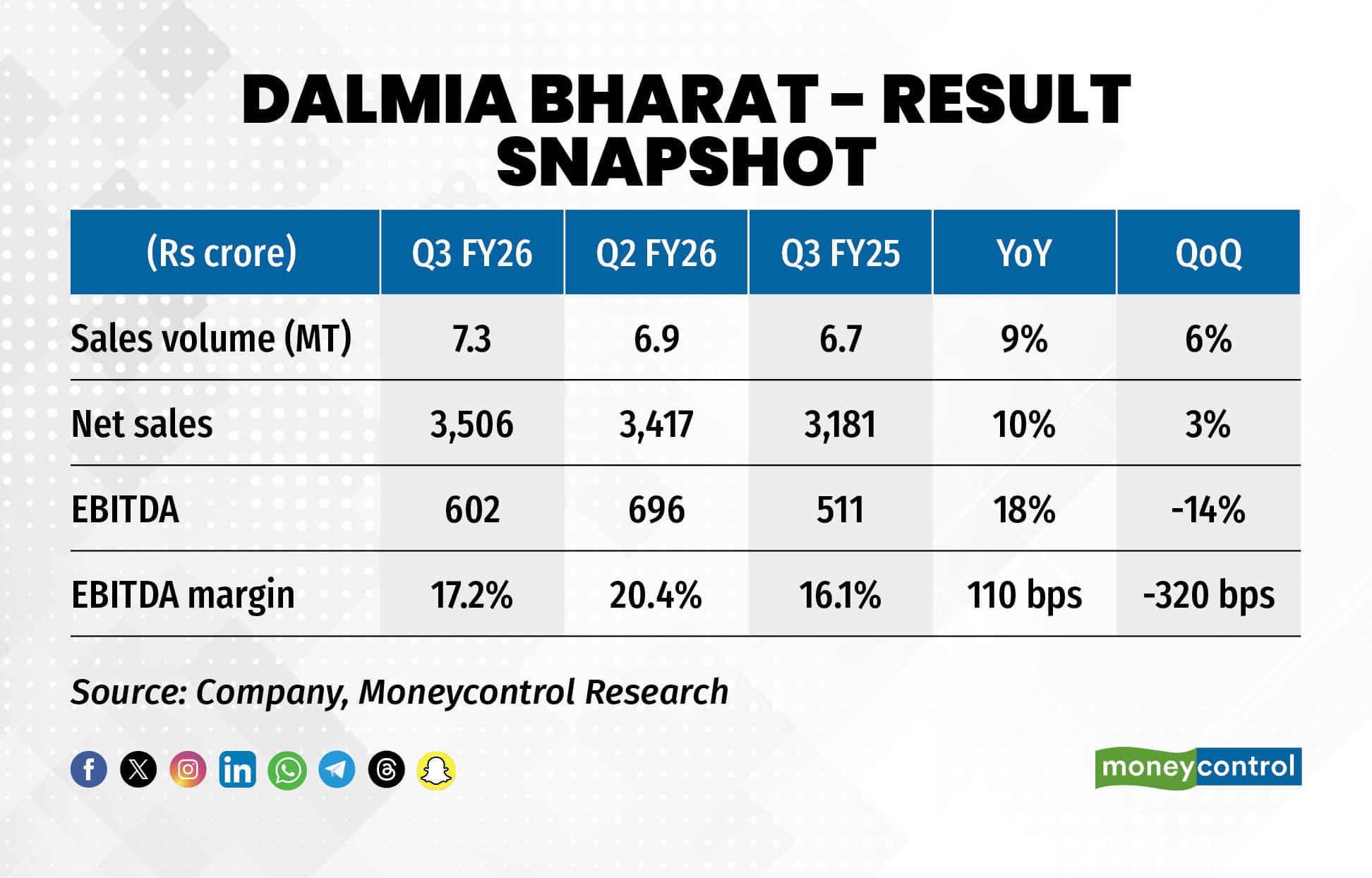

Dalmia Bharat outperformed the broader cement market in Q3FY26 with volumes growing 10 percent year on year (YoY) to reach 7.3 million tonnes (MT), comfortably surpassing the industry’s growth rate of 6-7 percent.

The Q3 volume figures highlight that Dalmia Bharat has regained the market share it had lost in earlier quarters. The share of sales through trade channels came in at 62 percent (vs 66 percent in Q3 FY25), whereas the premium products mix stood steady around 23 percent.

