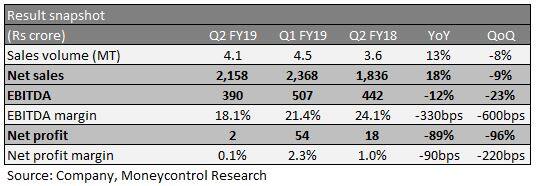

The Q2 FY19 earnings of Dalmia Bharat, India’s fourth largest cement manufacturer, was in line with other industry majors. Double-digit volume growth drove sales, but profit came in softer as the increase in operating costs dented margin. Despite cost challenges, the company continues to deliver industry leading volume growth in the sector through superior execution. The company has consistently outperformed its peers and is gradually expanding its presence through organic and inorganic routes.

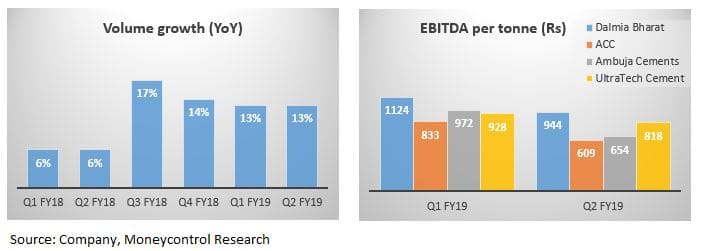

Volume-led topline growth Q2 revenue rose 13 percent year-on-year (YoY) to Rs 2,158 crore. The company sold 4.5 million tonne of cement during the quarter gone by, a volume growth of 13 percent. Strong demand across its key operating markets (east and south) drove volume growth in Q2.

Earnings before interest, taxes, depreciation and amortisation (EBITDA) margin declined 330 bps YoY as the sector is facing challenging times on the cost front. Power and fuel costs as well as freight expenses have witnessed a sharp rise in the last 12 months.

Realisations stable but costs weigh on margin Realisations remained stable quarter-on-quarter (QoQ) but picked up marginally on a YoY basis as the company benefitted from premiumisation. The company introduced fine blend composite (FBC) cement (mix of clinker, slag and fly ash) in the market last year and has seen positive traction in volumes in this product since its launch.

Despite stable realisation, EBITDA per tonne dipped to Rs 944 as unitary cost increased 4 percent QoQ.

Operational performance was significantly better than UltraTech Cement, ACC and Ambuja Cements. EBITDA per tonne continues to be much ahead of its peers.

Looking to optimise cost structure The management has increased focus on operating efficiencies and cost rationalisation measures. Petcoke usage constitutes around 57 percent of the current fuel mix. The company is increasingly looking at alternate sources to optimise its cost structure. The recently secured coal linkage should result in further cost savings. Also, easing of axle norms should help reduce freight expenditures.

Amalgamation with Orrisa Cement (now OCL India) is complete. The company plans to list OCL in Q3 FY19 and expects the combined merged entity to be listed in early Q4 through a share swap agreement.

The company has also completed acquisition of Kalyanpur Cements (1.1 million tonne capacity) and the subsidiary has been renamed DDSPL. The management has been able to revive clinker production from this plant over five months and aims to start commercial operations from November.

The company is still awaiting the National Company Law Tribunal and Supreme Court’s final decision on Murli Industries and Binani Cement, respectively.

Outlook and recommendation Demand for cement has been fairly strong in H1 FY19. However, pricing power remains elusive as industry leaders prefer to chase volumes. Prices as well as demand should remain stable in the run-up to general and state elections.

Despite the higher competitive intensity, Dalmia has been able to outperform the industry both on volumes as well as margin front. High debt and muted price environment remains a concern, but strong cash flows and acquisition synergies should help pare debt and improve return ratios over the next couple of years.

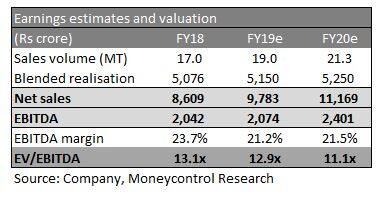

The company has delivered fourth consecutive quarter of double-digit volume growth and remains our preferred pick among large sized cement companies. We expect it to outperform peers in the largecap cement space.

Discover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.