Highlights: - Bata’s Q3 show was impressive

- Store additions and marketing drives will bolster revenue growth

- Margin accretion would depend on rent rationalisation and premium products

- Competition and high ad spends may impact earnings

- Valuations are heady, thus limiting upside

--------------------------------------------------

Bata India has proved its mettle in the third quarter-ended December 31, 2018 on all fronts. Asset-light expansion, a revamped brand portfolio and healthy fundamentals make us bullish on the stock. However, the elevated valuations leave little on the table for a new investor.

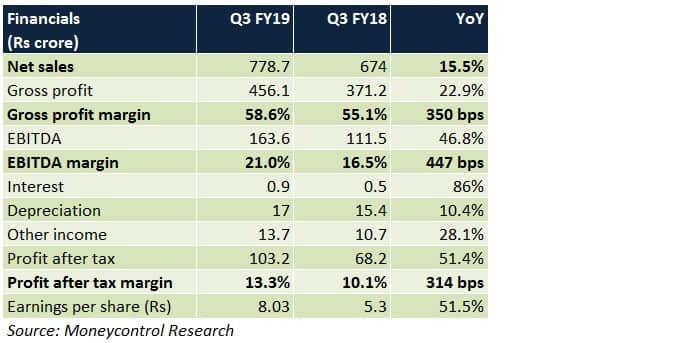

Q3 analysis - Strong top-line growth was seen on account of improved retail coverage and onset of the festive season

- Operating leverage was attributable to approximately 10 percent same-store sales growth year-on-year (YoY), cost controls and an uptick in gross margins

- Profit after tax margins expanded sharply too, aided by a 28 percent YoY growth in other income

Observations Revenue drivers - The management plans to open 100-200 new retail stores each fiscal year to augment its network of around 1,375 outlets (as on March 31, 2018)

- To attract more footfalls, store renovations will continue throughout the year. Additionally, experience centres and kiosks will be launched in a phased manner at the outlets

- Spends on promotional activities are anticipated to increase from Rs 40 crore in FY18 to Rs 80-90/100-150 crore by FY19/FY20-end, respectively. Celebrity-backed endorsements would gain momentum as well

- New offerings in select segments (women, youth collections, sports) are likely to be made available in new exclusive brand outlets. Visual merchandising initiatives would complement this move

- To strengthen its omnichannel, the company is investing heavily in developing its website and mobile application. Blogs and posts on social media will be equally pivotal in this regard

Margin drivers - Stock management processes are being optimised

- The share of high-margin premium products is slated to increase gradually in due course (from 25-30 percent of sales in FY18)

- A major chunk of the capex for new stores will be undertaken by franchise partners

- Rent agreements are under negotiation at a few locations

- Most of the new outlets will be small or medium sized in nature to curtail overheads

Outlook - After a stellar Q3, the stock has set a 52-week high. It has been one of the best performers despite heavy market volatility in recent months

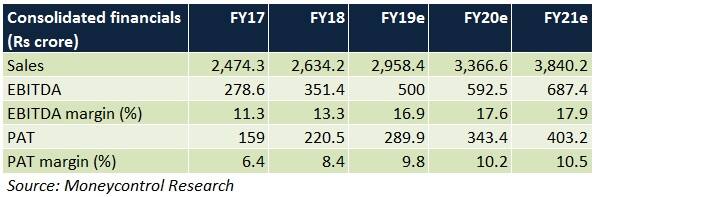

- At 39.7 times its FY21 projected earnings, the rich valuations comprehensively capture all the positives in the short to medium term horizon

- To command such superlative multiples, the company will have to deliver a combination of robust top-line growth and improved margins on a consistent basis (on an already high base). In our view, this could be tough to achieve in an industry where brand loyalty is waning

For more research articles, visit our Moneycontrol Research page

Disclaimer: Moneycontrol Research analysts do not hold positions in the companies discussed hereDiscover the latest Business News, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!

Find the best of Al News in one place, specially curated for you every weekend.

Stay on top of the latest tech trends and biggest startup news.