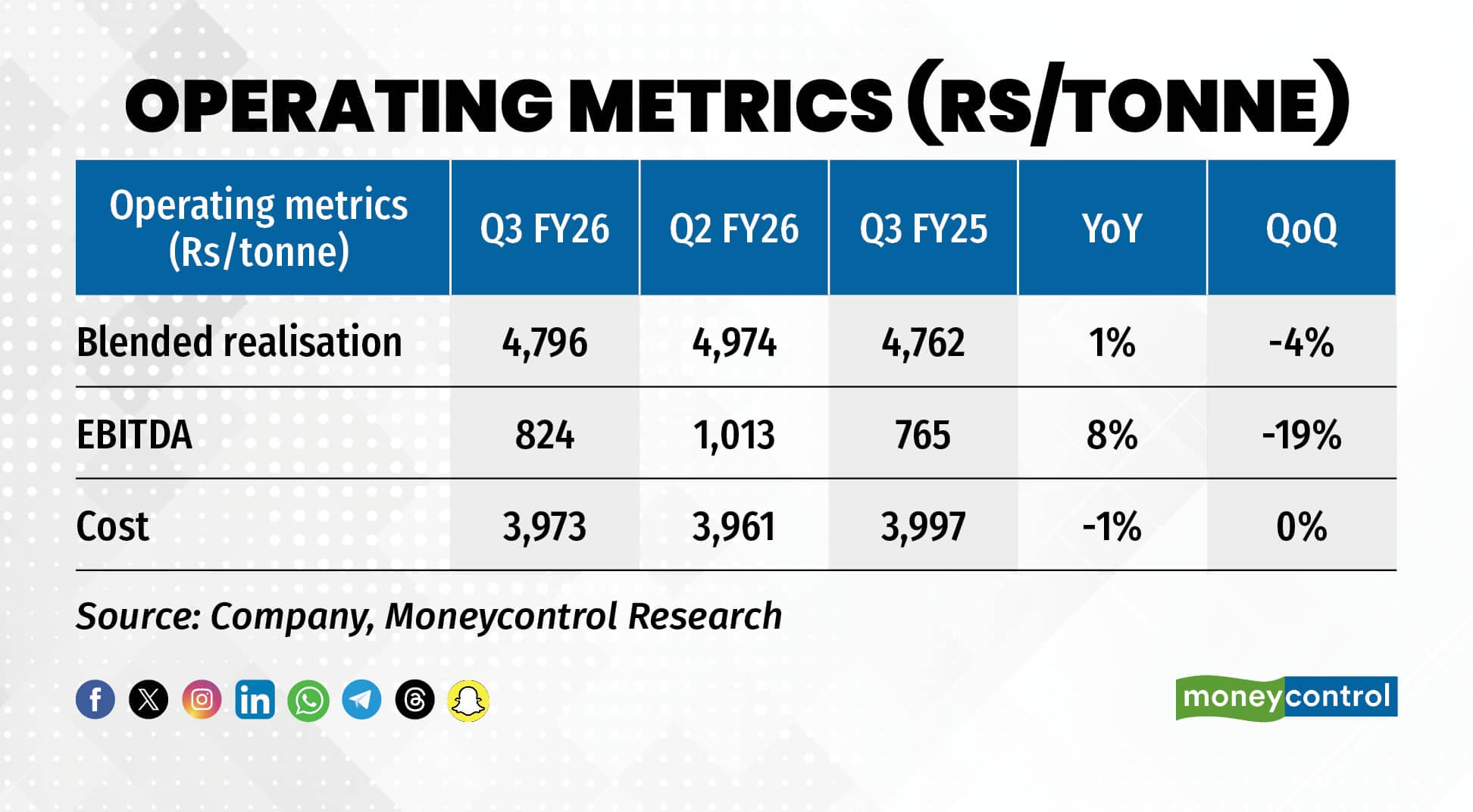

Blended realisations contracted 4 percent quarter on quarter (QoQ), owing to the decline in cement prices after GST revisions. During the last quarter, the southern market witnessed a steep fall in prices due to labour shortages and a slowdown in construction activity. Meanwhile, the eastern markets also witnessed weak price trends on account of Bihar elections.

Raw material costs grew just 2 percent YoY despite the additional levy of mineral tax in Tamil Nadu (Rs 160 per tonne). Operating margins expanded by 110 basis points to 17.2 percent, primarily driven by the reduction in freight expenses (down 6 percent YoY), while power and fuel costs were stable YoY. As a result, EBITDA (Earnings before interest, taxes, depreciation and amortisation) per tonne came in at Rs 824, up 8 percent YoY.

Diversifying manufacturing footprint

Dalmia Bharat is targeting a pan-India market presence and intends to reach 75 MT capacity by FY28. The key projects include a 3.6 MT clinker and 3 MT grinding unit at the existing Belgaum plant, and a new 3 MT grinding unit in Pune to strengthen its western Maharashtra presence.

Dalmia has commenced commercial production from the Umrangso Clinker line (3.6MT) in Jan-26. The management is also evaluating a 6 MT greenfield expansion in Jaisalmer (Rajasthan), for which land acquisition and mining lease formalities have been completed. Environmental clearance is still pending.

The management has given a capex guidance of Rs 4,000 crore for FY26. The company added 143 MW of renewable energy (RE) capacity in 9M FY26, taking its total operational RE capacity to 410 MW. The company is targeting 576 MW of RE capacity by mid-2026.

Price trend improving

Despite regional pricing headwinds throughout the last quarter, 2026 has started on a strong note with prices firming up by 2–3 percent month-on-month in January across all major territories. However, the key challenges for the sector remain elevated competitive intensity and rising fuel costs. Pet coke prices have increased 15-20 percent YoY, which can constrain margins in coming quarters.

Outlook and recommendation

The domestic cement sector continues to maintain a positive trajectory, with industry expecting a steady 6-8 percent growth rate due to robust government infrastructure spending, ongoing urban development, and anticipated uptick in private sector demand.

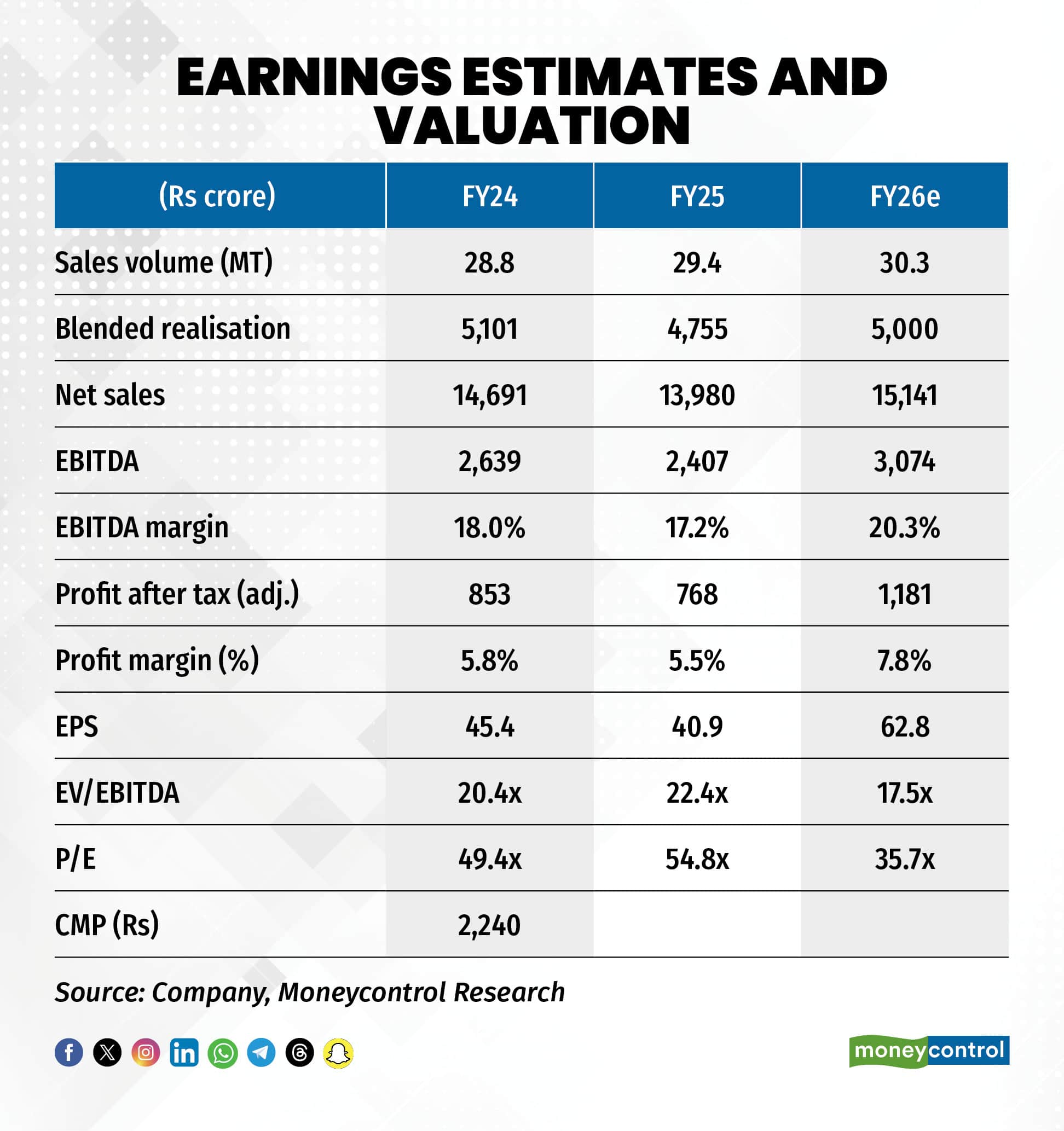

Dalmia Bharat’s operational excellence makes it a solid contender in the infrastructure space, though its premium valuation (17.5x FY26 EV/EBITDA) partly reflects the business positives. Therefore, any correction in share price should be viewed as an opportunity to accumulate shares in a healthy company at a reasonable valuation.

For more research articles, visit our Moneycontrol Research page

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.